Yes. Even I am not so stong in to do fundamental Analysis and Technical analysis… But Just learnign and implementing as much as I can.

Hope some day , My all steps will correct

Hope some day , My all steps will correct

Hi All,

I want to know one thing. Coin deducts money for SIP or lumpsum from Kite Balance. So if I have opted for a monthly SIP of a certain amount, do I need to first deposit that amount in Kite Balance (through Q Backoffice) or will Coin directly deduct that amount from my Bank Account monthly ?

Reason for asking this is that if Coin cannot deduct directly from my Bank Account then every month I have extra task of first putting the amount to Kite.

Also everytime I put this amount, Rs 9 + taxes will be charged as deposit fee (as per normal Q backoffice charges)

Thanks,

Omkar

This is the only option available now.

They are working on Direct Deduction from Bank account.

You can add Zerodha’s account number as beneficiary then you can do neft or imps. In this way you don’t have to pay extra 9 rupees you are talking about.

How is using Coin more beneficial than investing in Direct schemes directly thorugh mutual fund websites.

Here is why Coin

When you think it in a long term it will be very less. Take a example you are investing 5k Per month and continued for 25 years.For this You will be paying only 15k. It is very less compared to regular funds. You will be paying 2.52% expense ratio in regular funds.

As you mentioned Rs.59 is the only charge for Coin. May i know what are these additional charges. Can you explain. Will it happen every year. I could not see Demat charges for MF mentioned anywhere in Zerodha/Coin Charges.

Answered here. But it would really be great if you could contact our support desk for account specific query.Tradingqna isn’t meant for support. ![]()

Hi Nithin,

Where can we see the debit of this 50 Rs PM charge? I cannot find it in my ledger.

Regards

With MFUIndia you will save that 15K also. Plz compound 50 PM for 15 yrs

For apple to apple comparison, Zerodha coin should compare itself with its best direct platform competitors rather than regular ones.

The advantages of Coin is valid in case of regular vs direct fund. Highlight advantages over direct fund competitors also.

There are few platforms who charges a flat fee for advisory and few are even free such as Kuvera and Groww. Just naming few.

Basic features such as easy SIP, consolidated view for funds are available in all.

With such comparison Coin would be at disadvantage when total cost is compared (subscription charge+transaction charges at Zerodha and from bank+ GST). Still many features are lacking in Coin such as STP, SWP, capital gain statement XIRR for funds, direct fund deduction from bank account in simple way without transaction charges from bank. These charges are recurring and multiplies if more family members of a person joins Zerodha. This is a case with me. I can list few more disadvantages.

The biggest advantage which I see with coin is updating personal details in one place and one time paper work for nominee claim (everything in Demat gets transferred to nominee at once) but at the same time limitation of one nominee. One support to get in contact in case of any issue, that’s convenient. NAV tracking feature, not much useful though for mutual funds since it does not fluctuate through out the day.

So, the discussion should be focused on both advantages & disadvantages, not one way biased. There may be different requirements for different people.

I would request people from Zerodha to also reply and present their point of views constructively when disadvanges are highlighted.

So, the main reason why I chose coin is for making things easier for my nominee when Iam not around.

Update: Coin app launched and XIIR for individual funds. Though I would also like it for complete portfolio including exited funds.

1 Like

Anyway I have been invested Rs. 1 lakh through coin but currently evaluating other platforms such as Unovest and Groww which are IMHO are very promising. And for security concern any money invested though them is directly bought through various MF platforms(BSE StAR MF, Karvy, MF utility etc) so no concern for your money. I have invested Rs. 10000/- through unovest and then confirmed through the AMC site for the same. Everything is very transparent. Only benefit I have not to pay Rs. 59/- per month for the service. If we don’t require any value added service (Personal Advisory) which they are offering then I think it is best to invest through those platforms.

Yeah i am also thinking of moving out of coin. But i recently started investing (4months) So it looks my P/L is lesser than the remat charges. Not sure what to do.

It will be wise to wait for at least 1 year to avoid exit load, later after completion of 1 year you can move from coin to those sites.

1 Like

@Bhuvanesh

Though Coin is a very good platform to buy MFs but still if someone wants to getout of its subscription then how to do it.

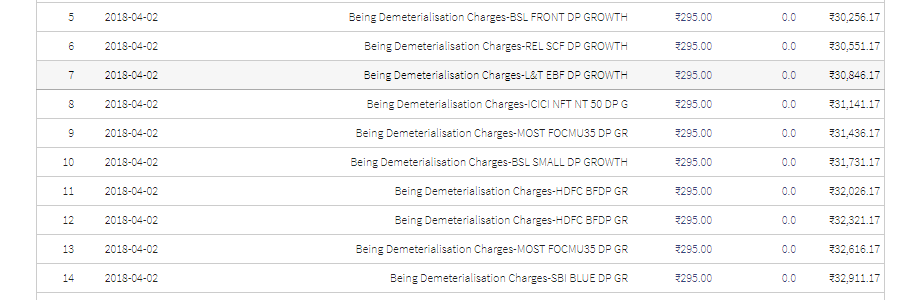

Rematerialisation charges are heavy (150+GST) per folio. Instead of that you can redeem and move to other platforms if your funds are more than 1 yr (to avoid exit expenses)

What if I sell all the units from Coin and purchase directly from MF company and payment will be through the bank account,

If you sell there will 1% expense ratio if fund is less than 1 yr + DP charges 5.5 per folio + tax. Crediting the redeeming amount will take T+3 days. Then you can buy it from MF directly.