rather than lookig at it as starting a business to make loss so that you dont have to pay tax on trading income. think of it as using trading income to boost profits on a manufacturing business, where profit margins are paper thin.

also know that the machines were not bought with cash, so there is no question of opportunity cost. the machines were bought by pledging land.

so heres how the game is played:

you got land? pledge it for something capital intensive (doesnt mean you go buy a bentley) I mean something that generates cash flow… maybe in the maufacturing sector preferably (because I know ONLY this)… CNC machine, laser cutting machine, water jet cutting machine, plastic injection moulding machine, aluminium pressure die casting machine via a loan. look out for subsidies/PLI schemes (the one i went for was Tamil Nadu government’s NEEDS scheme for 1st gen entrepreneurs = 25% subsidy… i.e you can buy machines for 1Cr, but loan principal is only 75L). one more is the CGTMSE scheme where MSME’s can borrow upto 5Cr, collateral free!!!

now it’ll take 2 years to get the business to stand on its own 2 feet, in my case I had to support the business with 30L in the first 2 years, i.e. promoter’s capital…

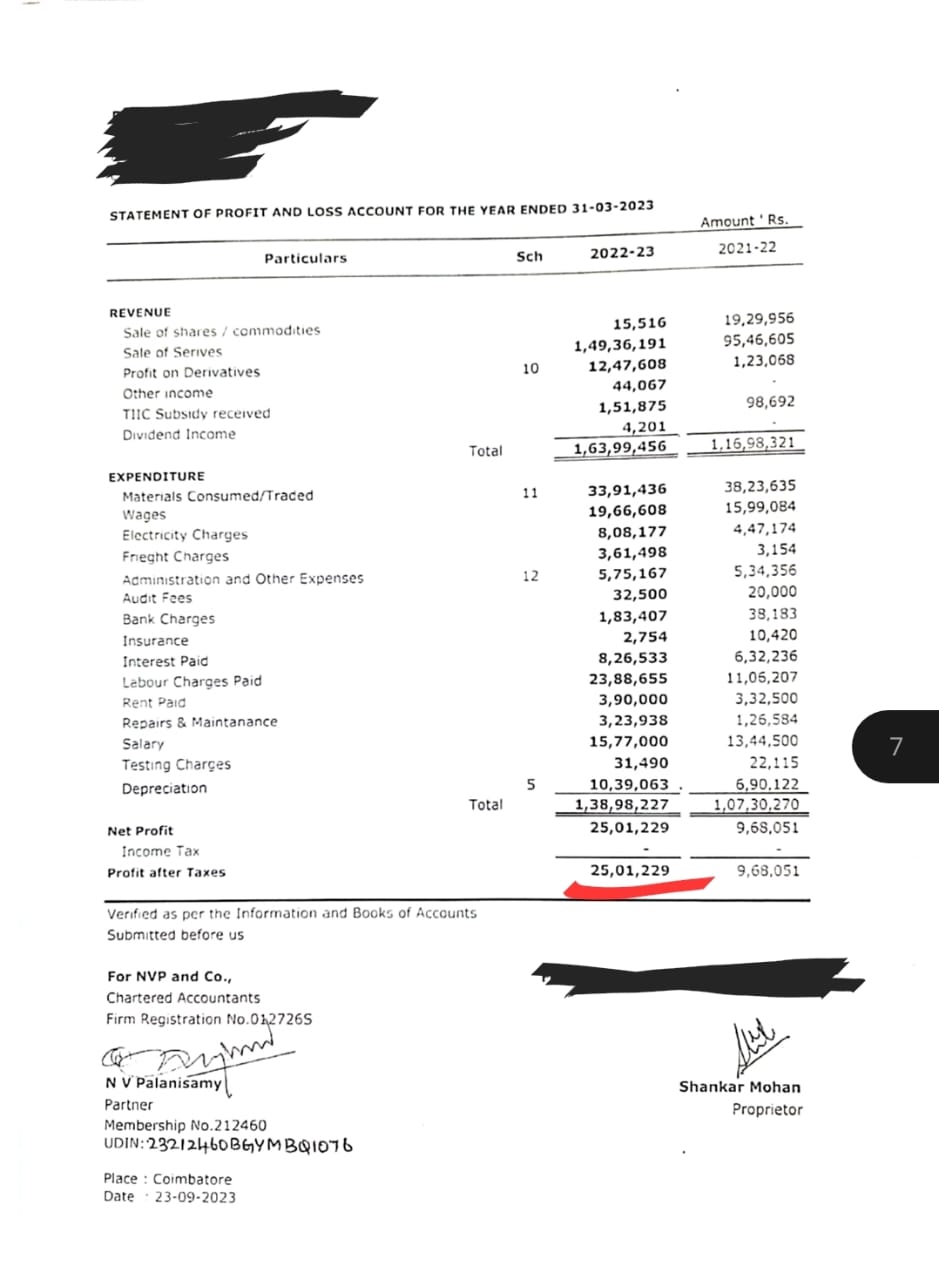

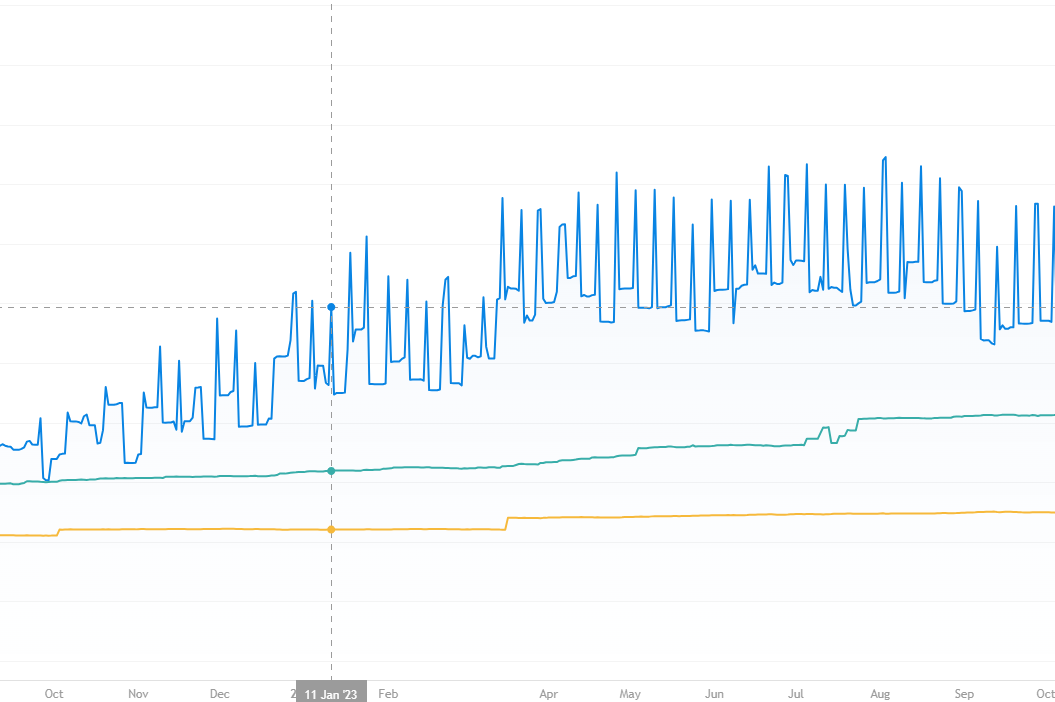

manufacturing business are not known for the profits they generate, but are known for the tremendrous cash flows. in my case i was rotating 10-12 L every month + had access to around 30L (20% of turnover) as overdraft facility. i use my overdraft facility only on wednesday, thursday and friday (i trade ONLY NIFTY)… so every thursday i have the ability to deploy 30L which is not my cash (it is dangerous I know, but my loss will not be the burden of my lenders/creditors, if i take a big hit, i can still pay off people, thus my increased risk appetite)