Here you go, this one will be a long post, understandably so, since I’m trying to compress and post the highlights of a 460 page doc

Background

ICICI Securities has filed DHRP, this indicates that they file for an IPO anytime soon. Previously there are instances where companies have filed DHRP and withheld the IPO for various reasons. Hence there is no guarantee that ISec will go ahead with the IPO.

Nevertheless, there is a ton of information available here, and it matters especially for people working (or aspiring to work) in the capital markets. I’ve picked information only that matters and which I thought makes sense.

So here you go, let me start with the risks involved in the business -

-

ISec (ICICI Securities) operates in the capital markets with interests in broking, distribution (MF, Insurance), and Investment Banking

-

The business is sensitive to Market risk, economic conditions, and inflation

-

Bulk of the business is dependent on the 3-in-1 model, which means ICICI Bank has a serious play here

-

On average, brokerage income contributes 66.7% of the revenue, 23% from distribution, and the rest from Investment banking, and prop trading

-

This means the business is susceptible to - regulatory risk, RMS risk, regulatory risk on distribution, risk involved in the deal-making industry, and risk from prop trading

-

Apart from that, there is also serious risk of safeguarding client information (UIDAI, CERSAI, CKCY etc)

-

ISec has about 3.8M clients, but only 5% (1.9L) of these contribute to the entire revenue

-

They have a debt of close to 640 Crs

-

ISec has nearly 7L clients who have traded at least once in the last 1 year. This was 5L in 2013

-

Client addition grew from 2.1M in 2013 to 3.8M in 2013

-

200 branch offices, 4600 sub-brokers.

There is a lot if industry gyan, here are the highlights -

-

Estimated revenue from all brokers is @ 14K Cr, this also gives you a sense of how big the industry opportunity is. This has grown at 20% year on year and 14% CAGR since 2013.

-

Full-service brokers have 95% of the pie, 5% belongs to discount brokers

-

There are about 200 brokers, with at least 1 active client

-

Turnover from the Top 5 brokers increased from 14% to 19% from 2013, top 25 contributes to 51%

-

CRISIL pegs the brokerage industry to grown to 30K Cr by 2022, this is roughly 15-18% CAGR

Some information from the MF distribution business -

-

Across all the AMCs, total AUM stands at 20.4LCr (as on Mar 2017), representing a growth of 26.8% since 2013

-

Last year has been quite phenomenal with 40.1% YoY growth

-

3.4LCr was the inflows into MF last year compared to 1.4L in 2016

-

732 distributors qualify under AMFI distributor commission disclosure norm, this was 373 in 2013

-

Distributor commission grew from 24KCr in 2013 to 50Cr in 2017, growing at 20.1%. (HINT: Invest in direct MF via Coin and save on comissions)

-

Top 10 distributors were paid 48% of the commissions, of which top 7 were banks

-

Besides the banks, NJ and ISec feature in top 10

-

3.5% of the overall distributor commissions were paid to ISec

Valuations

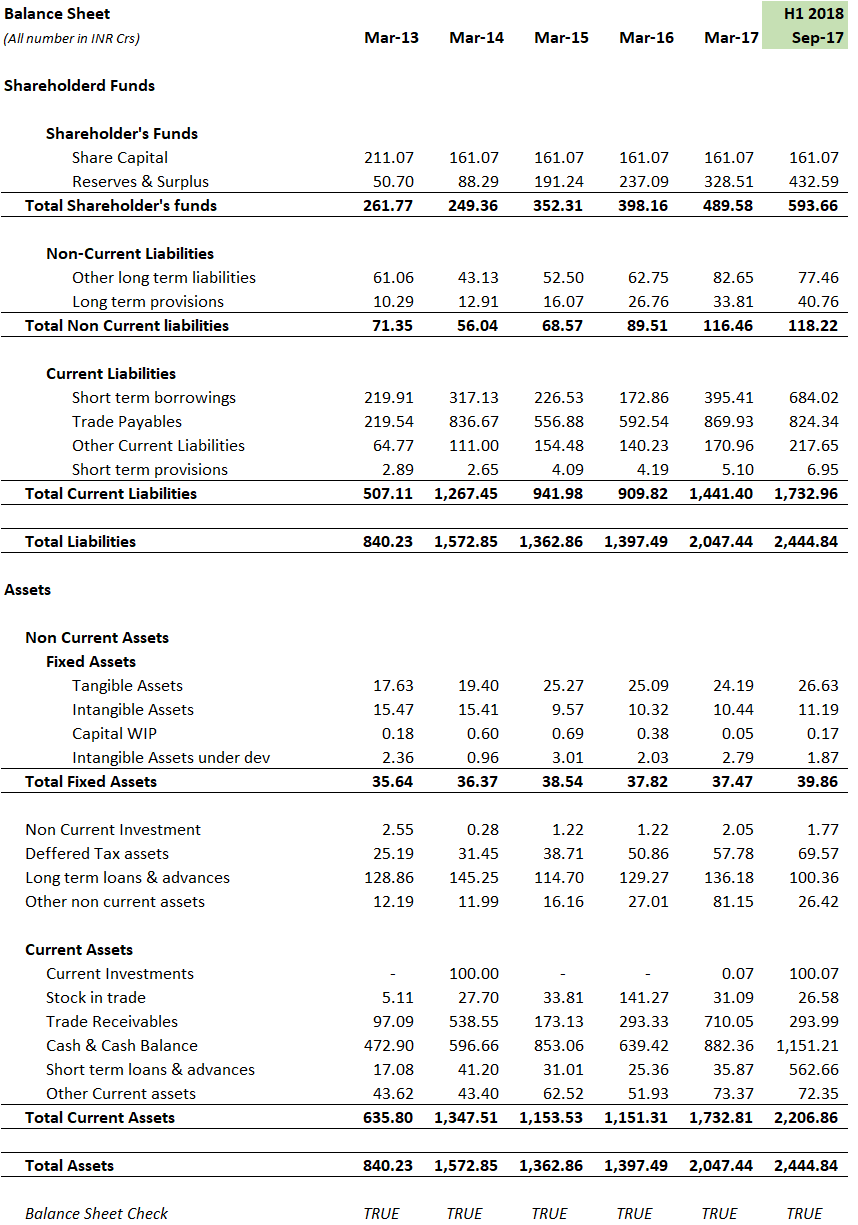

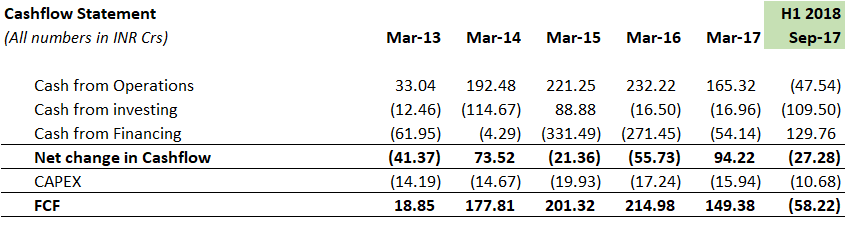

Have a look at their financial statements, I’ve converted the numbers to Rupee Crores (they’ve reported in INR Mils). They have reported the numbers from Mar 2013 to Mar 2017, plus the 1st half of 2018 ending, Sept 2017. The numbers are quite impressive -

Balance Sheet

P&L

Cash flow (with CAPEX and FCF)

Based on this, I did a rough 2 stage discounted cash flow valuation, I call this the quick and dirty valuation, basically to give me a sense of how big the business really is. Most importantly, I’ve valued this business based on March 31st 2017. There is data available for H1 2018, which I’ve not considered. So this should give you a sense of the ‘quick and dirty’ natures of the valuation.

Here is the DCF snapshot -

The core intrinsic value of the business according to this is about 4500 Crore as of 31st March 2015. Note, this does NOT include any premium. This is just its bare bone worth. This also translates to a very conservative share price of Rs.137 - 140. Include fiscal 2018, I’d suspect the share price of say Rs.175. Point to note is that this does not include any premium.

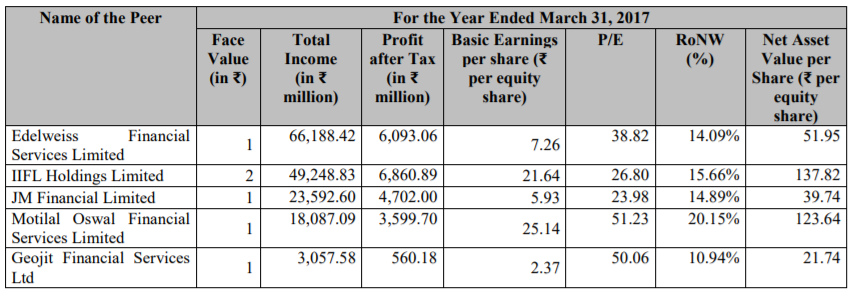

The industry Price to earning is as follows -

Highest is 51.2X (Motilal)

Lowest is 24x (IIFL)

Average is 38x

Considering ISEC’s EPS at 10.51 as on 31st March 2013 and the avg industry multiple, the share price should be around Rs.400. However, EPS of ISEC has grown phenomenally, so assuming at least a 25-30% growth in EPS (for FY2018), the estimated EPS is about13.66, and at 38x, the share price translates to Rs.520. This translates to about 16.7KCr marketcap, which I think is a tad bit expensive.

I wish I could spent more time on this for a more accurate valuation, but I guess this should be ok for now.

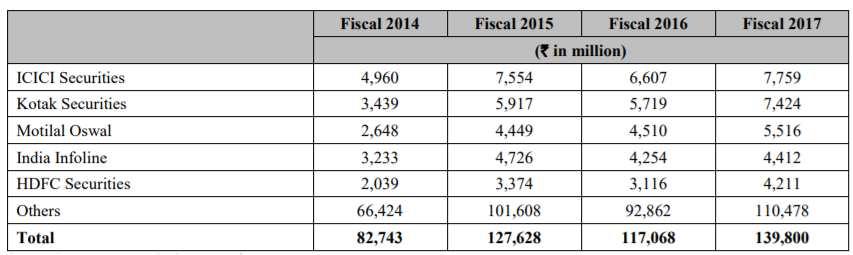

I found few other useful information, here are the snapshots -

Industry Revenue -

Industry Valuation (listed peers) -

Distribution commission and their market share.

I’ll stop it at this, comments are welcome!