UPDATE: IDFC FIRST Bank now requires Rs. 25,000 as Average Monthly Balance w.e.f. 1st April, 2019 and non-maintenance of the aforesaid AMB will attract a penalty from Rs. 50 - Rs. 400 as per the various segregated slabs of the maintained balance.

what are the benefits of using 3in1 account

1 Like

I can’t see my idfc bank balance on kite funds page

That’s not good. I guess I’ll have to move back to my Kotak Edge saving account that requires only Rs.10,000/- AMB with lots of advantages over IDFC. The whole idea behind moving to IDFC was to have some kind of seamlessness which isn’t worth the effort.

1 Like

@nithin @Bhuvan

I had a chat with IDFC First Bank Representatives, they said that for 3-in-1 Zerodha account we need to open a savings account with minimum 25000/- as AMB. They also said that the zero balance account is no more available for new customers.

Don’t you think 25000/- as AMB is quite high for an account used for the purpose of trading?

You are right. I made a mistake moving from Kotak to IDFC. My Kotak Edge account has AMB of 10,000 which is reasonable. Also keep in mind that Kotak is a much bigger bank than IDFC and has more/better services. For AMB of 25,000 IDFC is providing those services free of cost which are not much used in everyday banking. How many of write cheques frequent;y or order a demand draft?

@Nithin @siva

What are the benefits?

Do we get 7% even after we utilize whole margin daily for intraday trades?

Can check benefits here, also you won’t be getting saving bank rate as it takes t+1 day to credit to your bank account.

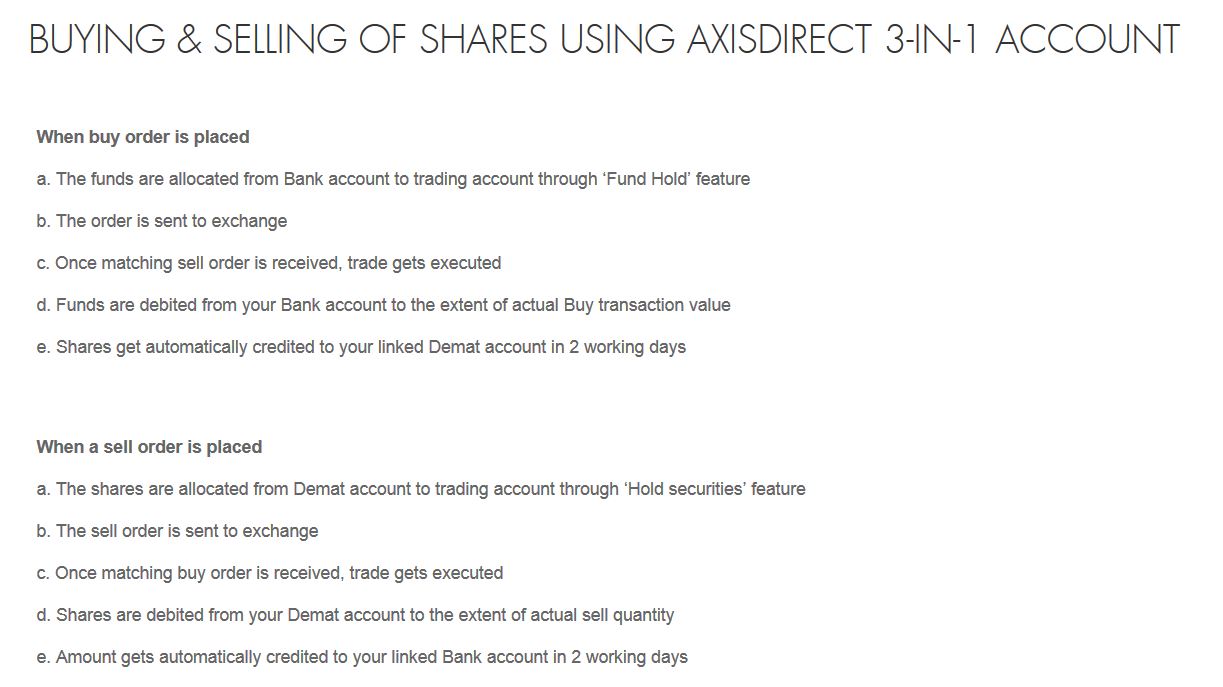

Hi @siva. Please correct me if I am wrong, but my IDFC 3-in-1 Account does not seem to work like other 3-in-1 accounts, like Axis below for example. The debits and credits do not happen automatically from the savings account. Instead we have to add/withdraw money manually from the trading account. Is this the way its intended to work or will things change in the future?

@siva I also recently opened the saving account in IDFC to get it linked with Zerodha to avail 3-IN-1 benefits. So, it means 6% or 7% interest rate will only be availed if that is in the IDFC First bank account but not if it is zerodha funds for trading? Means, 3-in-1 is only helping us in to save on transfer charges that we can otherwise do with UPI or with net banking? Hope, I am clear with my query.

@NithinKamath…Please help on below 2 queries. For example, if I have parked 2 lakh in my IDFC first saving account.

Q1 If I need to trade with 50,000 for intraday, do I need to transfer that first to zerodha fund from IDFC First manually or will it auto debit from the bank account?

Q2 If I have transferred 1,00,000 to my Zerodha funds but only utilized, 50, 000 out from that for intraday, will the remaining 50,000 kept in the zerodha fund will get 6% interest from the bank?

Hi @Vikram_Verma,

Q1 If I need to trade with 50,000 for intraday, do I need to transfer that first to zerodha fund from IDFC First manually or will it auto debit from the bank account?

- This has to be added manually, you allocate funds to the Zerodha account using the one click transfer on the Payin page on Kite.

Refer:https://support.zerodha.com/category/account-opening/idfc-3in1/articles/benefits-3in1

Q2 If I have transferred 1,00,000 to my Zerodha funds but only utilized, 50, 000 out from that for intraday, will the remaining 50,000 kept in the zerodha fund will get 6% interest from the bank?

-The unutilized part of the funds lying in the Zerodha account will not yield any interest from the bank.

Thank you @lindo @siva …means if I have KOTAK account connected to the zerodha, I will just need to bear transfer charges while transferring funds to ZERODHA while with IDFC First there is no transfer charges & instant transcation,

I need POA to be submitted for connecting my IDFC with Zerodha for 3-in-1. Will that be safe option or should I let my KOTAK bank connected only instead of IDFC? Please suggest.

Hi Vikram,

Can you please clarify with a idfc zerodha 3in1 account can i withdraw funds in real-time even now ?

Hello,

I am not sure and actually I haven’t tried it…

I am happy with the current setup, linked my HDFC account and I get it quickly…

Based on the info that I have read here is the summary between HDFC Account linked to Zerodha against IDFC First 3 in 1 with Zerodha.

- Fund Transfer to trading account is real time in 3 in 1 and HDFC Bank(without charges) it takes around 5-10 mins to reflect

- Fund withdrawal is same except that withdrawals in 3 in 1 account done on 2nd & 4th friday will be deposited only on follow on Monday against Saturday itself in HDFC Account.

- No limit on fund transfer in 3 in 1 and in HDFC it is Rs.25,00,000/- per day.

- 3 in 1 account is available only for Equity and Commodity should continue to be regular mode. Hence you can do fund transfer to commodity only during NEFT/RTGS timings without charges.

Additional 3 in 1 benefits can be seen when when funds are blocked during trading & only the required amount is deducted from savings account by end of the day or transfer funds during trading hours along with automatic withdrawal of excess money/margin into savings account by end of the day.

Has anyone been using this feature…Have both Zerodha and IDFC accounts but was not aware of seamless funds transfer between IDFC and ZERODHA…Now I can actually move from Angel to Zerodha