One query I keep seeing here is about what fund to select. And I think, this is a wrong question. Investors will do better to figure out why they are investing, what are their goals, whether they are achievable, how much risk they can bear for each goal, and then think about the instruments for various goals. Fund selection, in the grand scheme of things, doesn’t matter.

Now, assuming that you know your goals and how much risk you can take for each goal, here’s how you can build a simple low-cost portfolio for long-term goals which are more than 10 years away like Retirement.

Active vs passive

Before I talk about the funds, the topic of active or passive has to be addressed. The reason being, active funds largely don’t make sense. Globally, we’ve seen the Index funds have become popular choice in the recent decade. In the US over 80% of all large. It’s the same in India as well.

In the large-cap space today, it makes ZERO sense to invest in actively managed funds. You might be wondering why?

- The markets have become increasingly professionalized and are dominated by algos, institutions etc. These guys have humongous resources and compete among themselves. With lesser dumb retailers supplying alpha, it has become impossible for large-cap funds to beat the Nifty 50 or Nifty 100.

- SEBI a few years ago recategorized all mutual fund categories and defined the stock universe for large, mid and small-caps. So, large-cap funds can only invest in the top 100 stocks by market cap. There are 40 large-cap funds and none of the fund deviate significantly from the benchmark to generate alpha.

- Perhaps, the most important reason is costs. You can invest in a Nifty 50 index fund for 10bps. Even a direct large-cap fund on average charges 1.5%. So, the large-cap fund straightaway has a disadvantage of 1.4%.

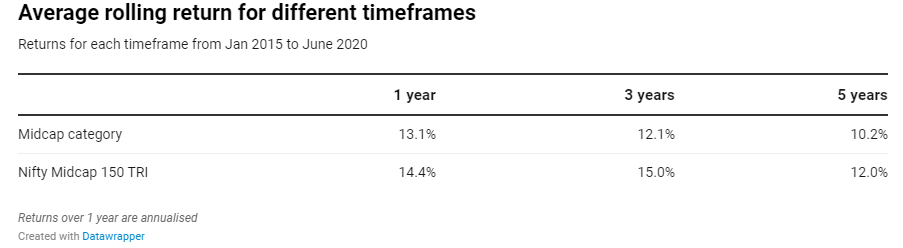

- Even in mid-caps, fund managers are having a tough time beating the Nifty Midcap 150

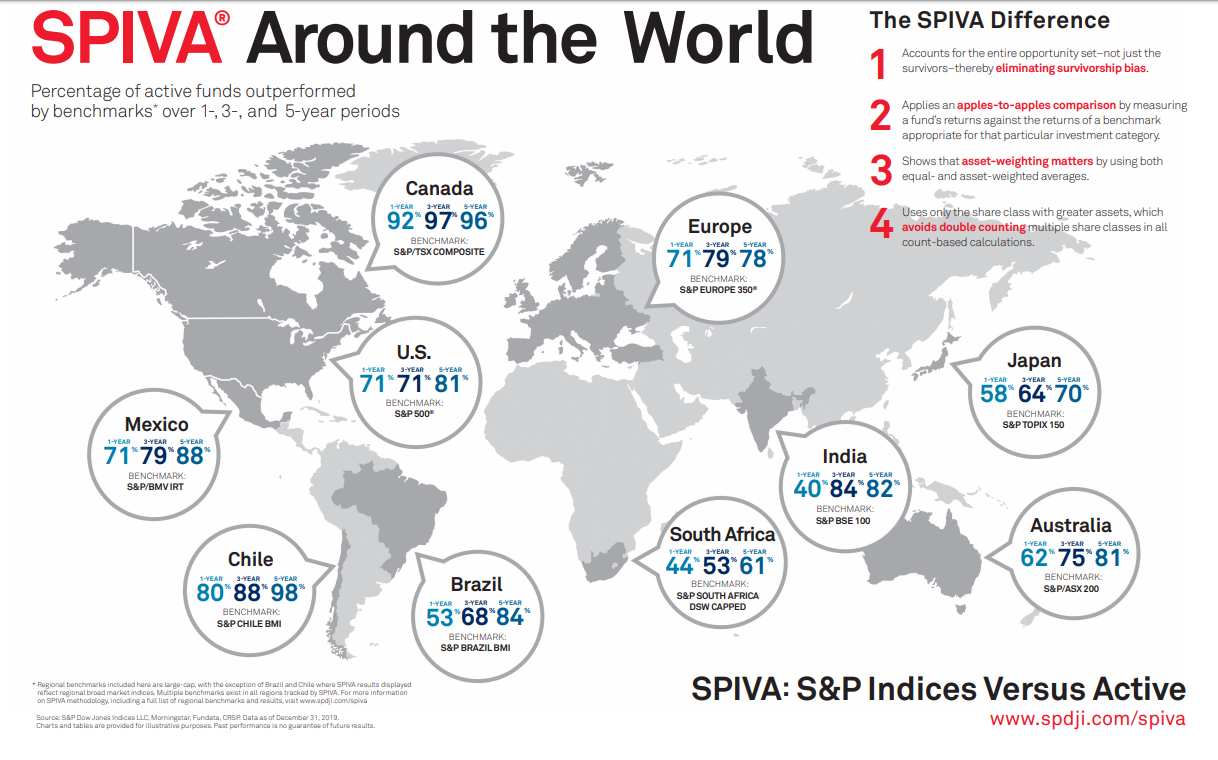

Source: Primeinvestor

Active or passive?

It’s active and passive. From the image, you can see that 8 out of 10 funds underperform the index. So, picking an active fund is nightmarishly hard. What you can do is use a core and satellite approach to portfolio construction. The core is where you put a bulk of your money to get market returns (index fund) and in the satellite portion, you can pick some active funds to generate some extra return over and above the benchmark.

Duration

You can only use these funds for goals over 10 years. That is TEN! Not 3, not 4, 10. For shorter goals, you are better off having lower equity exposure. And for goals under 5 years, you should not invest in equity at all in my view.

Funds and ETFs

Core equity

Nifty 50

Nifty Next 50

Motilal Nasdaq 100 ETF or FOF

Motilal S&P 500 (MF only, no ETF)

Satellite equity

Active equity funds

Smart beta ETFs like ICICI Low Vol ETF, Nippon NV 20, ICICI Alpha Low-Vol, DSP Quant Fund

Thematic funds (I don’t like them personally)

smallcases

Core debt

Bharat Bond ETF or FOF

Banking & PSU debt funds

Corporate bond funds

GILT Funds (for goals above 10+ years). Stay away if you don’t understand interest rate risk

Satellite debt

People recommend credit risk funds etc. But I don’t think investors should be chasing return in debt. Stick to safer bond funds.

Satellite commodities

Goldbees

Sovereign Gold Bonds

How much to allocate

This is a very personal question and there is no right answer here. The equity debt and gold split depends upon your risk tolerance and risk capacity - both are not the same

Risk tolerance - your ability to take risk

Risk capacity - whether you should take the risk. For example, if you are 55 years and have the ability to take risks, it would be foolish to have to say 50% of your corpus in equity. Hence your risk capacity is low.

The easiest way to start off is with a 50/50 or 60/40 equity and debt split and then see if you have the guts to handle the volatility and then adjust your portfolio.

How to allocate between core and satellite

A bulk of your money should be in index funds. For example, if you have Rs 100 to invest in equity Rs 80 should be in index funds and Rs 20 can be active or smart-beta funds

Which index funds?

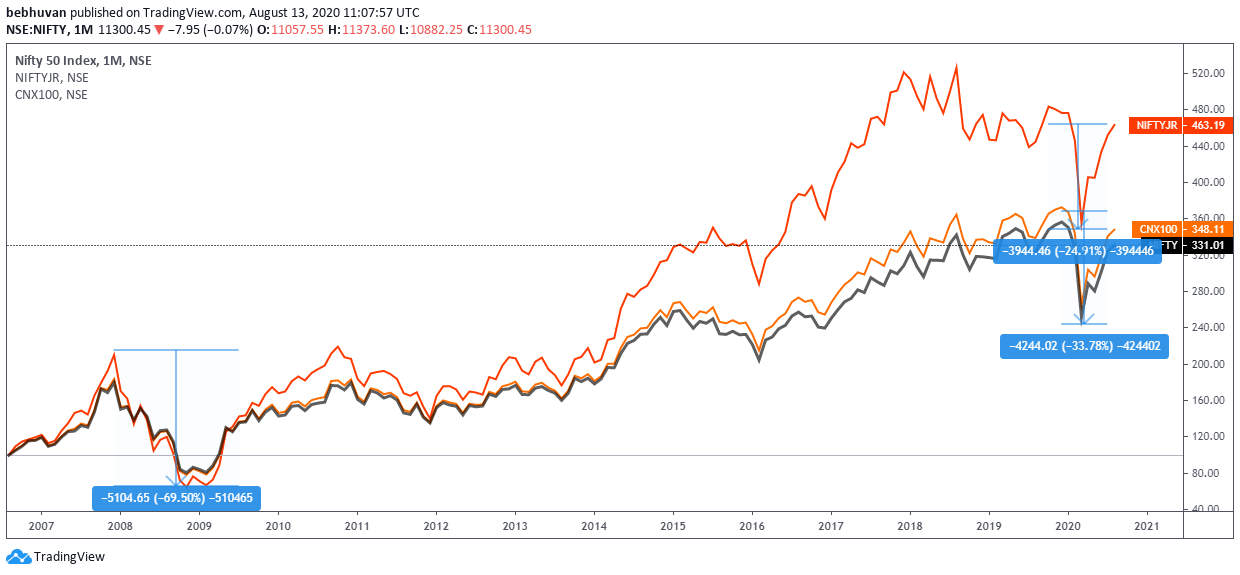

I personally believe Nifty 100 is enough. You can either do this by buying Axis Nifty 100 fund or combine Nifty 50 + Nifty Next 50. Remember, Nifty 50 + Nifty Next 50 is not equal to Nifty 100!!!

Nifty Next 50 is an extremely volatile index. It is similar to a mid-cap index in reality. Look at the peak to trough falls. In 2008 it fell by nearly 70%. So, beware.

How much international?

India is just 2% of the global stock marketcap. That means a majority of all the emerging opportunities are outside India. And global indices aren’t as correlated as Indian indices are. Add to this the fact that Indian rupee tends to depreciate over time. It makes sense to have some global diversification.

In my view, either the S&P 500 or Nasdaq 100 will suffice. Nasdaq 100 is tech-heavy and tends to be more volatile than the S&P 500. While the S&P 500 is less volatile. Pas returns of Nasdaq 100 have been phenomenal but that comes at a higher risk.

Alos, over 40% of the sales of S&P 500 companies come from outside the US. So, it is just like owning a global fund.

Stay away from other global funds, fund of funds, and feeder funds offered by Indian AMCs. They are costly and mostly very very bad products

How much gold?

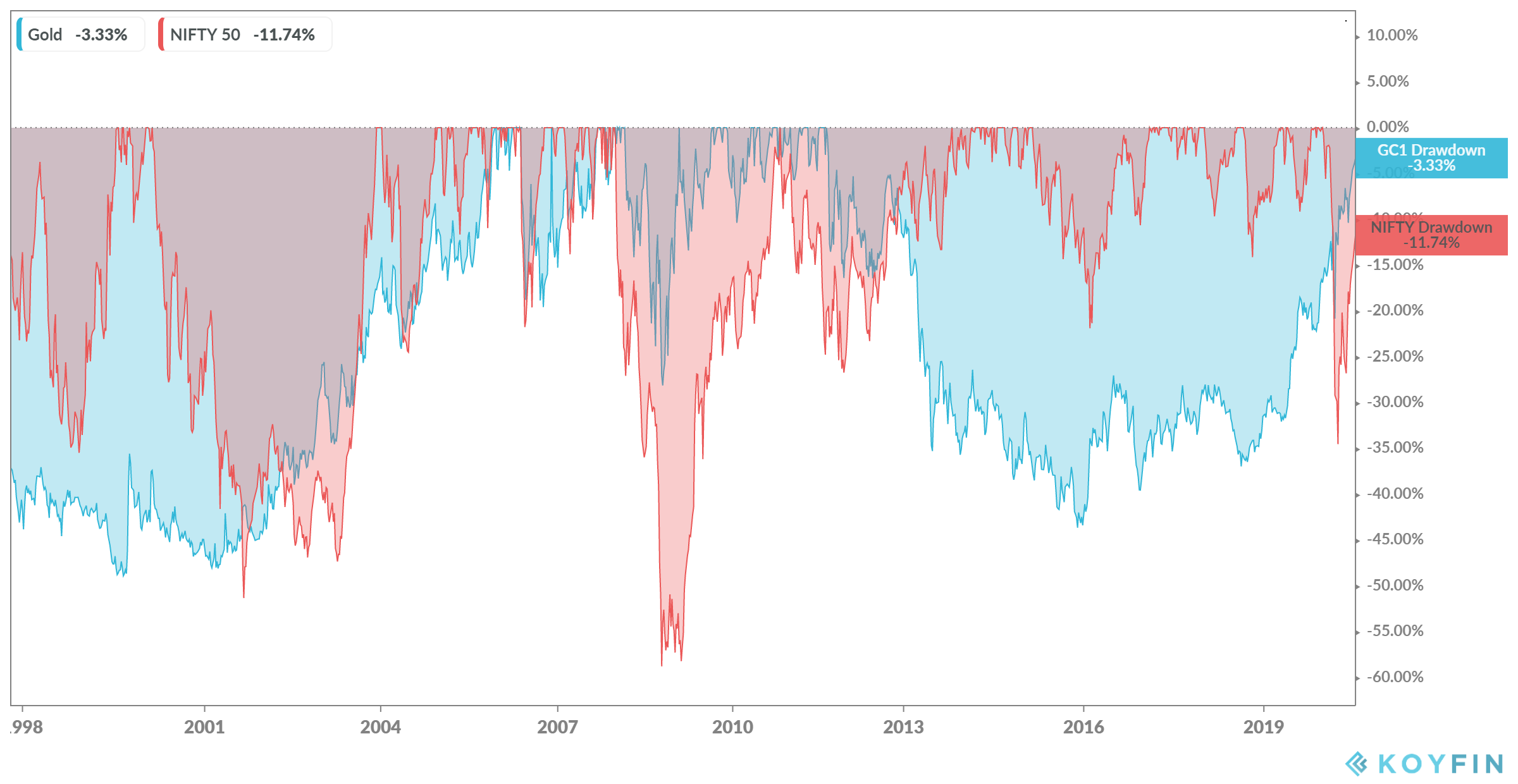

Having an uncorrelated asset like gold makes sense. By uncorrelated, I mean an asset class that does the opposite. But you need to understand that gold go long periods doing nothing/

Moreover, gold is an incredibly volatile asset class. It’s as volatile as equities. Here’s the drawdown profile of gold vs Nifty. So, you need to figure out how much you can invest.

Debt

Look, the reason why you invest in debt is for stability. Not for generating returns, that’s why you have equity. So, the return of capital is more important than return on capital. So, it makes NO SENSE to chase returns in debt. The best way is to choose funds with relatively low credit and duration risk and invest in them. Bharat Bond ETF is a brilliant product. You can choose the 3-year duration fund if you don’t want too many hassles. The 10 year ETF/fund comes with a lot of duration risk and is as good as owning a GIlt fund. So if you are buying a 10 year ETF, be double and triple sure you know what you are doing.

You can also pick a decent corporate bond or Banking & PSU fund.

Two important risks you need to be aware of when investing in debt funds are interest rate risk and credit risk. Without knowing these risk, I can guarantee you that you will end up losing money with 100% certainty.

This Varsity chapter is a perfect starting place.

Rebalancing

Make sure to rebalance your portfolio periodically. Otherwise, you end up damaging your portfolio. If you are hearing about this for the first time, here’s a handy explainer