Franklin schemes are now live on coin

We must consider Inflation when we deposit in RD.

5-6% interest in next year hardly earns 0-1% real return due to tax and inflation.

I suggest you to go for Balanced Mutual Fund if you’re conservative investors [10-13% returns in average], otherwise go for ELSS Mutual Fund [tax saving and returns upto 20%] or Large Cap Fund [18-22%] if you’re moderate investors. But I also suggest diversified fund which is also better option [20-25%]. And SIP MF is best option due to Power of Compounding, and advantage of Rupee Cost Averaging.

You can withdraw any time you wish, there’s no restriction.

Consider exit load (generally 1%) which exist only when withdraw upto 1 year. Otherwise, no exit load for more than a year.

And ELSS fund has 3 years lock in period.

Here are recommended funds below:

- HDFC Small Cap Fund [Diversified Fund]

- HDFC Balanced Fund [Balance Fund]

- Aditya Birla Sun Life Tax Relief 96 Fund [ELSS Fund] (tax saving and deduction under section 80-C)

- SBI Bluechip Fund [Large Cap Fund]

Other than ELSS Fund, 10% LCGT tax will be applicable only when you have gained over Rs. 1 Lakh profit.

I don’t think you have understood the requirement. Allow me to explain to you in a better way.

I have set RD installments every month which helps me accumulate funds for renewal of insurance premium, etc annual subscriptions.

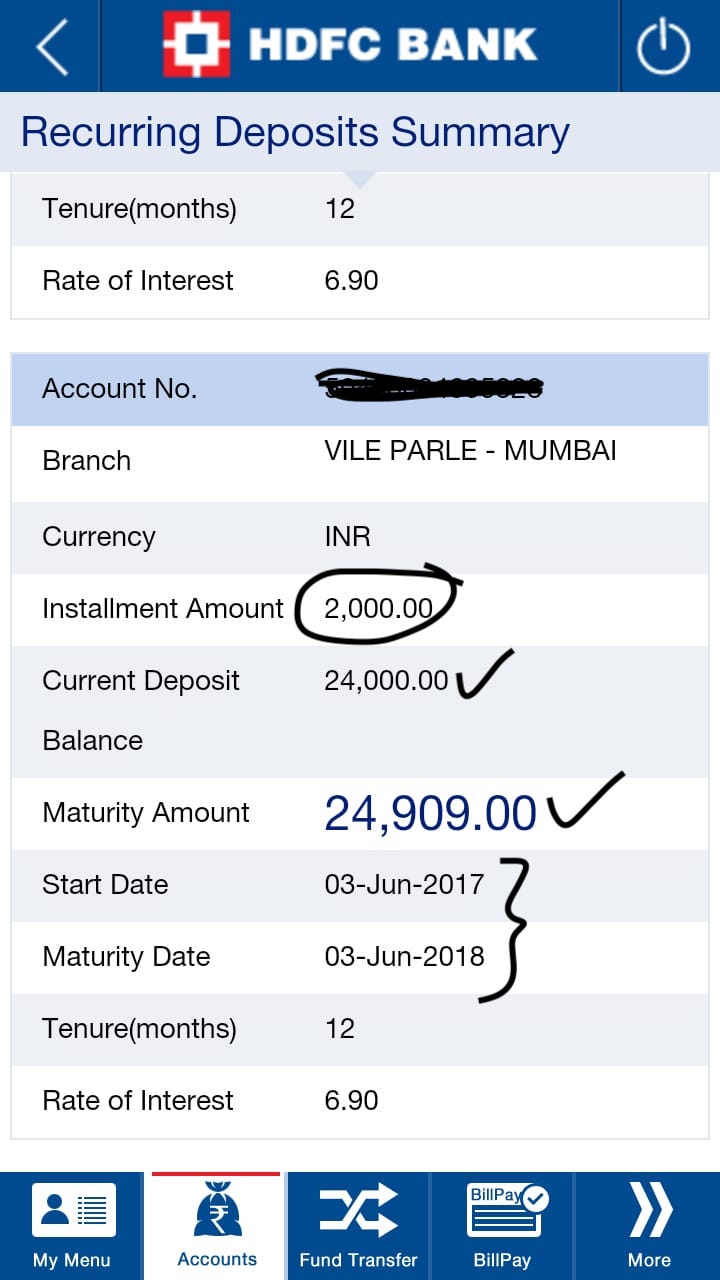

E.g. this RD of Rs 2000 which was started on 3rd June 2017 @6.9% interest rate will mature on 3rd June 2018.

So total investment of Rs 24000 will fetch me Rs 24909 at the time of maturity.

I will use that amount to renew my insurance premium and start another fresh RD for a tenure of 1 year to plan next year’s renewal.

Now from 24909 - 24000 = Rs 909 is the profit on investment at maturity.

10% TDS will be deducted on 909 i.e. 909 - 90.9 = Rs 818.10 is my income which will be then added to total income in the FY and then will be taxed as per the tax slab.

My initial question was if there is a better way to plan this? I discovered Franklin Templeton Ultra Short Bond Fund which in past has given returns of approx 7.5-9%.

RD gets you 6.9% interest where 10% TDS will be applicable.

whereas,

Franklin Templeton Ultra Short Bond Fund has a historical return of approx 7-9%. And there is no entry or exit load but since it involves redeeming units at the end of 12 months to pay for the annual insurance premiums, there would be a short-term capital gain of 15% on profits.

Instrument | Investment Period | Returns (%) | Taxation

++++++++++++++++++++++++++++++++++++++++++++++++++++

RD | 12 months | 6.9 % | 10% TDS

Ultrashort MF | SIP 12 months | 7.5 % | 15% STCG

Thus, would like to explore more, if there is any other better way to invest for 12 months with no exit load and yet better returns so as to compensate for 15% short-term capital gains?

Are there any other MF which don’t have exit load for redemption in 12 months and better returns (while keeping the investments safe as every 12 months they need to be withdrawn)?

Hope I have articulated the requirement well.

Please let me know.

Did you explore HDFC SavingsMax Account ?

Cheers

Vinay

The reason I brought Equity funds is to get better return and escape tax (through ELSS).

But I get your point, there’s something I need to clarify this taxation view

Since Ultrashort bond fund is a debt fund. STCG (<3 years) = as per individual income tax’s bracket) [Not 15% which belongs to Equity Fund]

The only way to get better than FD is either Corporate FD or Debt Fund only. But debt funds are preferred in my opinion. Your picked Franklin Ultrashort bond fund is a good one.