With less than a month remaining to invest in tax-saving investments until the end of the financial year, now would be a good opportunity to make lump sum investments to meet the tax exemption limit of Rs.1.5 lakh u/s 80C.

Should investors invest in ELSS now that markets are volatile?

Unlike fixed income instruments such as PPF, NSC or tax saver FD, making lumpsum investments in ELSS (for instance, when markets are falling) can impact the future value of your returns. This is because an ELSS is an Equity-linked Savings scheme with a minimum 80% of its underlying investments comprising Equity or Equity related investments. Investors can use opportunity of any correction that the markets offer by investing a lumpsum.

How does ELSS compare with other tax saving instruments u/s 80C?

The following table offers an overview of the return potential of the different tax saving instruments.

Past performance may or may not be sustained in the future. These are historical values. The actual NPS returns might vary.

Data as of June 30, 2021. Source: paisabazaar.com.

Why has ELSS been the preferred option?

An ELSS is a tax saving investment to achieve an investor’s long-term goals such as child’s education or retirement. It complements an investor’s equity allocation to profit from the long-term economic growth in India.

ELSS funds have been the preferred option in recent years for the following reasons:

a. Tax benefit: ELSS funds offer a tax deduction of up to Rs 150,000 under Section 80C of the Income Tax Act. This means up to Rs.46,800 tax benefit can be availed by the investors falling under the highest tax bracket.

b. Dual benefit: ELSS tax saving funds offer dual benefits: tax exemption and wealth accumulation.

c. Diversified Portfolio: ELSS mutual funds have underlying investments in a diversified equity allocation, thereby allowing investors the opportunity to earn long term risk -adjusted returns.

d. Lowest lock-in among other tax-saving options: An ELSS stands out due to its minimum lock-in period of 3 years giving investors the flexibility to redeem once the lock-in tenure is completed. On the other hand, the mandatory lock-in period of three years helps significantly reduce the portfolio churn and thereby keep a check on the expense ratio.

Cope better with inflation over the long term: Investors should look at the real rate of return after the impact of inflation when looking at the return potential, With an ELSS, though the return is not guaranteed, it has the potential to generate a long term real rate of return. In addition, ELSS scheme gives investors exposure to equity markets which historically gives potential for higher returns commensurate with the risk exposure and help cope with inflation over the long term.

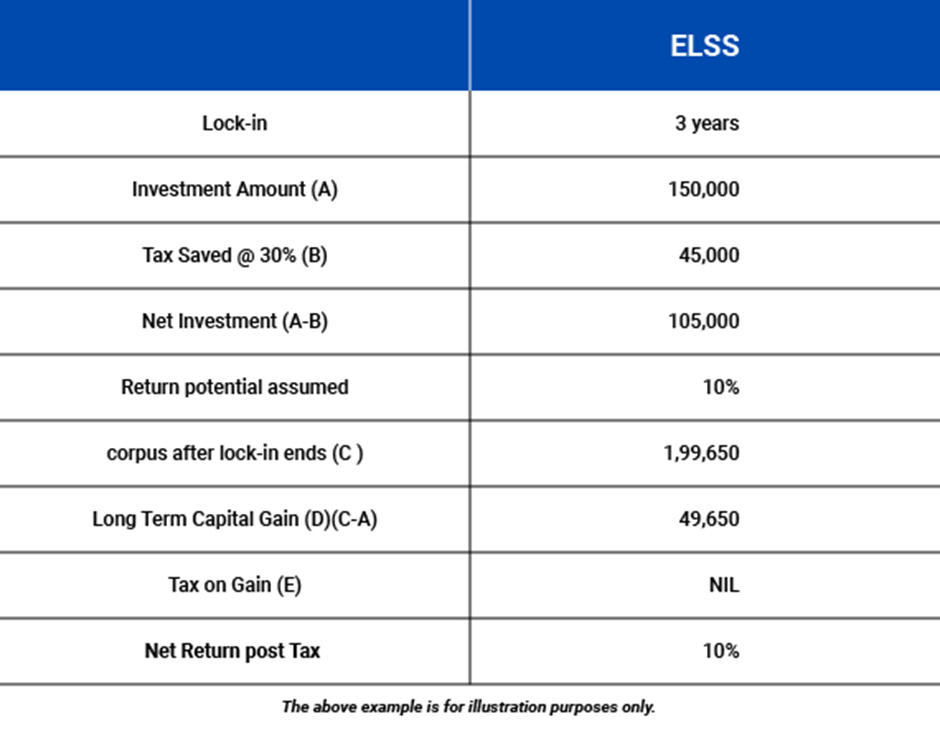

How does an ELSS work– An illustration

Suppose an investor Ajay, who is in the highest 30% tax bracket, decides to invest Rs. 1,50,000, he would have a tax benefit of Rs.45,000 (excluding education cess). Thus, for a net investment of Rs.1,05,000, after the 3-year lock-in period, at an assumed rate of 10% return, he could have earned on his investment at around Rs.2,00,000.

Long-term capital gains of up to Rs 1 lakh a year are made tax-exempt in case of an ELSS scheme. Any gains over this limit are taxed at a flat rate of 10% plus applicable cess and surcharge. Thus, an ELSS offers potential for

However, investors are to note that since ELSS mutual funds are equity-oriented funds, they carry similar risks that any other equity mutual fund carry. Therefore, investors can reduce the impact of market volatility by staying invested over the long term to achieve one’s long-term financial goals. Therefore, though an ELSS has the lowest lock-in, investors must exercise restraint and stay invested for the long term to take advantage of the market cycles and ride out the market uncertainty.

An ELSS investment is an equity mutual fund and hence is suitable for investors willing to take high to very high risk to earn potential for higher returns than other tax saving investments u/s 80 C. Start investing a lumpsum and avoid the rush before the financial year ends to avail the dual benefits!

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual fund investments are subject to market risks read all scheme related documents carefully.