As of last week i noticed one thing which is that many of the NIFTY CE that were OTM declining in premium even when the market was moving Upwards. I try to relate it with theta greeks but I’m not able to as I’m talking about the Nifty 10000 CE 14th May expiry anyways it gained premium in last trading session of the week. But every other Nifty CE of June month also declined by 100%

It has to do with option greeks, check about volatility and time value, can refer varsity options module here, also see videos on sensibull to understand options better.

Well i did study the Varsity module 5 and then only this doubt came to my mind.

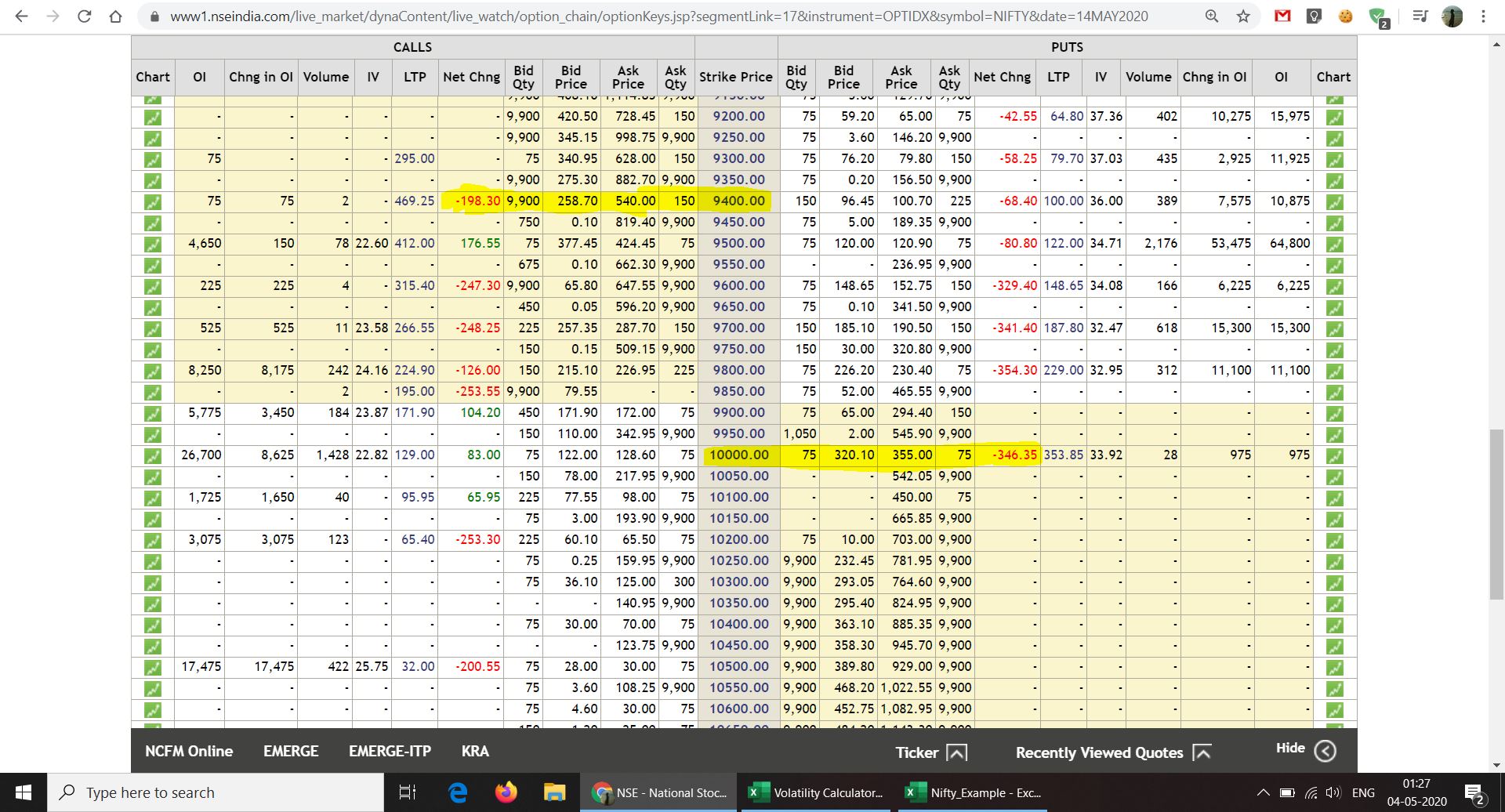

Expiry for all these strikes is 14-May-2020

price of nifty increased from 9553 to 9859 in the last trading session(30-May-2020).

As you can see in the screenshot 9400CE Premium is also decreasing. Now according to the greeks:

Delta - 0.55 (ITM option)

so it should increase.

Gamma - I don’t know how relevant it is for this outcome.

Theta - Even if we take it 10. Then also it should decrease only 10 point from one day to another.

Vega - Around 5. then even if the IV cooled of from 30 to 25, there should only be change of 25 in premium.

Coming to the conclusion even after studying the module thoroughly (although studying the last chapter still left), i don’t understand why the premium decreased 198.

PS - Considering Theta and Vega as i don’t know how to get the past data of IV.

you are looking at the illiquid contracts …

its not necessary that call will gain when mkt goes up and put will gain when market goes down

So you mean to say that liquidity also plays role in determining the premium price? If yes can you please elaborate how?

Hey thanks Gautam for such a beautiful explaination.