Hey @adityaparakh

Dont look at Delta - cause vega is too low.

I’ll correct it slightly - Dont look at vols. Because Vega is low and vols dont really matter outside OTM.

Dont look at premium price - as it wont effect delta-neutrality for practical pusposes or taking position.

It is rather important to be equidistant from weekly-future price. - Yes

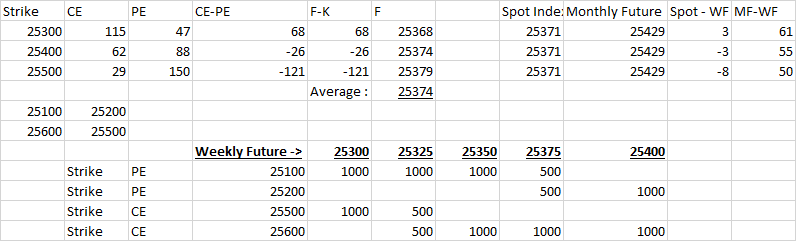

To determine this future price :

For 25500CE = Rs.127 , 25500PE = Rs.173 ,

127-173 = F - 25500 , Hence F = 25454

I am a little surpised here. The future is in discount! Math is correct.

where the option prices are weekly ones. Choice of strikes of Options ? Closest to Spot ?

If I use : 25600CE=Rs85 and 25600PE = Rs.228 ,

85-228 = F-25600 , Hence F=25457 Close enough.

D will always be considered to be 1. All Days of Week / All 4 weeks ?

D = E^rt were t is number of days/ 365

Week1 =1.001151

Week2= 1.00230402

Week3=1.00345802

Week4=1.004613349

So take 1, unless you are looking at longer term options

From this F value , we become equidistant and we are good ?

Spot : 25490 , MonthFuture : 25498 , Weekly F : 25454

A 200-250 point OTM position would 25200PE/25700CE based on calculated Weekly F. -

Yes

This F value , is more appropriate than SpotIndex or the Month End Future value ? Yes

As to determine the F value , and take our position we are not looking at all at the Spot or the Month-End-Future. !?

Interestingly, yes

The price of the options plays more role. This F becomes our only input for the OTM Strangle position.

Yes

Secondly a lesser significant question :

Say , Weekly F is 25525 , what would be an ideal combination to make a good balanced strangle average 200 points away

25300-25700

and least effected by moves either side.

And for 25575 ?

**25400-25800 **