S&P BSE Sensex increased by 4.3% on a total return basis in the month of October. It is down by just 2.8% year to date recovering most of its losses for the year despite the sharp sell-off seen in the month of March 2020. S&P BSE Sensex performance was better than developed market indices such as Dow Jones, S&P 500, which gave negative returns during the month. It was also better than the MSCI Emerging Market Index which rose by 3.5% (like-to-like currency)

Mid-cap and Small-cap indices underperformed the Sensex in October; with the BSE Midcap Index rising by just 1.4% and the BSE Small-cap Index rising by 0.2%. On a YTD basis, their performance is much better compared to the Sensex with the BSE Midcap index rising by 0.6% and the BSE Small Cap Index rising by 9.7%.

Banking, IT and Real Estate were among the winning sectors for the month. Banking sector stocks have positively surprised in the Q2FY21 results with much better collection efficiency and Asset Quality relative to expectations. Healthcare, Auto, and Oil Gas stocks underperformed during the month.

FIIs were net buyers in the month of October buying stocks worth USD 2.7 bn. In 10 months of 2020, FIIs have been net buyers of USD 6.7 bn. DIIs were large net sellers in the month, selling USD 2.4 bn worth of stock. Cumulatively they have bought USD 6.6 bn worth of stocks. Indian rupee depreciated 0.5% during the month.

Rising Global Nervousness

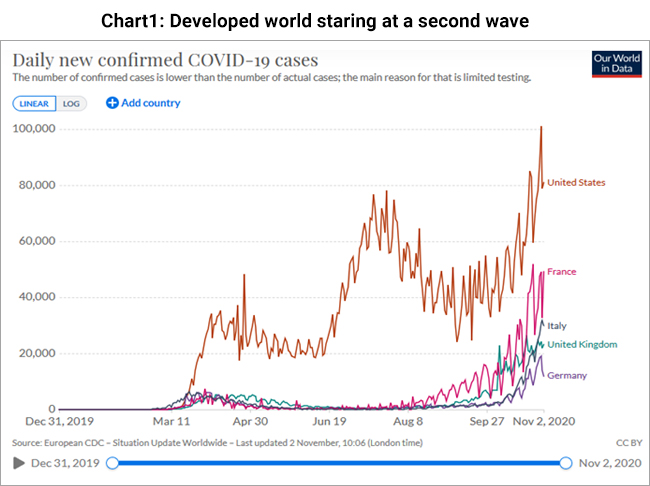

Internationally a rising wave of new covid cases remains the biggest concern for Equities as the US and Europe stare at record new cases and mull further lockdowns. The event risk of an upcoming US election has further raised risk aversion. However low-interest rates and loose monetary policy have so far been a big support for equity markets. With Central Banks in the mood of “Doing whatever it takes for as long as needed”, one can expect an extended period of low-interest rates elevating probabilities of mispricing risks. The US elections as we write this note looks to be a much tighter affair than what experts predicted. Irrespective of whoever wins we do not believe US policy towards India is going to alter much, India continues to be perceived as a credible counterweight to China and we expect India will continue to be viewed favorably in the US view of the world.

India in a comfortable place

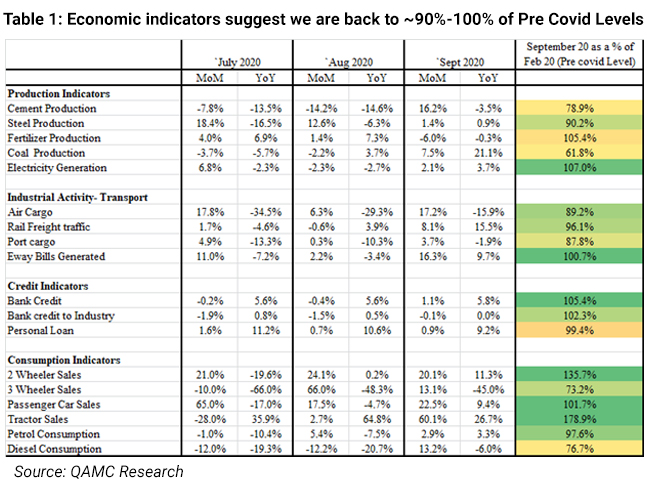

Falling new Covid cases and continued easing of lockdown has meant India is in a much more comfortable place than its developed market peers. Indeed economic data points to activity getting back to ~90% levels and in some cases even crossing 100% compared to pre covid levels. The festive season has started off on a mixed note with some sectors reporting robust sales while others advising caution.

Initial trends of Q2FY21 results have generally been positive with companies doing better than analyst expectations, which were fairly muted after Covid related lockdowns. The strong recovery numbers could have been influenced by pent up demand as well as inventory build-up, as companies gear up for the festive season. There is a risk that the demand resurgence may fade once both the variables are exhausted. Our research team continues to actively engage in channel checks as well as interact with company management to gauge the sustainability of the recovery. Given the impact on income due to the stringent lockdown, we remain slightly cautious about its sustainability.

Valuations rich

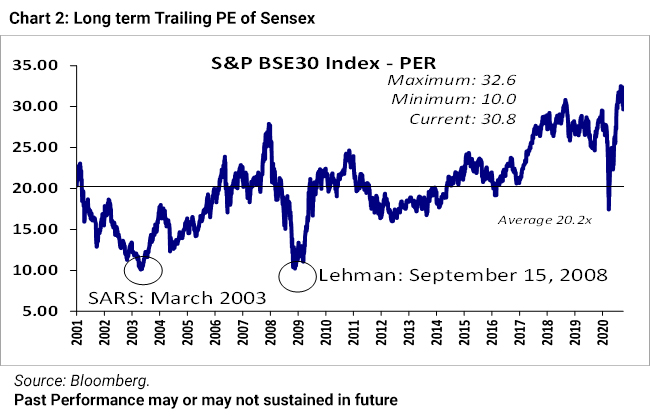

The current PE of the Sensex at ~31x trailing earnings is significantly higher than its long term average of ~20x. One of the factors for the substantial spike in the current PE is the sharp drop in Q1FY21 earnings driven by a severe lockdown. But even adjusted for that anomaly the PE is significantly higher than its historical average. Even though overall market valuations are rich, given the concentration of the rally, we still find pockets of opportunity where valuations remain reasonable

QLTEVF saw a 4.0% appreciation in its NAV in the month of October. This compares to a 2.9% increase in its benchmark S&P BSE 200. Outperformance for the month was driven by holdings in IT and Cement stocks. Stocks in Financials and Consumer Discretionary underperformed relative to the Benchmark Cash in the scheme stood at approx. 10% in October. After a sharp run-up, the scheme trimmed its weight in an existing IT name.

Despite rich valuations, we remain optimistic about Indian equities with a slightly longer-term view. In a relative world, Indian companies that are expected to grow much faster than their western peers will continue to look attractive for investors seeking growth. Fortunately, the major growth driver of the Indian economy is domestic consumption and GDP is less dependent on demand from the western world which may struggle in a post-Covid environment. Apart from a near term concern on extended valuations, we remain hopeful that the Indian Equities remain an attractive investment avenue for domestic as well as foreign investors and will continue to create wealth over long periods.

Data Source: Bloomberg

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments.

Mutual fund investments are subject to market risks read all scheme related documents carefully.

Please visit – www.QuantumMF.com to read scheme specific risk factors. Investors in the Scheme(s) are not being offered a guaranteed or assured rate of return and there can be no assurance that the schemes objective will be achieved and the NAV of the scheme(s) may go up and down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risk such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme(s). Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-) Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited. The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956.