I had invested 50k in the 3 year NCD ISIN: INE202B07IY2 which I think on paper would mature on 4/6/2021.

If that is the only DHFL NCD you hold, as per approved resolution plan, you should expect around 95%+ of 50K once resolution is completed

Hi Akash

I have copied your write up to create a new post as I thought whatever you have advised makes common sense.

The topic is “Few things retail investors can do”. If I continue here it would be high jacking the original topic of DHFL

1 Like

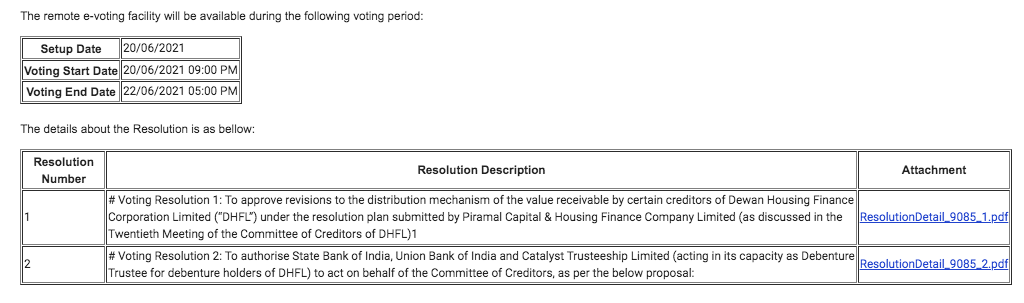

https://www.evotingforibc.com/download-resolution-pdf/9085/12054/Y

https://www.evotingforibc.com/download-resolution-pdf/9085/12074/Y

@Akash_Shah looks like DHFL is proposing only 40% payback to the Secured NCD holders in the new resolution regardless of the investment amount, compared to 92% previously as mentioned by you for category 1 with investment < 2 lakh?

I couldn’t find any such reference in the proposed amendments.

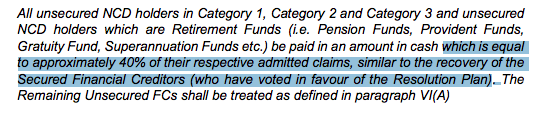

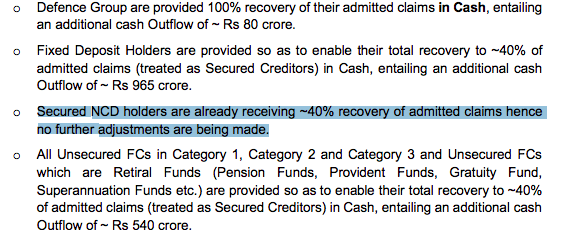

I think in this amendment they are proposing 40% for unsecured NCD holders (which weren’t getting anything earlier) and for FD holder they will ensure that everyone at least get 40%.

And some extra cash for defence institutes.

Apart from that there is no change in resolution plan. So I assume original full payment to secured NCD upto 2 lakhs stay.

That’s my understanding

page 2:

page 9:

please check again. except the defence category, haircut for all despite the investment amount.

On twitter also few are talking about the same.

https://twitter.com/MoneylifeIndia/status/1406528070362615815

1 Like

Yes, as I said, page 2 refers to payout to unsecured NCD holders.

There is difference between secured and unsecured NCD. Earlier unsecured NCD holders were not getting anything so amendment is proposed to give them 40%

Page 9 makes a generic statement that secured NCDs are already getting 40% which is true for most NCD holders (less than 2 lakh investor are small part of total secured NCD holders)

It also says no further adjustments are being made which means original proposal of payment for secured NCD holder stays (means less than 2 lakh should get full 100%)

People on twitter are full of opinion but lack any subject knowledge, so I generally avoid reading them, but even money life tweet specifically says two new resolution, which to my knowledge refers to 1) unsecured NCD & 2) defence

So I don’t see any reason for original plan changing. And secured NCD less than 2 lakh should be getting 100%

That’s how I am reading it, but let’s wait for some more clarity

Okay, keeping fingers crossed.

One more query to you, and @Quicko:

Just in case we have to take a haircut, it’s a long-term capital loss in a debt instrument.

Do you know how is taxation, loss carry forward and set-off work for this?

@Akash_Shah Received an update.

https://pr9.saymails.com/ctltrustee/preview.php?nc=vm&m=90&u=UwMFDAMGBA0=

Yup, I got that too from the trustees.

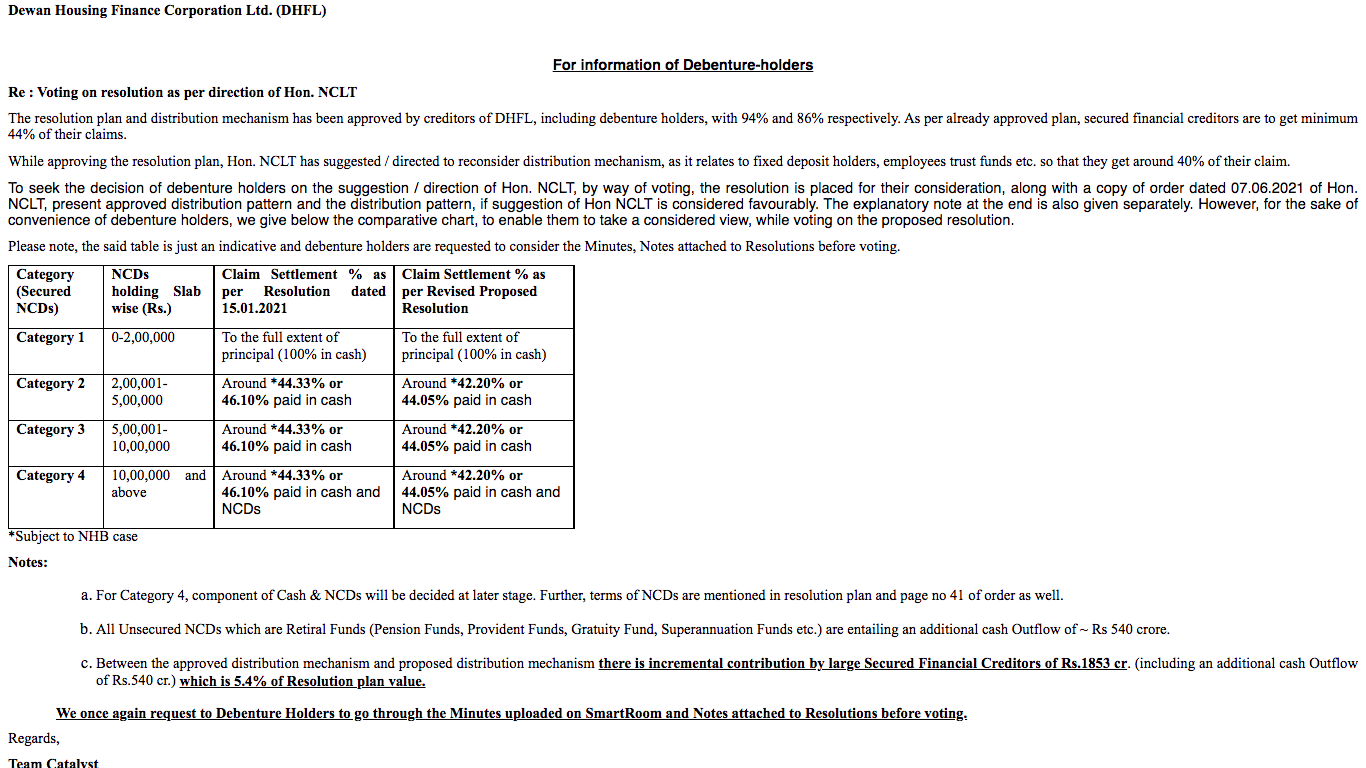

Matches with what I understood yesterday. 100% payout for less than 2 lakh secured NCD holders. No change in it.

1 Like

- 89.19% of the financial creditors voted against the proposal.

- The large banks majorly have voted against the new proposal.

- At least 66% of the financial creditors must vote in favour of a proposal for it to be passed.

- Surprisingly, the fixed deposit holders and unsecured NCD holders have also voted against the proposal which would have given them more money.

Now what @Akash_Shah

Yup, this was known. In last COC meeting itself all banks had gone on record and indicated that they are against changing anything this late.

They took a vote because nclt “suggested” them to review it. Now this proposals are voted down, so original resolution plan will stand, Piramal will take over DHFL and they should start paying in next quarter.

I think this is the logical end to all uncertainty. Unless some court puts a stay on it again

Yes, too many twists and turns so far.

But I also think this would make the retail investors little cautious about NCDs from now on, especially the so called ‘secured’ part of it. But I didn’t find any mention of it in the NCLT judgement. Because all eyes were on the judgement as it makes it a case study for the future.

On the contrary, retail investor should actually consider investing in secured NCD, This is live example where both FD holders and unsecured NCD holders are loosing money, but at least retail secured NCD holders are getting capital back

NCLT judgement came in on 7th or 8th June approving the plan with some suggestions (like if possible look out for small FD holders and Army trusts and so on). COC voted on those suggestions and rejected it yesterday.

So I don;t think anything is left for NCLT now.

1 Like

Going back to the previous proposal means -

The defence group investors (which was supposed to get 100% as per the new proposal) and the retail investors having unsecured NCD and FDs (which were supposed to get around 40% against earlier 5% recovery) would now get lesser payouts?

Sir what if someone has invested more than 2 lakh in ‘Secured NCD’ of DHFL ? Is he also getting something back ?

Yes,

FD investor will get around 27% recovery regardless of investor type i.e. retail, institution, army etc.

Unsecured NCD holder should get 5% regardless of investor type

NCLT wanted COC to show some mercy to specific investors, but COC do not want to show any mercy

For investor holding more than 2 lakh of secured NCD, recovery is around 40%. So should get 40% of money back.

If you are holding more than 10 lakh, then part of it will be cash and part of it would be instrument from Piramal.

Very well said. It is just noise there. Even trending topics have no meaning and forgotten within 24 hours.

1 Like

what is the recovery rate for secured ncd investors ( less than 2 lakh ) who did not participate in the voting process?