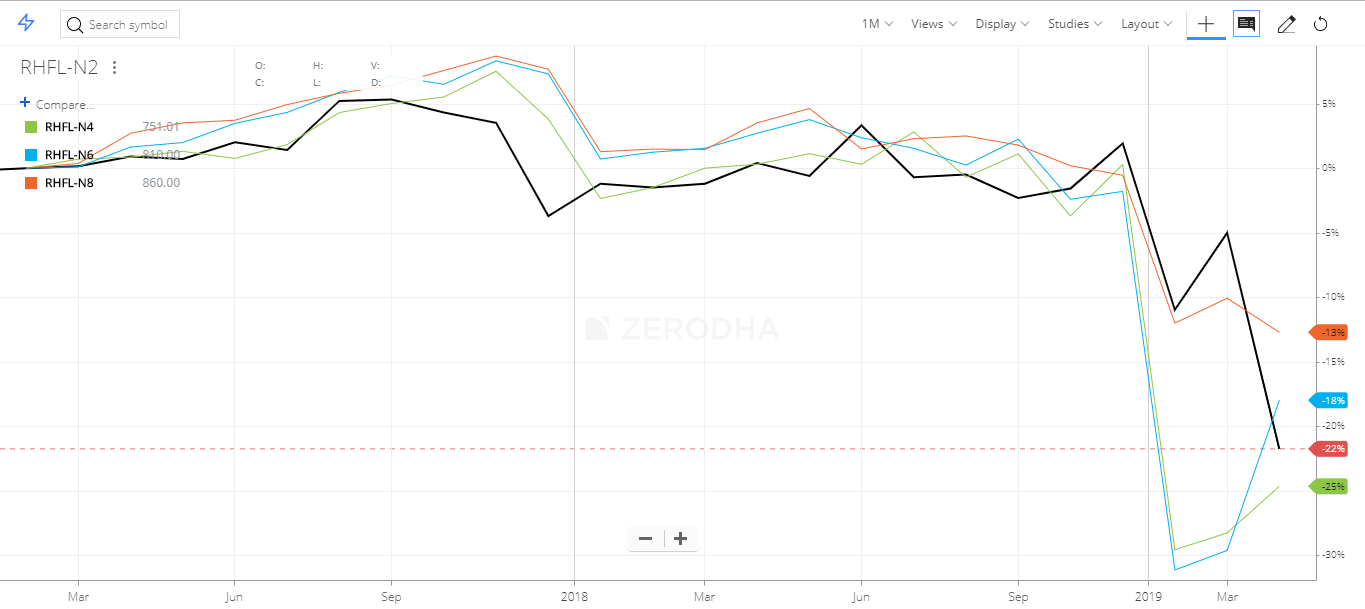

After IL&FS and DHFL, it now the turn of Reliance ADAG companies. In the past few days Ratings agencies have downgraded the ratings of Reliance Capital, Reliance Home Finance (RHFL) and Reliance Commercial Finance.

26 April

CARE Ratings downgrades ₹12700 crores worth of long-term bank facilities from BBB+ to D

CARE also downgraded ₹5,000 crore of debt issued by Reliance Commercial Finance from BBB+ to C.

CARE again downgrades ₹4980 crores of long-term debt issued by Reliance Home Finance from BBB+ to D.

₹12320 crores of debt downgraded fro BBB/BBB+ to C.

ICRA downgrades commerical papers issued by Reliance Capital, Reliance Commercial Finance and Reliance Home Finance commercial paper from ICRA A2 to ICRA A4.

Mutual funds have around ₹2600 crores of exposure to Reliance Home Finance and Reliance Commercial Finance.

What will mutual funds do now

Depends on how the mutual funds value the securities. In case of a default, they will have to write off 100% of the value and the NAV will fall by that extent.

How is interest paid in this NCD -annually , quarterly or monthly and from where we can get to know all the relevant details of the bonds which we are interested in.

Because someone got DHFL bonds when they had crashed and has already make a killing there? As per public reports, quite a few PE players were interested in purchasing these bonds from the secondary market.

I personally believe most HFC debt is a low risk investment since it is relatively easy to liquidate assets / loan portfolios at fair values to repay debt. Unless of course, the entire foundation on the company is built of fraudulent premises, then no money is ever coming back.

I have one query , when bond prices fell this much can’t issuer company buy back these bonds from secondary market and get some debt out of their books.

Even if they could, they will not be inclined or perhaps even unable to do it. When facing a liquidity crisis, buying back longer term NCDs - even at 50% off - will probably hurt their chances of survival. Case in point, CARE downgraded RHFL’s long term debt to D - Default because they are having difficulties coughing up principal payments of only Rs. 542 Cr. out of 16,000 Cr of Total Liabilities. So, its hard to imagine them finding cash for buying back the Debt/NCDs that are not close to maturity.

Bonds dont work that way. When a company wants to pull out its bonds from the market, this is called ‘calling back’ the bond. As per mandate, the company has to pull it out at face value only.