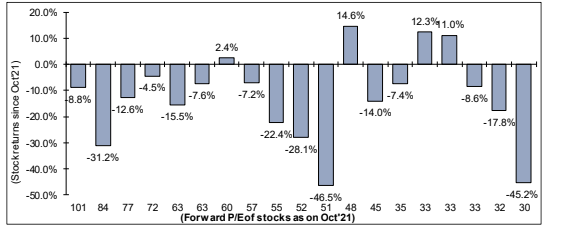

Quantitative tightening cycle triggered contraction in equity valuation for the NIFTY50 from ~23x in Oct’21 to sub-19x currently. Bulk of the correction in stock prices emerged from the low-volatility and expensive segment of the NIFTY50 (>30x forward P/E) concentrated around quality financials (insurance, NBFCs, private banks), consumption and IT.

The average forward P/E of the said stocks has dipped from ~54x in Oct’21 to ~39x currently.

What would be your comfortable buy zone based on PE for blue chip companies?

Also, in situations like above when do we decide to sell ? Because we have noticed in the past that some of the blue chips always remain expensive. Are there any factors which determine PE expansion or contraction?

Investment if doing long term is about the business, valuation metrics have to be looked at in the context of business, participation of institutions and retail, future growth, sustainability of margins, debt, performance of other sectors etc.

There is no single point of view w.r.t buying or selling, unless the investor is a value investor, who not only can come out of a overvalued business but also can find an undervalued business. Growth investing is relatively easy to value investing.

I don’t think there is a one size fits all kind of solution to this. Consider this - A stock trades at 30x, and going by a blanket approach, one can reject the stock, thinking it’s expensive. But what if the entire sector trades in the range of 25-30x multiple? PE is just one valuation metric, and basing your investment decision on this metric is not a good idea.

When evaluating an investment opportunity, you need to look at it from multiple aspects. Understand the business, evaluate moats, understand the risks, compare with peers, evaluate the price (and valuation), and choose to invest or reject the idea. If you are like me, then probably you’d want to look at the margin of safety while investing, which I guess not many believe in these days

The decision to sell or exit a stock investment should stem from your investment thesis. You’d have bought into a stock basis an investment thesis. For example - high profitability, low competition, high barrier to entry for new entrants, ethical management, new geographic expansion etc. All these reasons, along with reasonable valuations.

Post-investment, you need to keep track of your investment thesis. You hold on to the stock until the thesis holds, and you exit when you see a break in your thesis.