The above screenshot appears to be from

the Coin GSEC page - Kite - Zerodha's fast and elegant flagship trading platform.

A footnote on the above page explains Indicative Yield.

Indicative yields are annualized and based on the last traded price of G-Secs and are only for comparison purposes. The actual yield of the security depends on the weighted average price discovered in the auction. Learn more.

New GS refers to a G-Sec that is being issued for the first time. When a new G-Sec is issued, the yield is discovered through a yield based auction. Learn More

My understanding from reading this is as follows…

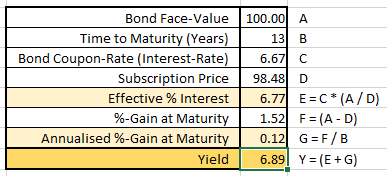

The Indicative Yield of a bond is an estimate of the yield

due to the estimated subscription price of the bond,

which is based on an estimate of how much under-subscribed / over-subscribed the bond is expected to be.

For example,

it appears that the 6.67 GS 2035 is estimated/expected to be subscribed at an average price (VWAP) of Rs.96.80.

(instead of the face-value of Rs.100).

Thus Indicative Yield of 667GS2035 = 6.67% * (100 / 96.80) = 6.89%.

Well not exactly!

This is just half the story - Returns from interest/dividend payments.

In addition to the interest payments,

Yield also accounts for the capital gains/losses on maturity.

For example,

if one bought a bond

- that matures in 5 years,

- of face-value Rs.100

- at say Rs.95.

Though one initially paid Rs.95, one would receive Rs.100 when the bond matures.

This additional Rs.5 gain (100-95) over 5 years adds 1% to the yield.

Thus, for 667GS2035 purchased in 2022 to provide a yield of 6.89%,

a reduced subscription price is necessary,

which will result in…

- a slightly higher effective rate of interest on the reduced subscription price.

- additional returns generated on maturity (diff between the reduced subscription-price and face-value).

…the 667GS2035 being estimated to be subscribed at Rs.98.48 implies an Indicative Yield of 6.89%.

Since, 667GS2035 is traded on the secondary market too (NSE),

let us quickly take at peek at what it is currently trading at…

Rs. 97.99. Hmmm…

That means if one purchased this bond on NSE today at the market-rate,

the effective yield one would receive would be…

(6.67 * (100 / 97.99)) + ((100 - 97.99) / (2035 -2022)) = 6.96% ![]()

The limiting factor to invest in this bond at 6.96% yield in this case,

would be the trade volume of this bond on the NSE.

( <100 units traded on most days of the month, and ~6500 units traded today)

To answer your question,

is this indicative is the highest i am going to get? or it might be higher also?

It can be higher or lower, depending on the actual participation of folks who bid for the bond till the close-date.