Given the 21 day lock-down imposed, there’s a lot of hue and cry over why the markets are open and there have been increasing calls to close them. There’s also a lot of chatter about banning short selling given the steep fall in the markets.

But do short selling bans help?

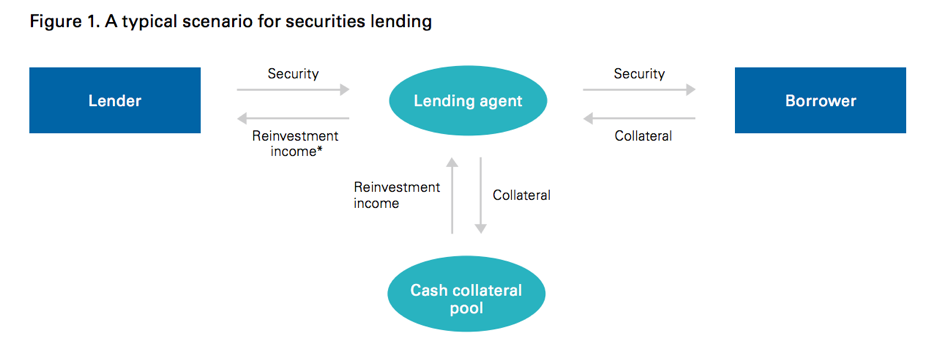

First, for people who aren’t aware, just like you buy a stock using CNC, you cannot sell it overnight. All short positions in cash markets are valid only for a day in India. To short sell a stock, you need to hold it in your demat. You can do this by borrowing a stock from someone who holds it. This happens through the stock lending and borrowing mechanism on the stock exchanges.

As a borrower, you need to pay an interest. You can check the current rates and bids for various stocks available for borrowing here.

But, the SLB market is tiny in India. Average volumes are between Rs 50 lakh to Rs 1 crore on normal days. Most shorting happens in single stock futures. So, when people want shorting to be banned, they are asking for shutting down the entire derivatives segment.

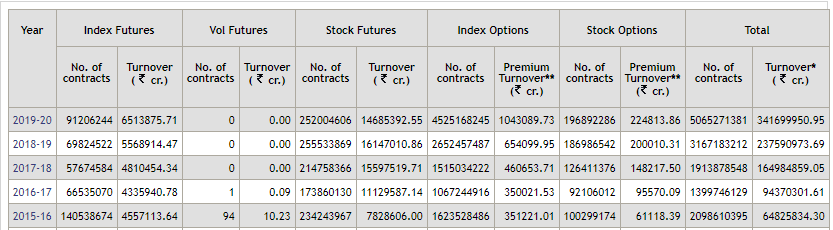

Size of the Indian derivatives markets.

That’s madness. And moreover, plenty of countries have tried some variation of banning short selling and it has always ended disastrously. I’ll cite some research. In 2008, the US financial stocks were battered and bruised and were falling as if they were going to zero. The U.S. Securities and Exchange Commission (SEC) imposed a ban on shorting financials. Here are two statements from the then SEC Commissioner in a span of 3 months.

“The emergency order temporarily banning short selling of financial stocks will restore equilibrium to markets” (Christopher Cox, SEC Chairman, 19 September 2008, SEC News Release 2008–211).

“Knowing what we know now, I believe on balance the commission would not do it again. The costs (of the short-selling ban on financials) appear to outweigh the benefits.

This study shows that banning short selling achieved the opposite of reducing volatility. Inf fact banning shorts led to poor liquidity, wider spreads, poor pricing of negative information,

Thus, with risk-averse investors the net effect of a short-selling ban on stock prices is ambiguous, and is more likely to be negative the greater the slowdown in price discovery induced by the ban. The prediction that a short-selling ban may aggravate a decline in prices, rather than prevent it, is also present in the model by Hong and Stein (2003), where the accumulated unrevealed negative information of investors who would have engaged in short sales surfaces only when the market begins to drop, thereby aggravating the price decline

This study by The New York Federal Reserve showed the same

Our analysis of the empirical evidence from the United States suggests that the bans

had little impact on stock prices. Even with the bans in place, prices continued to fall. At

the same time, the bans lowered market liquidity and increased trading costs. On the latter point, we estimate that the ban raised total trading costs in the U.S. equities options

market by $500 million2 in the period between September 18 and October 8, 2008

Shutting down the markets

A lot of people are making a lot of hue and cry over why the markets are open when the economy seems to be shutting down. This is another silly topic and I’ll explain why. Capital markets facilitate the allocation of capital from those have to those those who need. They also reflect the underlying realities of the companies and by extension, the economy and provide liquidity on demand. Equities is just one part of the capital markets, they are complex and have global linkages today. So, when people ask for a shut down of the markets, it’s not as if there’s a magic wand, you can wave to shut them down. There are real world impacts to the markets closing down. To name a few:

https://twitter.com/Nithin0dha/status/1242477360839942145?s=20

- All derivative contracts have to unwound. This is simply not possible. Everybody from FIIs to mutual funds have positions and unwinding them or just simply shutting down the markets isn’t an option without sufficient margin cover.

- If the markets are shut and positions carried over, the MTM losses can be severe and can cause far reaching systemic risks and failures to intermediaries including brokers when they reopen and if they fall.

- Promoters also pledge shares and obtain loans to fund various activities this will be shut down. And this also lead to a lot of margin calls etc, because upon reopening the markets have to price the gap. And if there’s a severe adverse move, the loan cover will reduce leading to more ripple effects.

- Companies issue long term debt and commercial papers to fund projects and working capital requirements including salaries etc. This has to be shut overnight. The holders of these debt instruments in the absence of a functioning market will be unable to hedge risks which will amplify systemic risks.

- India might be removed from global indices. The confidence of global investors in the openness and fairness of our markets will take a beating. This is like shooting ourselves in the foot.

From Prof. Jayanth Varma’s post

We need to remember that even as many economic activities shutdown, both individuals and companies have bills falling due. For businesses, revenues have evaporated but expenses have not. They still need to pay rents, salaries, interest and utility bills. The organised workforce might be still receiving wages and salaries, but in the informal sector and for the self-employed, income has collapsed. Monthly expenses still have to be met from some source or the other. Individuals and businesses, therefore, need to draw down their liquidity reserves, liquidate assets and raise new debt to keep making payments as they fall due. The only alternative would be a sweeping moratorium on all debt servicing and bill payments. The world has not reached that point yet, though some countries might need to consider that at some future stage.

There are real human costs to shutting down the markets, let alone economic costs.