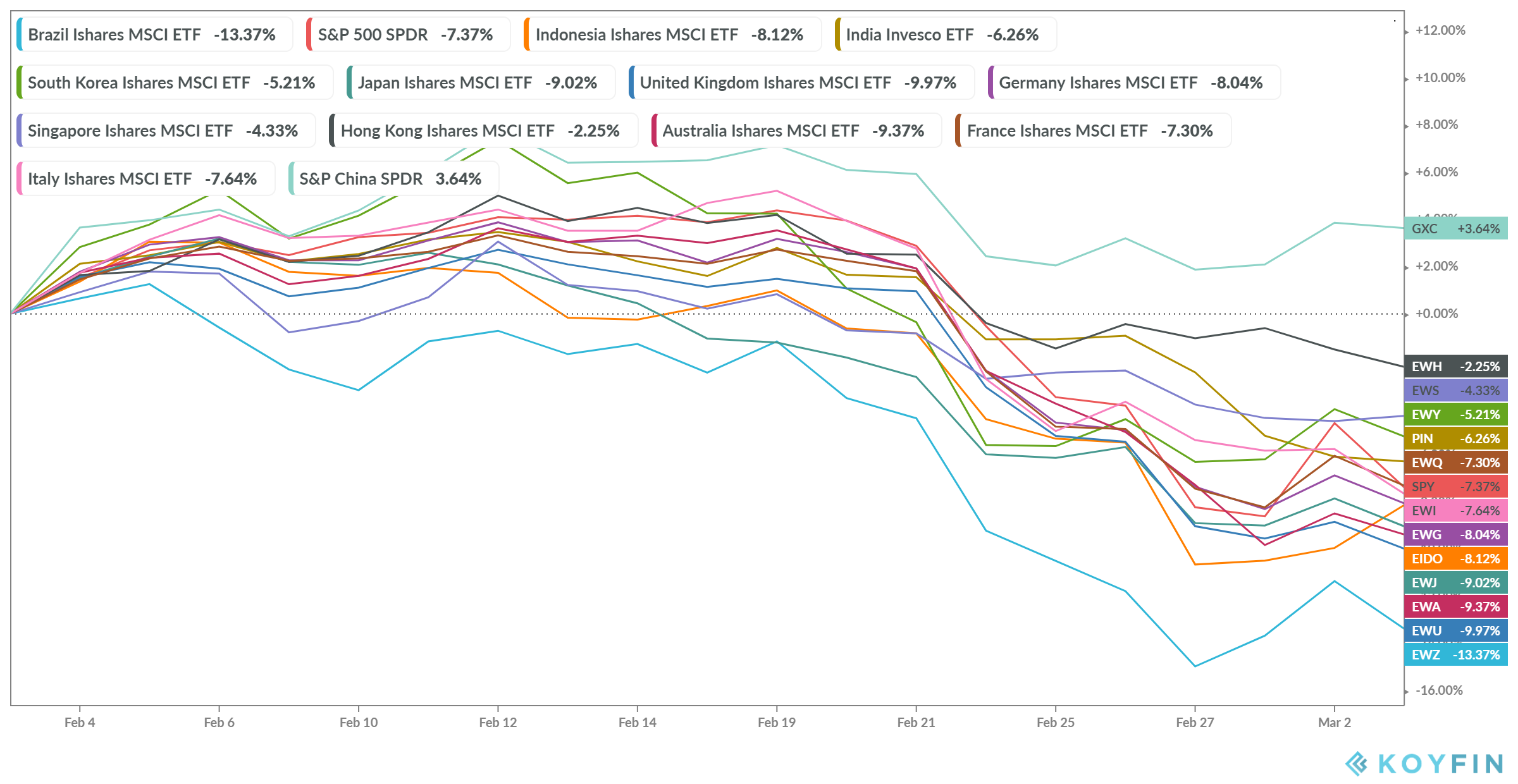

What a month it has been for the global markets. The sudden sell-off over the past couple weeks on the back of the Corona Virus fears has caught everyone off-guard. This sell-off is the worst since 2008, which a vast chunk of the current crop of investors haven’t experienced.

To sort of put that into context, only 12% of global stocks are trading above their 50DMA, down from 50% a couple of weeks ago according to data from SPDR Research. For a vast majority of people, it feels like the world is ending. If it really is, how do you invest? Here’s a perspective.

What caused the sell-off?

While you could attribute a million reason to markets crashing, these things are never easy. remember, we are living through an interesting time period. We haven’t had a market correction since 2008, and this one of the longest expansions in the US. Since 2008, pretty much everything has gone up and there’s a lot of complacency around the world.

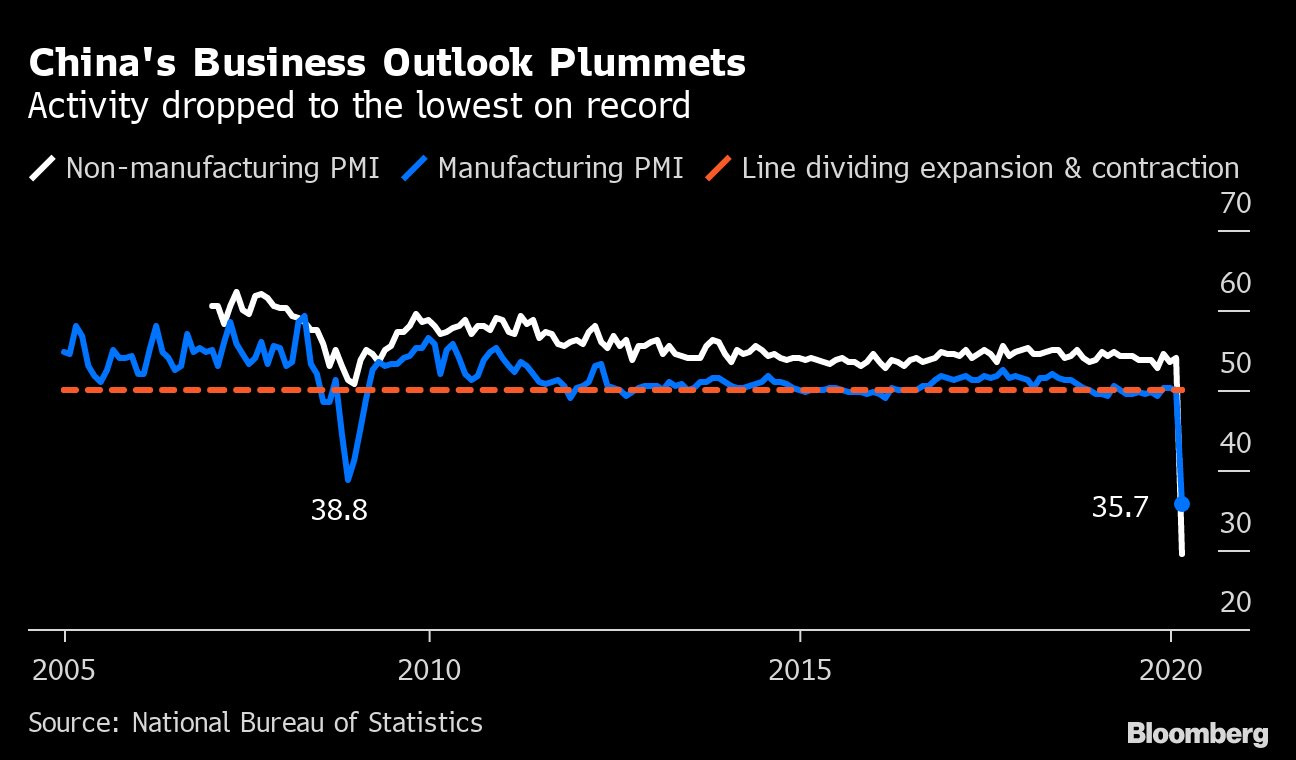

The markets reflect the views of millions of participants. But fears over the economic fall out from Corona Virus epidemic seem to have spooked the markets. A lot of economic data that has come in over the past month seems to point to a definitive fall in activity across the globe with China being particularly hard hit.

But, we’ll only come to know the true magnitude of the economic shock from this epidemic over the coming weeks and months as the outbreak spreads across the world. Global central banks have pledged to take the necessary steps to contain any downturn. The US Federal Reserve announced a surprise 50 bps rate cut yesterday, South Korea announced additional spending, World Bank also announced spending to contain the outbreak. It’s reasonable to expect more such moves from central banks. But given that interest rates are low to negative in most parts of the world, the amount of legroom central banks have is limited.

Interest rates for G20 countries

| Argentina | 40 |

|---|---|

| Turkey | 10.75 |

| Mexico | 7 |

| South Africa | 6.25 |

| Russia | 6 |

| India | 5.15 |

| Indonesia | 4.75 |

| Brazil | 4.25 |

| China | 4.05 |

| Canada | 1.75 |

| Saudi Arabia | 1.75 |

| Singapore | 1.36 |

| South Korea | 1.25 |

| United States | 1.25 |

| United Kingdom | 0.75 |

| Australia | 0.5 |

| Euro Area | 0 |

| France | 0 |

| Germany | 0 |

| Italy | 0 |

| Netherlands | 0 |

| Spain | 0 |

| Japan | -0.1 |

| Switzerland | -0.75 |

What should you do?

Some context first

I was recently listening to this podcast by Dr. Daniel Crosby, a behavioral finance expert and a psychologist and the opening of the podcast just stuck with me. What he says isn’t particularly a groundbreaking insight, but maybe it was the way he phrased. I couldn’t agree more.

Your brain couldn’t be worse designed to be an investor. There’s not one good thing about the way your brain is designed when it comes to investing. Your brain wants certainty, markets are all about uncertainty. Your brain hates risk, markets are all about risk. Your brain is made to optimize the here and now, markets require you to invest in an unknown future.

We humans are flawed creatures, more so when it comes to investing. We do a lot of dumb and silly things driven by our emotions and impulses. People often say, think rationally when trading and investing but that’s almost impossible if you ask me, we aren’t built be emotionless calculating and purely rational beings. At any given point of time, there’s a maelstrom of thoughts swirling around in our brains sending impulses designed to make us do really dumb things. I think the best we can do is to realize and accept this fact and stay cognizant when making investing and trading decisions.

And this is accentuated when the markets are turbulent like the last couple of weeks. Nobody can predict what’s going to happen with the Corona Epidemic. It might just slowly fade away over a couple of weeks the virus could mutate and become something else altogether and wipe-out half the human race by the end of the year. Anything is possible and you and I cannot possibly predict what’s going to happen.

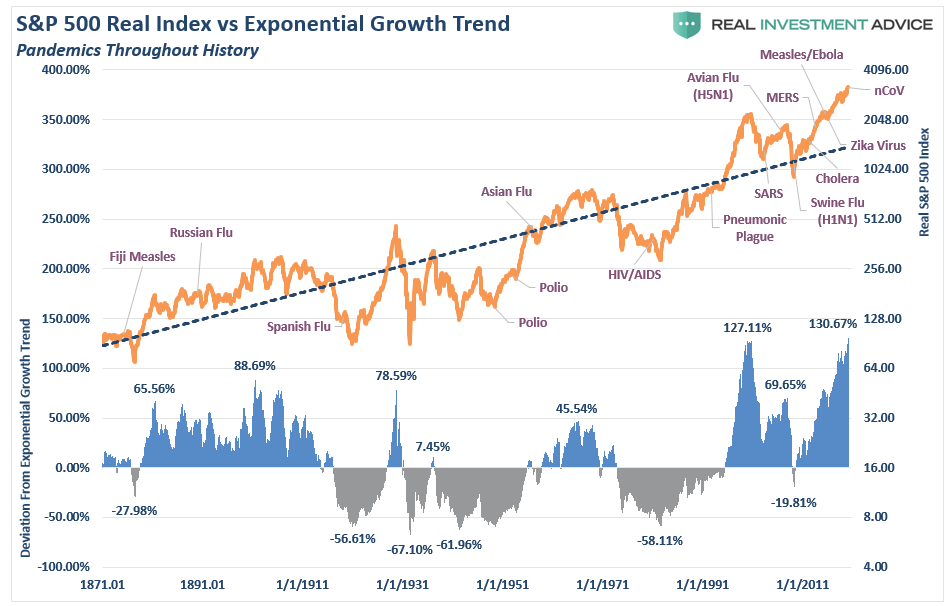

But history is nonetheless a guide, a weak one or a strong one, we could debate that until the crows come home to roost. Let’s look at what happened to the markets during previous outbreaks of diseases. Indian markets are quite young, so we’ll have to look at the US markets which have data going back to the 1800s. For context, the Nifty 50 index starts from 1996, and BSE Sensex for 1979.

Here’s how the S&P500 has performed through various epidemics and pandemics:

Source: SeekingAlpha

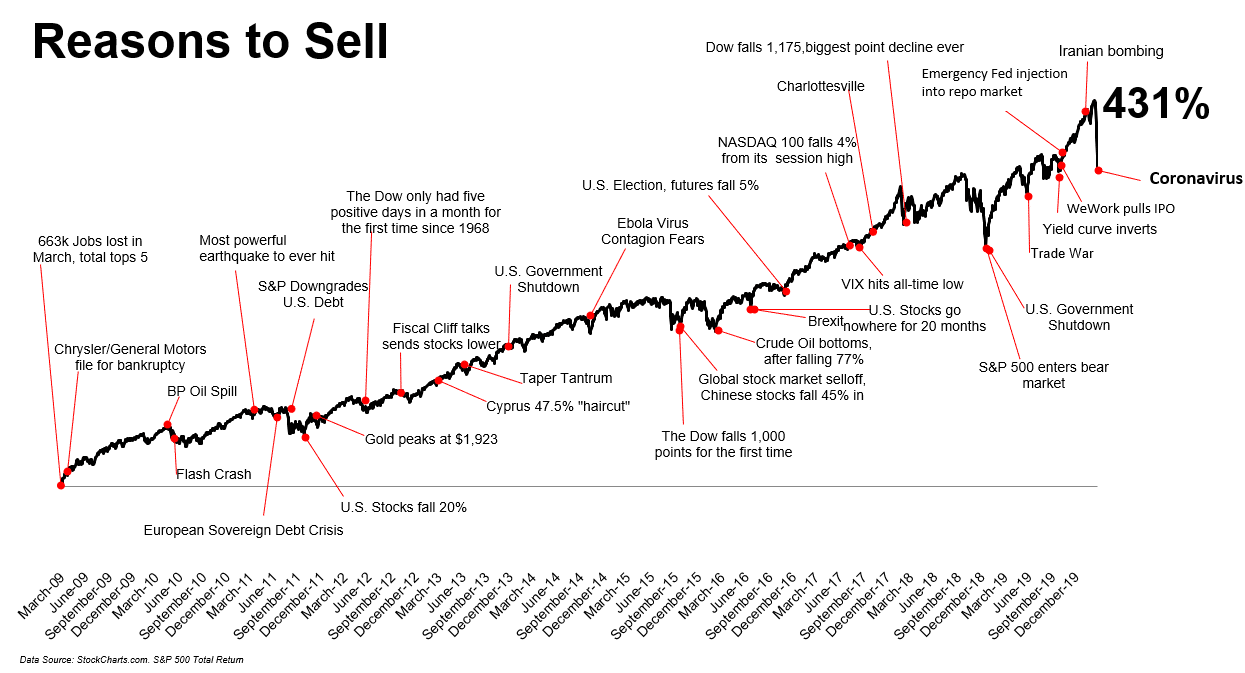

Another fascinating chart

Source: The Reformed Broker

I could say, buy and hold and everything would be alright, but that’s bullshit. Sure, the long term trend looks all nice and rosy but make no mistake, there’s usually a bloodbath in the short run and this is what we investors have a problem dealing with. Look at the peak to trough drawdowns in the bottom of the image.

Having said that you cannot control what happens to the markets. But you can control how you build your portfolio and behave during turbulent market phases. Equities are the most accessible asset class which gives you inflation-beating returns in the long-run. They are risky and can cause you to puke, that’s the reason for the existence of the equity risk premium, the premium the markets pay you to assume the risk of volatility.

Having said that having 100% in equities is stupidity. You need to have the right asset allocation based on the duration you are investing for and based on your risk tolerance. Asset allocation is an art and science. There are 100s of approaches to this and there is no one easy answer, all we can do is have a reasonable asset allocation that allows us to sleep peacefully at night.

What the hell is asset allocation?

Here’s the Wikipedia definition

Asset allocation is the implementation of an investment strategy that attempts to balance risk versus reward by adjusting the percentage of each asset in an investment portfolio according to the investor’s risk tolerance, goals and investment time frame.

The most commonly used asset classes are:

- Equities for growth

- Bonds for stability and income

- Gold as an additional diversifier and a hedge against inflation

The essence of asset allocation is to have multiple uncorrelated asset classes that don’t move up or down together. Let’s take a look at Stocks, Bonds, and Gold and see how they performed during 2008, which was the last crisis we say.

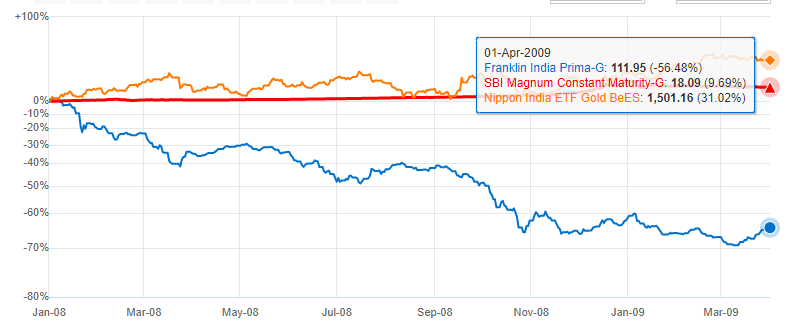

Here’s how Franklin India Prima Fund, Nippon Goldbees, and SBI GIlt Fund performed from Jan 1, 2008, which was the peak to April 1, 2009, which was the bottom. Notice that when equities (Franklin) was down by 55%+ stock and Gold were having a brilliant run.

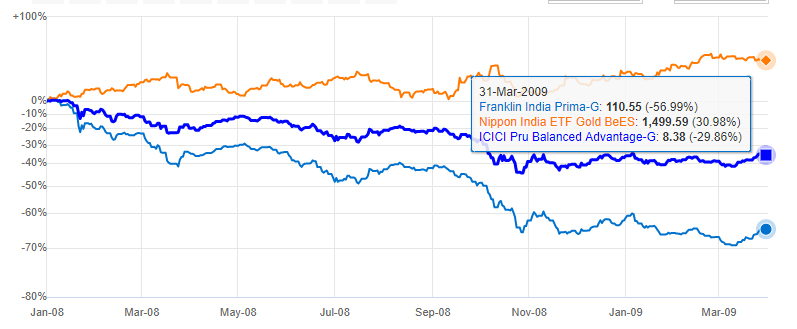

That’s what asset allocation means. Here’s the performance of ICICI balanced fund which has a mix of stocks and bonds vs Franklin Prima which is 100% stocks. You would be down by 30% as opposed to 55%.

Reason in being, the bonds in the fund would have gone up while stocks were going to the dogs.

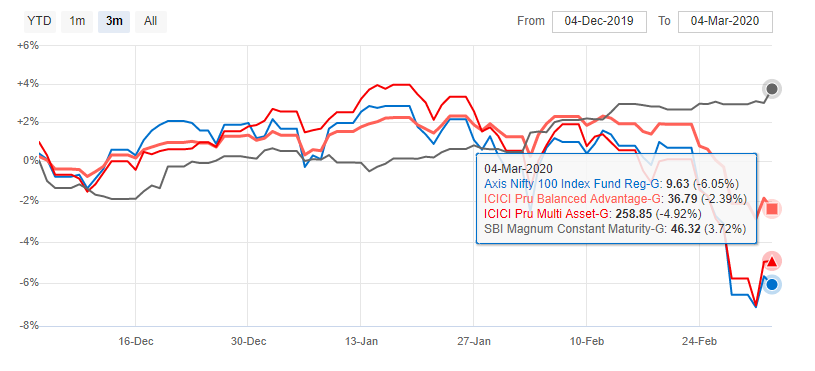

Let’s look at how this would have played out during Feb 2020 when the world was ending

Here are the returns of Axis 100 Index fund (100% stocks), ICICI Balanced Advantage funds (75% stocks, 25% bonds) and ICICI Multi-Asset Fund (68% stocks, 10% debt, 11% gold, 11% others), SBI GIlt fund and Nippon Goldbees.

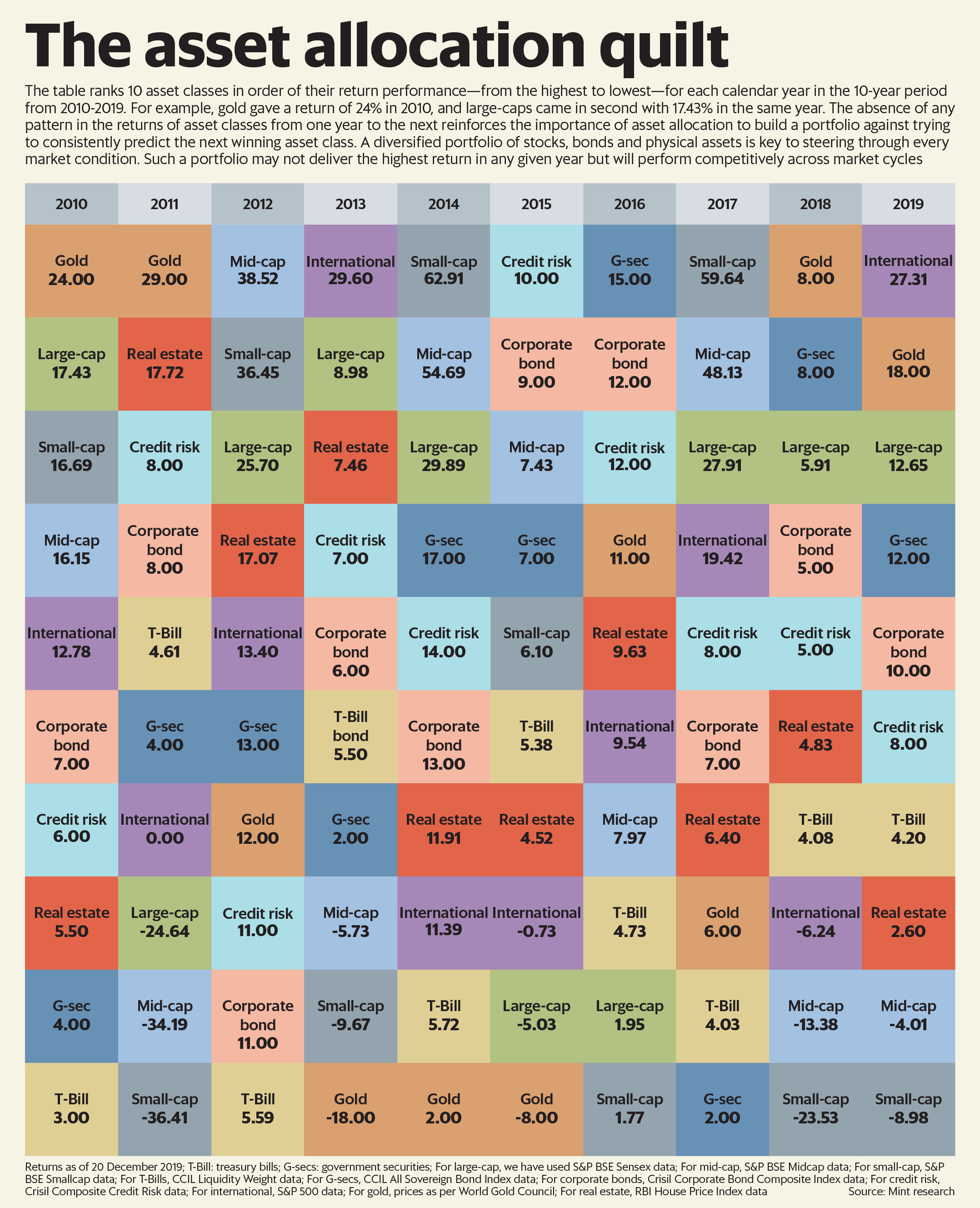

Here’s another interesting graphic, which shows the importance of diversification. Not just asset classes, you can diversify across style, regions, etc

All you can do is be prepared and let markets do what they do.

Diversification is a wonderful thing because (in theory) it should help you earn a given level of return at a lower level of risk (or volatility in this construct). But diversification isn’t just about portfolio construction. In fact, for the majority of investors diversification has little to do with Modern Portfolio Theory.

Diversification is a form of risk management in the investment decision-making process. It helps you live to see another day in the markets. It’s never too hot or too cold. And diversification can help you avoid panicking. When markets go to the extremes, as they are wont to do, holding extreme positions in your portfolio is a recipe for disaster. - Ben Carlson

Staying out, getting in

The impulse of timing the markets can be quite strong for most investors. Like other people, I am not going to say that it’s impossible, it’s not. But can everyone time the markets, HELL NO! The probabilities of you predicting a crash and recoveries very very tiny. Only the most skilled investors can get this right.

There are no rules for how these things play out, if there were, we would all be following them. The most important thing for investors that are worried, and that probably includes all of us, is to keep in mind that this too shall pass. It may be at lower prices, it may get more frightening, but this is what we signed up for. - Micheal Batnick

Which means, you are better of getting your asset allocation right than engaging in market timing. markets, have a mind of their own and the most often do the unexpected when we least expect it to. So better not to mess around by paying a heavy price

Markets can remain irrational longer than you can remain solvent!

If it’s any solace, it’s just not you, even institutions suck at this.

So, don’t try to do dumb things. Keep your behavior in check. I’ve always found it very helpful to write down on a piece of paper, the reason why I am investing. If you’re reasoning is wrong like expecting 20% in 1 year, then you are better of in a fixed deposit. ALWAYS, have a plan as to why you are investing with reasonable and achievable assumptions. If this goes for a whack, your portfolio goes for a toss.

There will be epidemics, wars and at any given moment the world will always seem like it’s ending. Maybe next time, it actually will, you don’t know and you cannot stop that, only Donald Trump can ![]() Believe me! The only thing you can pretty much do is not do silly things by following the short term noise.

Believe me! The only thing you can pretty much do is not do silly things by following the short term noise.