I don’t think so - I see substantial deprecation accounted for replacement of assets??

Depreciation as an accounting entry? Yes

Is cash retained on books which can be used in future? No

1 Like

PGINVIT is falling continues - I think it will touch 80 rupees

- no sense of dividend and stock falling Day by day

1 Like

Well, it is a freely traded asset. The market price doesn’t always reflect the underlying value. Perhaps someone wanted to offload a bunch of shares which resulted in the price drastically crashing. I also noticed that some of them were trading above market value which perhaps got corrected with the recent crash.

1 Like

During 30 year lease of either transmission lines or road lines for toll collection by corresponding invits, won’t they keep adding more assets to the list such that these invits run for additional years?

Suppose they get additional resources after 10 years which last for 30 years from then, it will be 40 years for us from now. Is this not the way invits in some other countries like the US work which started long ago? In this case, as long as we are getting profit share, why worry about the depreciation of current assets? If new asset additions occur even more slowly, forget about capital appreciation. Still, the profit distribution can continue for us and our future generations assuming these invits run for at least 50+ or sometimes 100+ years.

Not sure if Tesla’s wireless power distribution, air taxis, and flying cars arrive in the future as 50 years is too long for a fast technologically advancing phase of science. Of course, the Tesla wireless power distribution technology came long ago but got suppressed by elite people to avoid collapse and losses of their businesses.

Theoretically yes. But there is a limit to it and it depends on where will the money come for buying new assets?

Not sure what USA does, but currently INVIT (or even REIT) are not allowed to retain any earning on their book. They are mandatorily required to payout 90% of their cashflow to investor every year.

Since they do not retain money, they do not have more money to buy new assets in future. They can raise money to buy new assets by issuing more units, but that dilute existing investors and it expands per unit earning only slightly

OR they take more debt (there is a limit on how much debt they can take) but that too has limits.

Indigrid has been buying new assets using combination of both.

An INVIT can run for 100 years, but that does not mean original investor who invested at begining is still earning return ![]()

Chances are he is already paid back or got highly diluted and new set of investors have come in (or existing investor has reinvested)

So at the level of SPVs, individual SPVs cannot retain any cash? And for them too Depreciation will be just accounting entry? The 90% limit is applicable at SPV level too? or just at InvIT level?

Also, didn’t get this part? The Unitholder continues to hold fractional ownership (maybe diluted) till the InvIT continues to own Assets Right? Or once the Capital is paid the ownership ceases to exist?

At both level

Yes, ownership does not cease but it becomes so tiny that after a point it is inconsequential.

Let me explain it in a slightly better way. Assuming INVIT has an asset with life of 30 years. If you put in rs. 100 at start your cash flow will keep on reducing over the life as follows, assuming no new asset is bought over (Just an example … not actual numbers)

| Year | 1 | 5 | 10 | 20 | 25 | 30 | 31 |

|---|---|---|---|---|---|---|---|

| yearly Cash flow (rs.) | 10 | 9 | 7 | 5 | 3 | 1 | 0 |

Now, if INVIT continues to raise additional money and keep on buying additional assets, your ownership continues for extended period of time, but since youa re so much diluted, your returns would be inconsequential. Something like follows

| Year | 1 | 5 | 10 | 20 | 25 | 30 | 31 | 35 | 40 | 50 |

|---|---|---|---|---|---|---|---|---|---|---|

| yearly Cash flow (rs.) | 10 | 9 | 8 | 6 | 4 | 2 | 1 | 0.5 | 0.3 | 0.2 |

Again these numbers are just an example to show the drop, and not actual numbers (that will depend on lot of factors including what asset, how it is bought, how much dilution etc.)

The point I am trying to convey is that you paid money at the beginning to buy an asset and you will get returns in form of cashflow generated from that asset. Once that asset is done with it, more or less your returns are also done.

INVIT can keep on buying new asset with new money and prolong its own life, but that does not meaningfully increase original investors return beyond a point.

Also, one clarification - this is a concept and this is how INVIT will behave in long term. Capital appreciation in short term is different and that might happen due to drop in interest rates or some market euphoria because of “news” that INVIT is buying new asset.

3 Likes

Thanks for Reply @Akash_Shah

This reduction you are speaking of is due to raising of new equity, right?

But how drastic is the drop in FCFF over say 28-30 years in case of no new asset is bought?

And how accurate (or Trustworthy) are their projections of Future Cash Flows? Considering the TSAs are long term and most of the TS charges are fixed or based on a predetermined formula (I am not considering the exceptional repair costs that might occur in case natural disaster or exceptional litigation costs).

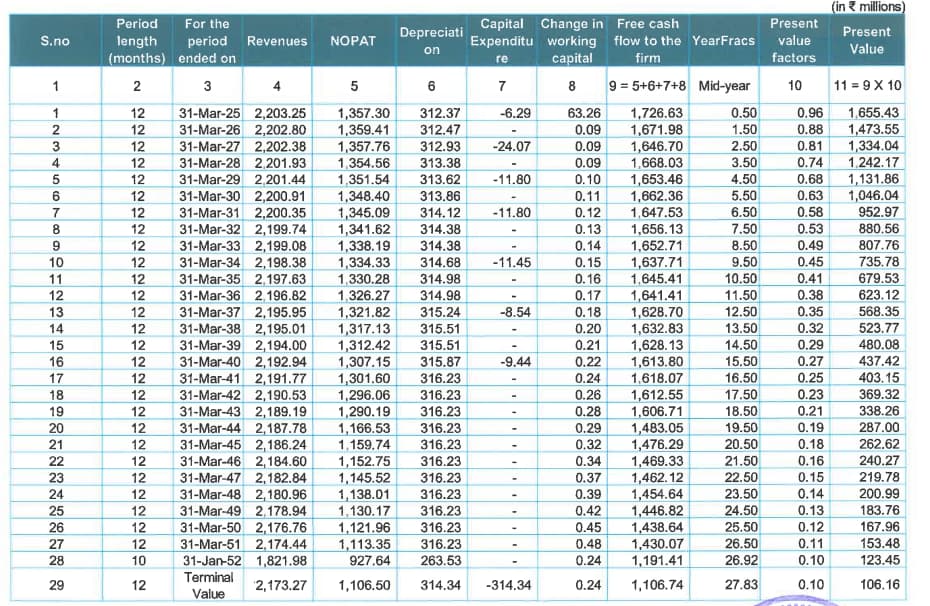

For example, in case of PGInvIT the reduction FCFF (Management’s Projection) drops by ~33% over period of 28 years from ~172.663Cr to 119.141Cr. In case of other SPVs the is around 50%.

OR is this just their Excel Sheet Wizardry? ![]()

1 Like

No I was trying to mimic the reduction in Free Cashflow of projects, reducing the distributable amount.

Completely depends on Asset and what Kind of contract it has. Each SPV contract would be unique and have variations involved in payment term.

Eg. for Grid asset, cashflows are high at beginning and tapers down near end.

For road asset, it is low at beginning and increases towards end (as toll and traffic both increases over period)

For grid asset, I would agree with what you said, these projections are generally reliable, unless some exceptional conditions arise.

For Road assets, I would never trust those projections. Govt has a habit of over projecting traffic data.

1 Like

You meant the Cash with InvIT post quarterly payout? You were using this (Cash post Payout) as a proxy for % ownership?

1 Like

I see the valuations mainly on predicted cashflows. Ignore depreciation etc since that doesnt effect cashflows. Terminal value can be set at 0.

Current selling has most likely a forced seller. Else why wud u sell fpr 89 thst which pays 12 next year and on average about Rs 8 per year over next 25years.

Quite long now

2 Likes

InvITs trading below their P/B value may indicate market skepticism about their future growth or cash flow potential. It could be due to factors such as rising interest rates, sector-specific challenges, or changes in investor sentiment.

Just stumbled upon this thread and couldn’t resist replying.

Now at 81.5

1 Like

Yes but u have received 6 rupees so avg price lower to 83 from 89.

Bot some today at 76.4. Heavy selling still.

Yes and that 6 rupees is supposed to be yield for investing your money, and not for adjusting price ![]()

INVIT is supposed to be a debt instrument and not an equity.

You are investing in INVIT so that you get a periodic cashflow, if end of year you get 12 rs. as dividend and price falls by 12 rs., then it is useless as you didn’t earn anything in a year.

Invits are neither pure equity nor pure debt. They are hybrid kind of products with regular income plus some scope for capital appreciation. Decline in unit price of pginvit is because of uncertainty of asset addition. That said, existing assets will continue to pay dividends. Currently this invit is paying Rs 12 per unit per year. In case of no new asset addition it will not be able to pay more than Rs 9 per year per unit from FY 28 and onwards. At the current price the yield will still be much more than Bank FD rates.

That is not a correct way to look at it.

Banks are paying 7-8%, but they return the capital at end of FD tenure. Same is not case with an INVIT. There is no concept of capital return at the end. Part of capital is being repaid every quarter and terminal value is going to be zero.

So INVIT is supposed to give higher yield to break even.

For eg. a bank pays 7% for FD and returns the capital at end Vs. and INVIT which pays 10% but returns 0 at end of tenure, which one is better amongst two?

There is no way to tell unless you run the NPV or do some other math.

2 Likes

So what will happen to the price , say if i buy Indigrid Infrastructure Trust Unit , presently trading at Rs.143

I cannot really predict the prices, else I would be very wealthy ![]()

But conceptually as it nears end of life (say 30 years) price will tend to zero.

However, Indigrid is managing its portfolio well and constantly buying up new assets, so it is somehow able to maintain the dividend and hence maintain the prices. This is kind of supporting the price.

Unfortunately PGINVIT is unable to do same, and hence the drastic reduction in price.

But again, I am only talking about concept. I cannot predict prices, especially in short term.