You can read the full article @ http://keepinvesting.net/index.php/2017/05/13/fixed-deposit-vs-debt-mutual-fund/

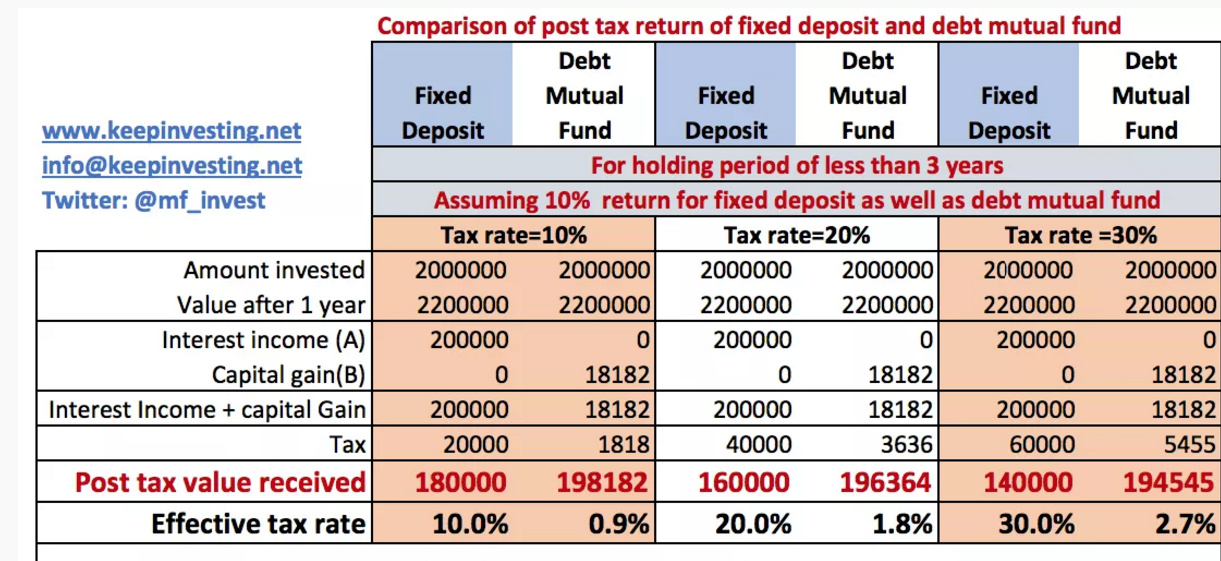

If the holding period of debt mutual fund is less than 3 years, then the tax calculation is similar to FDs that is as per the slab rates. the calculation mentioned in the article is sort of misleading in a way.

A major disadvantage with FDs is that, there would also be a TDS applicable incase your interest is more than Rs 10000. In case of debt funds, there is TDS applicable and you would have to pay tax only on the capital gains. Moreover, tax is paid for the interest earned on FDs every year but with respect to debt funds, the tax is paid only on the sale of the mutual fund units.

The returns generated from liquid funds (negligible risk compared to other debt funds) is significantly much better than the returns from FDs so even if they were taxed in a similar manner (assuming you sold your units within 3 years), the post - tax returns would still be higher than FDs.

If you have sold your units after 3 years, LTCG will be applicable at 20% after indexation. Indexation means to adjust the cost of purchase as per the inflation index number which the government releases every year. Lets assume, you purchased a unit at Rs 100 in 2017 and sold the unit at Rs 150 in 2020. Also, cost inflation index is 1000 for 2016 and 1200 for 2020 respectively. Then indexed cost of acquisition is (100*1200)/1000 is now Rs 120. The capital gains post indexation is Rs 150 - 120 = Rs 30 (instead of 150 - 100). So, 20% tax on 30 is Rs 6 per unit.

So, if you fall in a higher tax bracket and want to sell your investments after 3 years, then it makes more sense to invest in debt funds rather than FDs.

1 Like

Thanks @faisr

For such a detailed explanation,Even I thought the calculation is misleading but still wanted to get confirmed from the Zerodha community if there is any truth behind this.

Also would like to know, what is the impact on short term debt funds of financial crisis like we saw in 2008

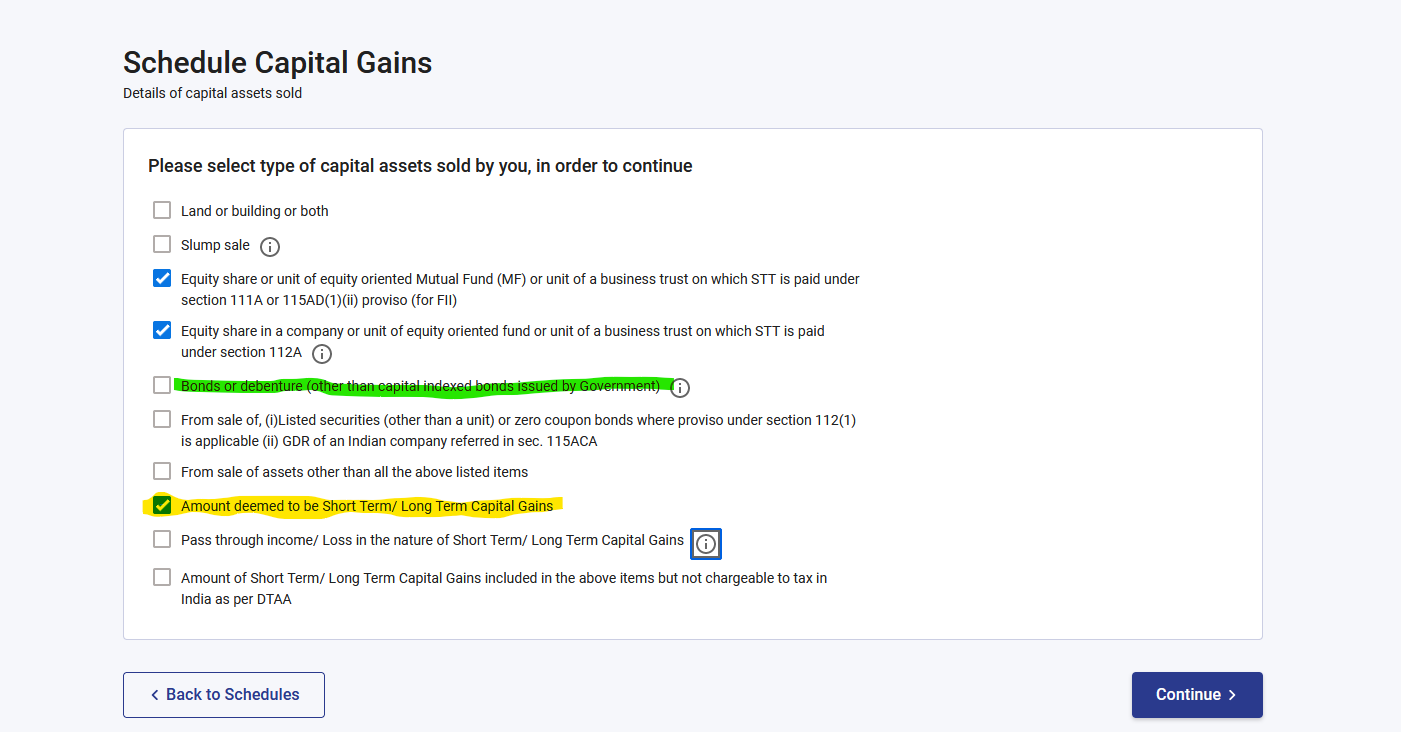

Can anyone please help me with which section do we mention the profit realised in short term from a debt Mutual fund?

Do we take it from Yellow or Green?