mirae. axis charges are high

Yes putting a lien on MF in demat is not possible for a third party. blindly deciding to put all money with ZD was a stupid mistake - a realization keeps getting stronger each time

1 Like

Hi @Quicko

If loan against securities/ mutual fund is taken and using this amount if Gilt funds are bought which are further pledged for collateral. Fno trading is carried out using this collateral. So the query is can this payment of interest on loan be treated as business expenses for lowering the profit and calculation of tax accordingly.

1 Like

Why you want to invest in Gilt fund by taking loan? Return on Gilt fund is less than loan interest, directly you can pledge orginal mutual funds right?

I will try elaborating it this way:

- Say I already own Gilt funds + some other mutual funds worth Rs. 5 lakhs

- I get loan against the above for say 3 lakhs with interest on loan say at 11%

- New Gilt funds worth Rs. 3 lakhs are bought from this loan amount

- These new funds are pledged for collateral from intention of doing fno trading… serving as margin money for option selling

- Now say original set of Gilt funds provide returns of 7-8%, so that way I will get around 14% notional returns by doubling the quantity

- If fno trading is done methodically and it turns out to be profitable, this profit coupled with returns as in #5 will be higher than the interest to be paid as in #2

- It’s a known fact that interest rates are at peak and fed / rbi will begin the rate cut cycle which will increase the Gilt fund returns substantially

Now the question is:

- Is it allowed to deduct the interest payable from the profit generated @Quicko

- Has such complicated arrangement worked in past… noobs in this forum may kindly opine @Jason_Castelino

Never trade with borrowed money.

Your entire thing is resting on the logic of making profits.

1 Like

So, you will get the return of 14% by doubling the quantity but you need to pay 12% interest on loan. Net return will be 2%. If you don’t take loan, your return will be 7% right.

You will get margin on 3L for F&O if you take loan, otherwise you get on 5L, here also you are loosing.

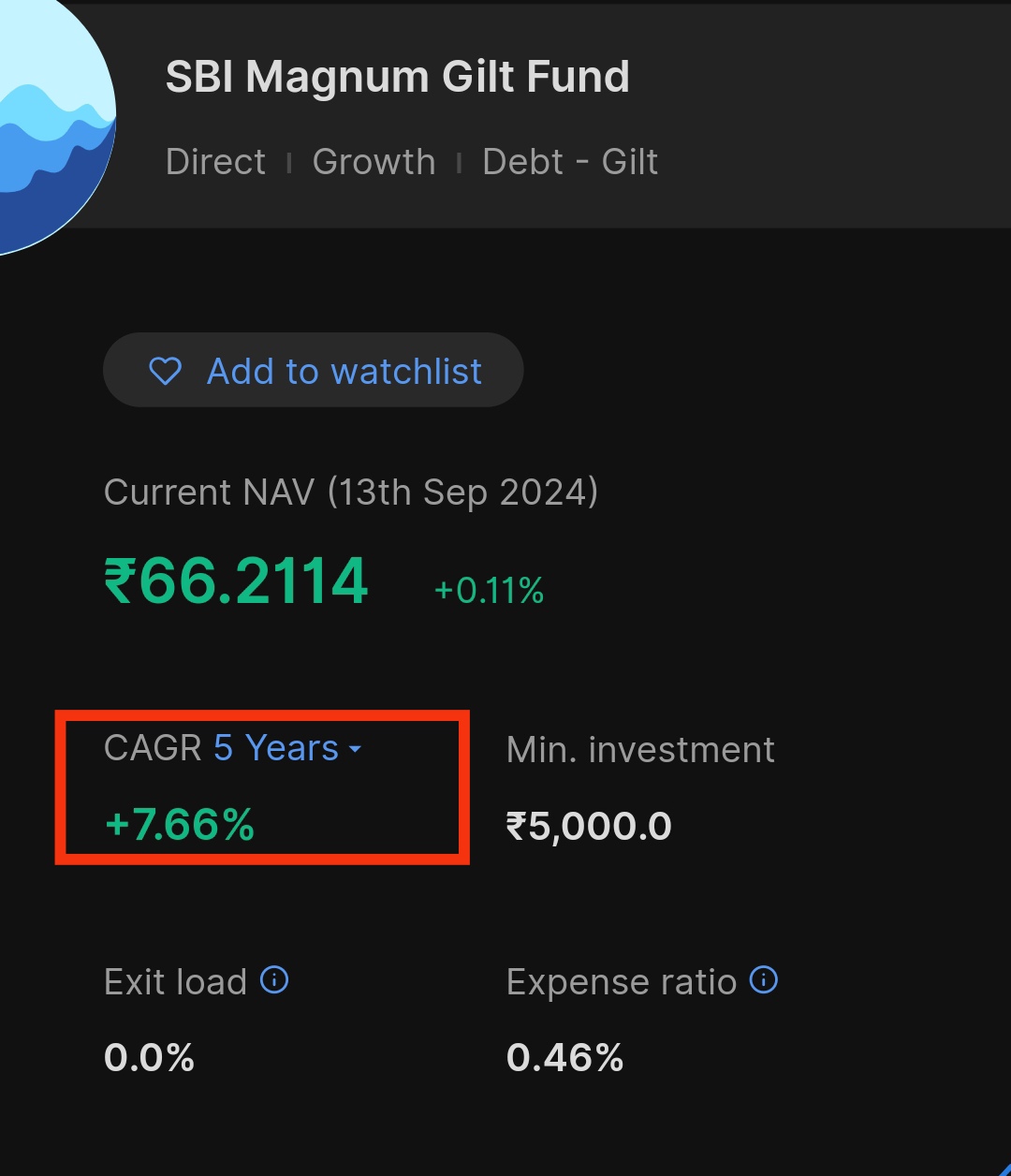

See basically objective is to utilise this opportunity of peak interest rates expected to be cut in near future. So in case of even 0.5% rate cut, returns from Gilt funds (considering their modified duration of 7-8 years) will be 3.5-4% in addition to their normal 7% I e. around 10%+ as observed during previous rate cut cycle.

So effectively doubling it to 20%+

Loan is procured at 10.5% as it’s a secured one against the mutual fund

So here net interest gain of 8-9%

Regarding trading strategy…well that is simply very very conservative risk averse say selling a weekly nifty strangle with 90%+ pop with ROI of around 0.5% a week

I know sounds extremely complicated and infeasible… But maybe workable with rule based trading with discipline … iota of luck ![]()

…and what does the math look like in the scenario in which

interest rates are not cut as per the timeline you have in mind?

(or say they go even higher due to some other unforeseen event in the near future)

You mean like gambling? ![]()

Only when interest rates increase, this setup will fail. Even delayed rate cut may be sustained due to marginal out performance from doubling effect.

Not a place for Gambling, but luck factor is like a chocolate… always welcome ![]()

I believe you could benefit from this price increase of gilt fund during a rate cut, only if you redeem during this short term when there is a spike in demand.

IMO, If you stay invested in such gilt funds, it would eventually average out the returns bringing it close to normal expected return, is it not?

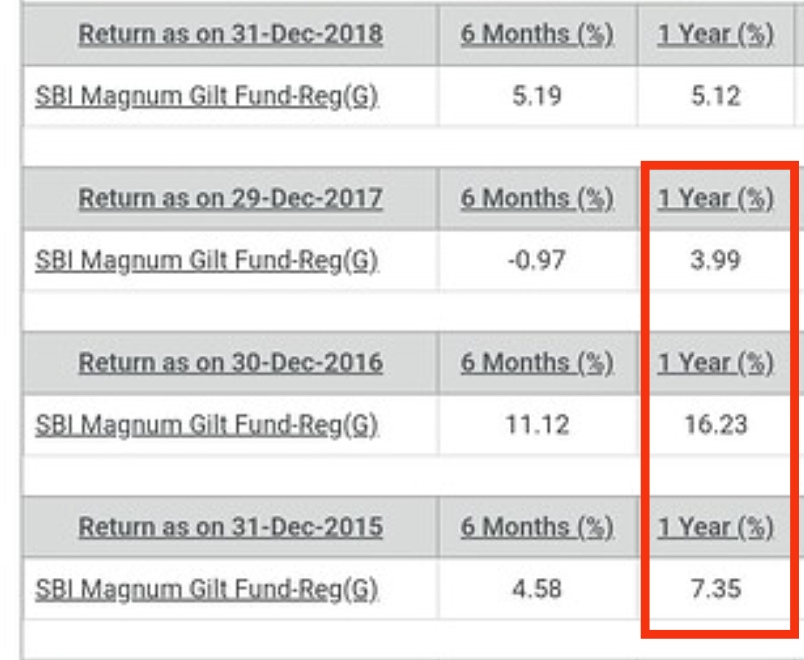

My thesis is based on past returns from the period of 2014 from when interest rate cut cycle began till I think upto 2017-18, momentarily paused and then again upto 2020 when interest rate cut cycle bottomed out.

This was the best period to cash in on nearly double digit rolling returns in an around 10%+

So expecting similar phenomenon to repeat.

Source: Mutual Fund Rolling Return | RupeeVest

Inflation is staying in comfort zone target of RBI and very likelihood of rate cut cycle to begin either by October or December

I was just referring to the fluctuations in the return.

Knowing when to exit is key to reap the benefits of price increase due to rate cuts.

1 Like

Yes that’s true, but it is generally observed that from rate cut cycle to bottoming out takes around 3-4 years… then the trough period of around 1-2 years… depending on inflation trajectory… so we have a good time cushion.

Once we get the indication of reversal as they are now…we take the action expected pursuant to that situation.

So essentially I am handling 3 things here

- Harness Leveraging power

- Logical entry / exit in long term debt fund

- Most risky part of high probability fno trading with very minimal RoR ~ 2% a month

Major query still stays that whether interest on payment of loan can be shown as business expenses and if deducted from the profit from fno (if I stay profitable).

Why not?

Any expense incurred solely for the purpose of the business is eligible to be claimed.

Assuming in your case, such borrowed funds are used for investing in debt, which in turn gets pledged for margin, interest on such borrowings would qualify as a business expense.

@Quicko can confirm this.

First milestone achieved… Tonight US Fed cuts rates by 50 basis points.

Will RBI follow the suit ![]()

Yep, 0.25% of the loan value is one of the lowest processing fees charged in the industry, if not the lowest. The standard processing fee generally varies between 0.25% to 1% of the loan value.

2 Likes

What’s are the charges for pledging additional units to makeover the increased LTV ? And can I pledge different fund for this time or it needs to be the same one as before ?

@Esha