Any plan to increase maximum loan amount limit from 25 lakh in nearby future. Secondly if the value of shares rises, how can we get additional borrowing against same.Lastly is it possible to pledge shares from other demat accounts too.

- Yes, we will up the max limit to a much higher amount. Restricting this to 25L since its beta.

- We will build a workflow for this in the future, but for now, this won’t be possible.

- Not on an immediate basis, but should be possible soon.

1 Like

What will happen if the pledged stocks lose 30-40% in value

Thanks.

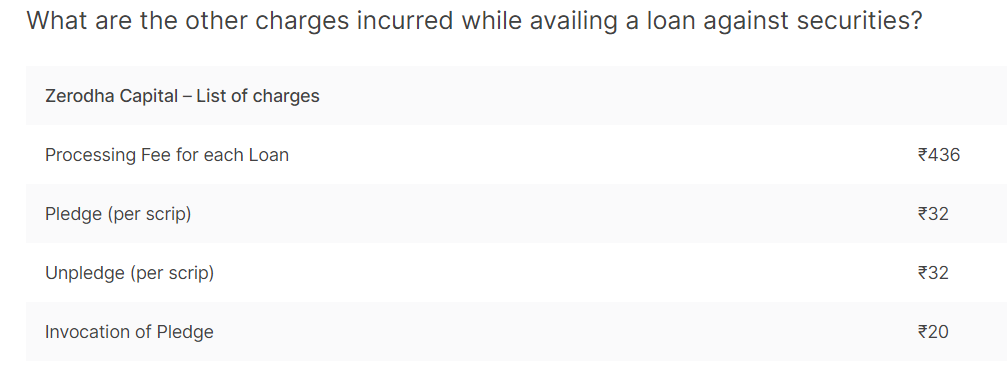

Can you please guide us about the annual service charges for using LAS, processing fees to apply for loan, etc involved in the process.

1 Like

As per the RBI regulations, the borrower is expected to maintain a 50% LTV during the tenure of the loan. When value of your securitues falls, LTV will increase.

To bring back the LTV to 50%, you either need to pledge more securities or repay part of the loan. If you don’t do either, then the NBFC can invoke the pledge and make good the difference by selling the securities.

For detailed explanation, you can refer to this FAQ.

2 Likes

Charges are as under, we have listed this under FAQ’s as well -

The processing fee of Rs.436/- is inclusive of Rs.200/- for stamp paper and18% GST applicable on the stamp paper.

There is no yearly AMC or any other charges involved.

A much awaited product thanks

Assume i have a holding of 10 lakh and i pleadge it to NBFC the maximum loan amount i get is 4.5 lakh cash

After i get the loan amount

Can i put that cash in my trading account and start intraday trade, or use that cash to fund any physical business?

How much is daily percentage of interest ?

Please enlighten

After the funds hit your bank account, NBFC has no further trail as to how you utilize the funds. However, as per compliance, you have to state the purpose against which you are borrowing the funds. We have made provisions to collect this information from the borrower in the workflow.

On a side note (purely from personal experience), it may not be a great idea to trade intraday with borrowed funds. I’d advice you against it.

At present, the interest rate is 10.5% per year or 0.028% or 2.8 Paisa per day for every Rs.100 borrowed.

7 Likes

@Karthik quite an expensive affair I must say and cumbersome to use from UX pov and recurring charges every time you take a loan. When my Demat account was with HDFC Securities I had enabled LAS service. Rs 1200+ taxes was the AMC. No other charges. No pledge charges for each script separately. Once the LAS was enabled, an overdraft current account is being added to my bank savings account with an amount equivalent to the value of pledged shares (value gets updated fortnightly). Now, whenever I needed money, I could transfer money from this overdraft account to my savings account, and instant liquidity was available. No processing fee. No charges. Every day at the end of the day interest was calculated and the interest amount was debited from the balance of the overdraft account. So easier to know how much I need to repay. If I transfer money from the overdraft account to the savings account in the morning say at 10 am and transfer it back to my overdraft account in the evening say at 5 pm, it does not incur any loan interest amount is repaid on the same day. Rs 1200+ taxes was all I was paying for a year for this convenience of a handy emergency fund.

@nithin please take a note

1 Like

Out of the 436, 200 + 36 is towards stamp paper and GST. Our charges are 200, and we have additional overheads here, right from kyc to your credit score fetch. We take in all these costs. I don’t think it is possible to go lower than 200 for processing.

While I’d not like to comment on how much others charge, please do have a look at HDFC’s list of charges

Besides, most of the players also have higher interest rates. By the way, other players are also restricted by the transfer agents (in case of MF pledge)…while we don’t have any restriction on that.

3 Likes

Other charges are for other services. e.g. they are accepting NSC, Kisan Vikas Patra, etc for pledging. Those are premium services I would say. I am not comparing apples to oranges. All I mentioned was pledging shares to create an overdraft loan account and use that money as a simple handy emergency fund to withdraw as per need (ease of use by transferring from overdraft account to savings and vice-versa).

I am sure HDFC bank’s loan against shares interest rate would be cheaper than any NBFC which usually has a higher interest rate.

I agree with you on this, that’s the advantage of being a bank ![]()

On that note, comparing a bank to standalone NBFC won’t be an apple to apple comparison.

As far as the interest rate goes, maybe you should check with the bank to understand the offer to a regular customer.

1 Like

you can get a loan against FD @ 6% in SBI.

why take a loan against securities @ 10 %?.

Loan against FD is a different product altogether. Typically, the banks make a risk free spread here. Suppose they offer you interest of say 5% on your FD, then they will lend you cash against your own deposit and make 6% from you. For the borrower, the primary purpose of booking an FD is lost and you make nothing, rather end up paying the bank interest.

In LAS, the borrower does not lose the primary purpose of his investment. The shares of MF units continue to grow, you continue to reap the benefits of corporate actions, while at the same time, without disturbing the wealth accumulation process, you have a line of credit to meet your other financial requirements.

4 Likes

Then why does a bank provide this product if the primary purpose of booking a FD is lost?

My point is if i want to get a loan irrespective of from where and how i get it. i expect to get it at the cheapest rate possible. in this case loan against FD would serve that purpose.

The primary purpose is lost for the customer, not the bank ![]()

Banks love this product!

Yes, it makes sense if you look at it purely from a cheap loan perspective. But as a good practice, you need to consider both the long term and the short term consequence of borrowing and the overall impact it has on your finances.

3 Likes

Knowing that Zerodha can’t compete with banks, it certainly can compete with the apps like Cred and Mobikwik etc which are giving instant credit loans. What is Zerodha’s edge on them? I would speak for myself, after having experienced HDFC overdraft loan account I am sort of disappointed with what Zerodha is offering. Faster and instant cheaper loans are available on these payment apps and loan-specific apps like Dhani etc. A salaried person can also get an overdraft facility in certain banks based on his salary. With such options available, Zerodha capital seems like too late, too little.

If I have to think for investors, I would think of how investors keeping funds in Zerodha trading account can earn interest. Don’t suggest liquidbees. That’s a shit product for retail investors. Can funds in the trading account be used for P2P lending to other zerodha user to earn interest. If current regulatory rules don’t allow a straightforward way, then rules can be hacked, bend, or mend to make things happen. Just about willful thinking to innovate. That’s missing.

2 Likes

Yea. Except kite all other products of zerodha is just like normal in market… Without any collateral one can get loan at 10.5%. Why someone risk, if market falls nbfc will sell your shares at lower price. Which gives heavy loss.

Like I’ve mentioned in my initial post, it is up to 24h working hours for now, but we will shrink the timeline as we move forward.

Broking & NBFC both under the same umbrella is a massive advantage. The fact that your MF units are in Demat is a huge advantage. For instance, some of the banks you mention don’t lend if the transfer agent is not CAMS. For us, it does not matter.

Also, some of your comparisons are not valid. LAS is a very different product, compared to the rest of the lending products out there. Yes, you can get an overdraft on your salary, you can borrow from Dhani, Cred or whatever. But when you quote these as an example, please compare it with a similar offering. LAS in very different, for example, when you borrow against LAS, you only service the interest, as I mentioned, your monthly obligation is 28 paisa for every 100 borrowed. There is no concept of an EMI here, hence monthly cash obligation is much lesser.

Noted, thanks for your opinion.

This is sucidal for investors. You need to get your stats on P2P right. Please check the amount of defaults and NPA in P2P, talk to folks who have done this consistently for over 3 years and understand from their experience.

Again, thanks for the opinion. But we all know what happens to players (and unfortunately their customers) who try and do such a circus.

Well, I dont know what to say for this rather nonchalant comment ![]()

5 Likes