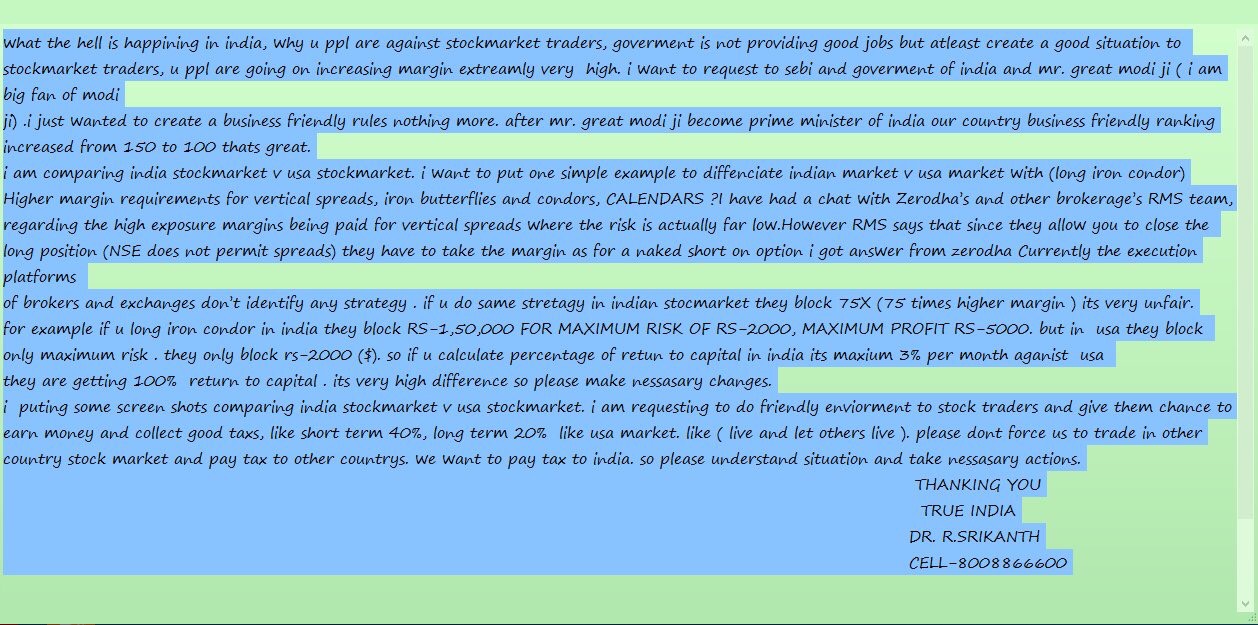

I cannot disagree more with each and every statement you made. It absolutely goes against the ethos of what equity markets are. Some of your statements are also mathematically incorrect, like pricing of options going up because margins went up. There is NO MATH equation that links option pricing to margin requirements.

I’m not sure how aware you are about how margins are calculated for risk defined strategies so I am going to share some of the stuff that is being discussed among option writers.

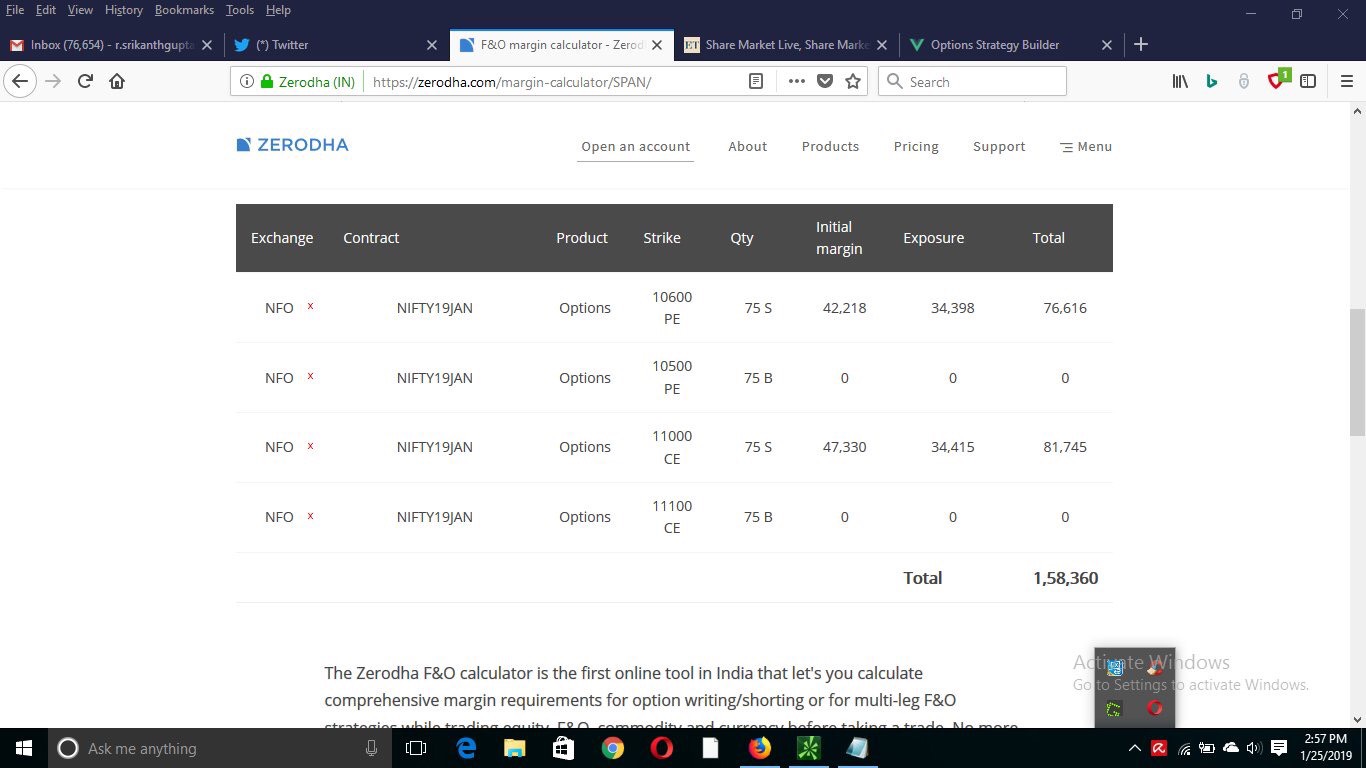

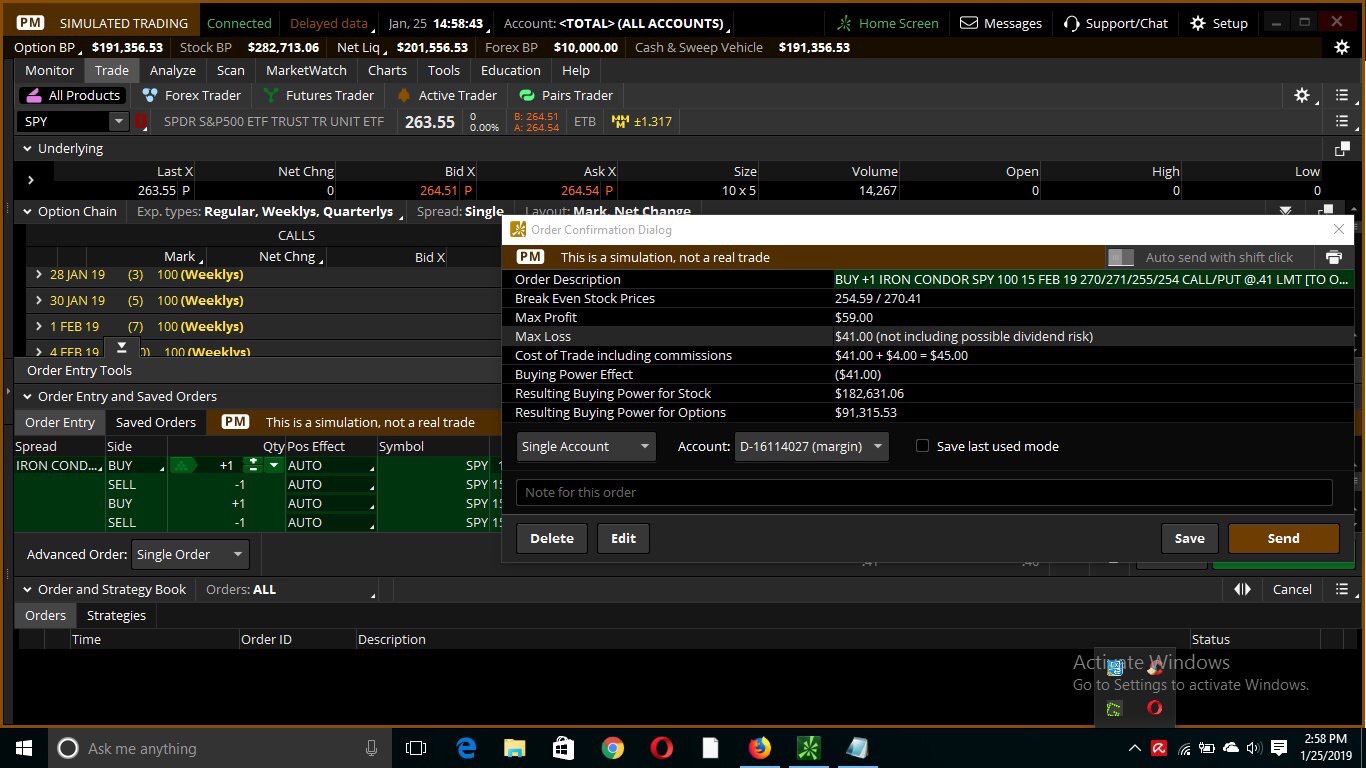

So basically if your defined risk is 2k, which is what it is for a covered call on BN then the max margin necessary should be 2k and some change - what is it right now ? 80k. Its fundamentally broken and none of what you have said has anything to do with the science and math of derivatives.