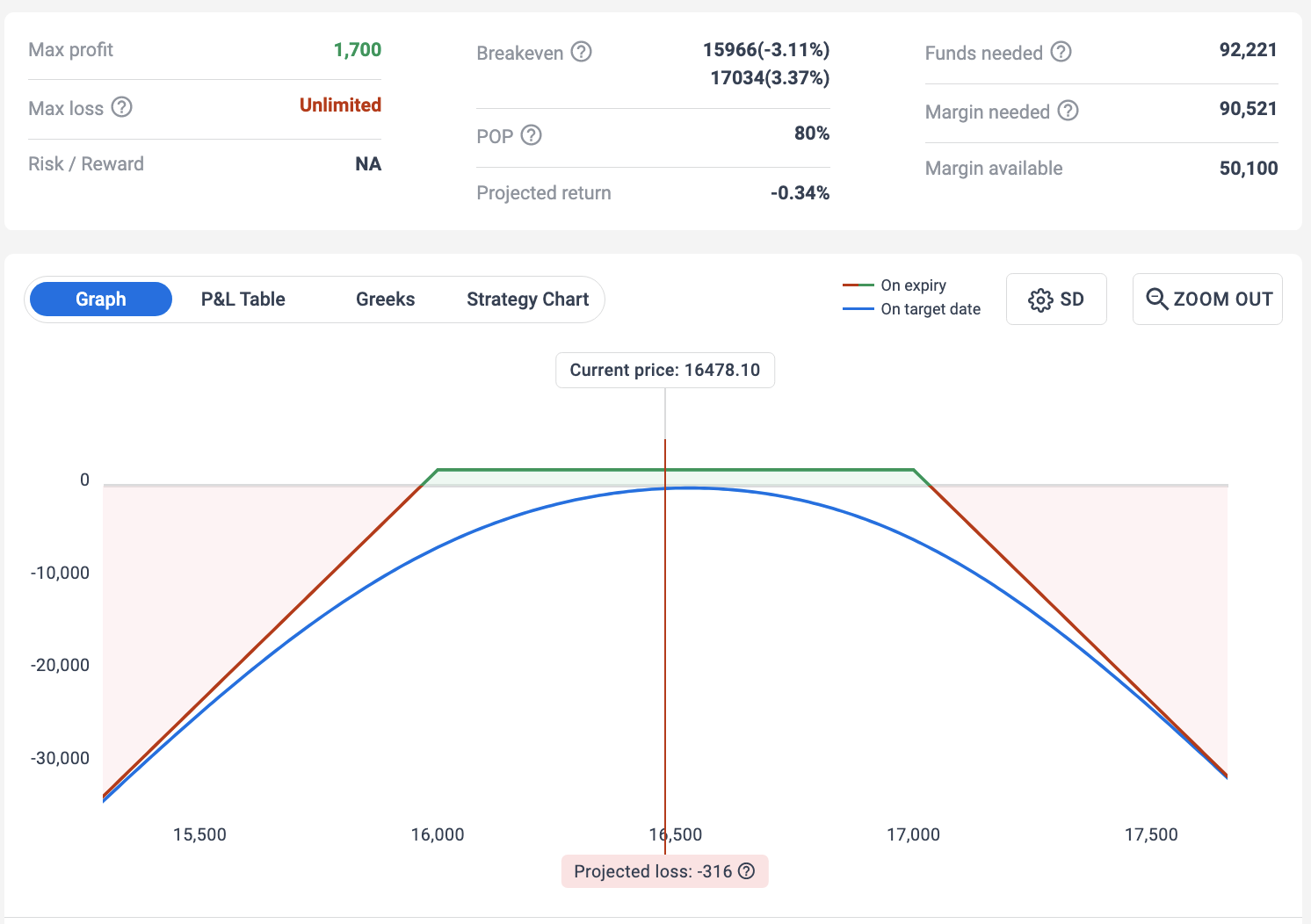

nifty spot price is 16500

Sell nifty 16jun2022 17000 ce - 14 Rs Premium

Sell nifty 16jun2022 16000 pe - 20 Rs Premium

nifty spot price increased to 16800

As per Varsity pay off excel sheet Call Option Writer is in profit of 34 Rs …

wont the premiums change of 17000 ce and 16000 pe if nifty spot moved to 16800?

how much premiums will be affected? who will be in losses buyer or seller? what could be approx premium values if nifty spot price moved 16800?

if spot price increasedto 16800 and 16500, the sold CE 1700 option price will go up resulting in a loss position. This should more less be offset by the decline in value of 16000 PE (a +ve position), provided both strikes were selected to be delta neutral.

Before I answer this let me clarify most important concept of options; option pricing.

The options prices depend on Black-Scholes Model.

In short option prices depends on

Underlying Price & Strike Price

Time to Expiration

Interest Rates

Volatility

Let me Elaborate Volatility

Option pricing models require the trader to enter future volatility during the life of the option. Naturally, option traders don’t really know what it will be and have to guess by working the pricing model “backwards”. After all, the trader already knows the price at which the option is trading and can examine other variables including interest rates, dividends, and time left with a bit of research. As a result, the only missing number will be future volatility, which can be estimated from other inputs

These inputs form the core of implied volatility, a key measure used by option traders. It is called implied volatility (IV) because it allows traders to determine what they think future volatility is likely to be.

The Bottom Line

Options are complex, but their price can be described by just a handful of variables, most of which are known in advance. Only the volatility of the underlying asset remains a matter of estimation.

Let me reiterate the last point

Volatility of the underlying asset remains a matter of estimation.

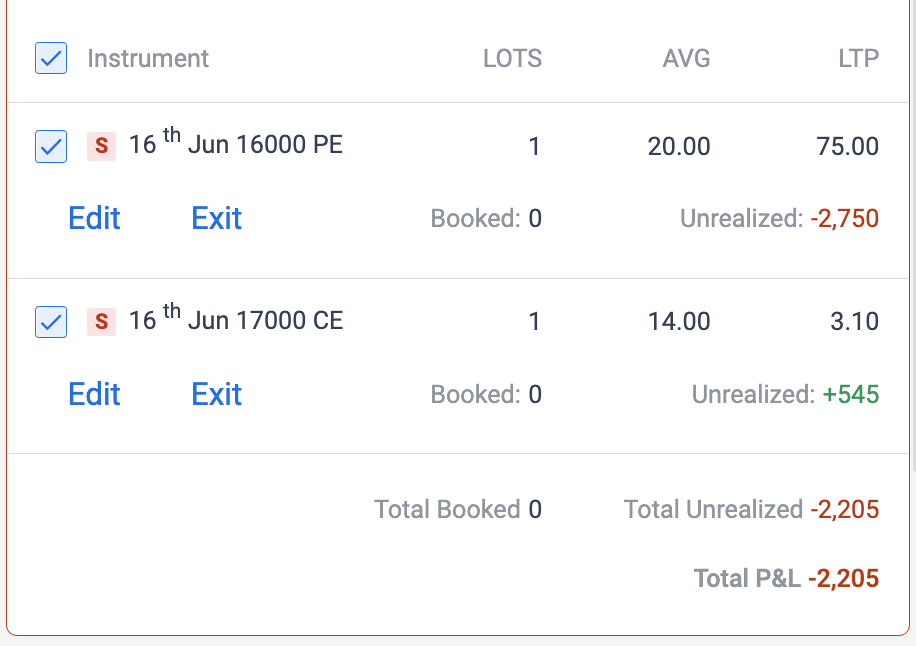

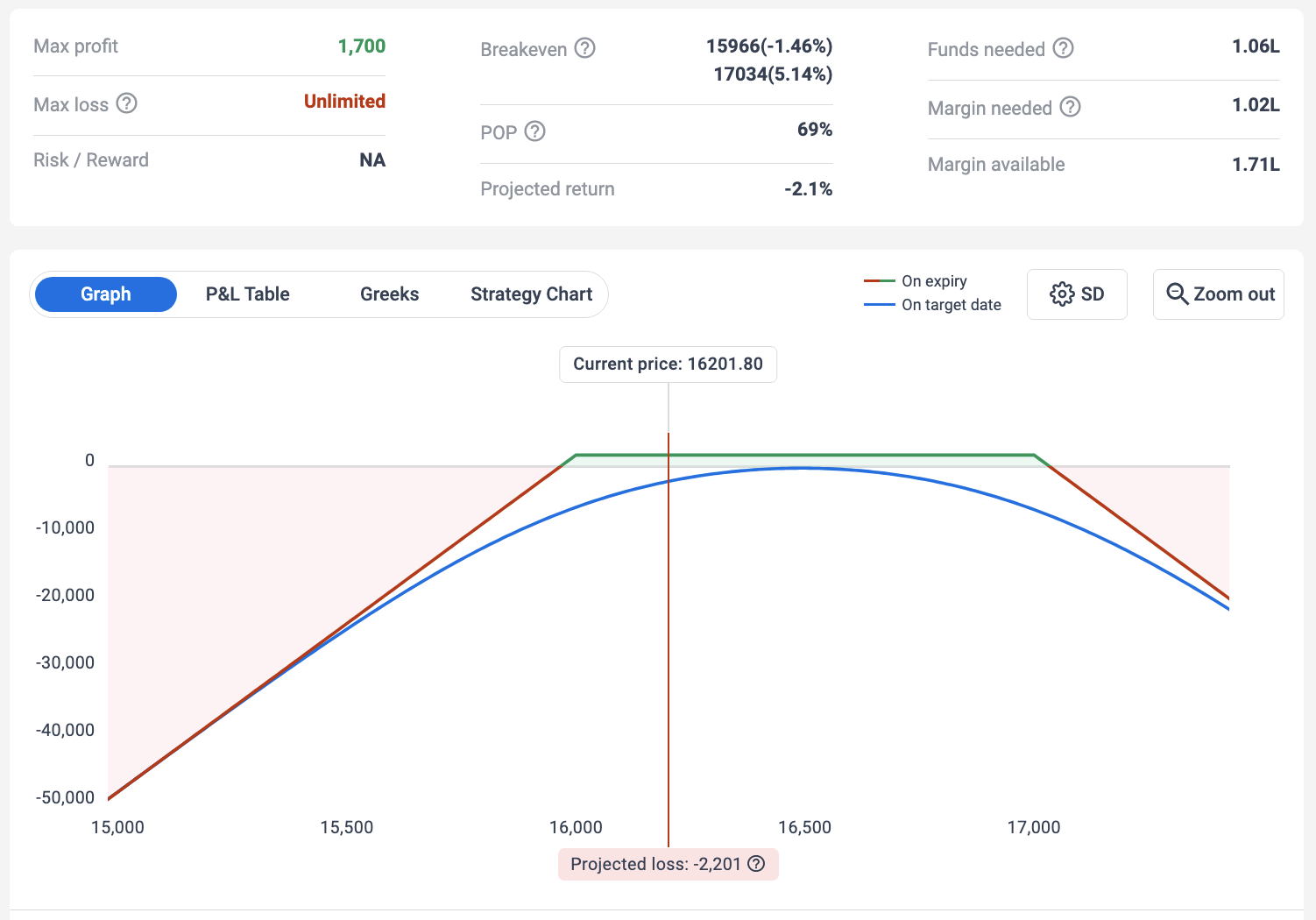

Here i have a few questions sir from your screenshot , 16201 spot

why premiums are shooting up fastly in the direction of market (20 to 75)and why not in opp direction ?

what happens if the buyer squared off position , assuming that seller want to hold these positions till expiry ? will the contract be transferred to new buyer or the position will be closed both for buyer and seller ?