I am totally cognizant of the fact that when the long options are squared off, the short options margin will increase.

But when you have not made a trade and then the margin shoots up, its something beyond your control. I did keep 5% extra for a spike in margin, but the surge here was 14L from 81L ie 17% (I am sure no trader will keep 17 to 20% buffer)

Nithin - do you have the rule book on how its calculated ? Without knowing the law, i wouldn’t know how i broke it.

Or can you try to talk with someone to get this added as a business expense, because last time @Quicko confirmed the penalties cannot be added as business expense.

Margin penalty is a fund collected by the clearinghouse for reserves to be used in the future or IPF or other purposes. This is compensatory in nature for the person who has paid can claim the same as an expense. This penalty is levied not against any law which is passed in parliment.

Margin penalty can be claimed as a business expense.

As per Explanation 1 of Section 37 of the Income Tax Act, any expense incurred by a taxpayer which is an offence or is prohibited by law cannot be claimed as a business expense. Eg: Interest paid on late filing of ITR cannot be claimed as a business expense.

Based on the nature of fine or penalty, if the penalty is for breach of a contract, it is deductible as an expense. However, if the penalty is for breach of provision of law, it is not deductible as an expense.

Margin Penalty is a penalty levied on trades performed without sufficient margin. Penalty paid to a stock exchange/broker is not an infringement of law. Thus, it does not violate Explanation 1 of Sec 37 and is deductible as a business expense.

@Nithin, you need to improve your own margin shortfall reporting system as well. I got charged an overnight margin shortfall penalty last week for apparently not keeping enough margin despite the fact that there was no sms/email sent for it, and more importantly, no shortfall when I myself checked it post market hours. Willing to bet my house on it as it’s something I do everyday by a force of habit.

There is a larger issue here which we are fighting for with the regulators on peak margin penalty issues and not really in control of the brokerage firm. Hopefully it will be fixed soon.

SPAN margin can change intraday based on volatility. This change gets updated on SPAN files made available before the market, at 11 AM, 12.30 PM, 2 PM, 3.30 PM, & at end of the day (EOD). If the volatility in the market goes up, SPAN margin goes up too and a customer who had sufficient margin when taking the position is now violating the peak margin requirement as rules stand today. SPAN margin can go up as much as 50% or more intraday, so even asking for 5 to 10% additional funds in the account isn’t sufficient. Every day there is some stock that moves over 5% leading to peak margin penalty on many client derivative positions in that stock.

The above issue gets worse when the margins go up as a result of the 3.30 pm SPAN file or the EOD SPAN file. Clients who had maintained sufficient margins till market close suddenly finds themselves short of margins post-market close. A penalty is then charged on the higher of two shortfalls - shortfall in EOD margin or shortfall in peak margin. Again as mentioned above, keeping additional buffer funds doesn’t guarantee that it would be sufficient to avoid penalty.

When the exchanges update the margins intraday, it takes a while for it to propagate to the broking risk management systems. Brokers have to download the file from the exchange FTP and upload it onto RMS. Today, this takes at least 25 mins on NEST (the most popular RMS system that powers at least 70% of the market). While the time to upload files will get reduced with time, this still technologically can’t happen instantly. In the time period that the files are being uploaded, the upfront margin being asked on the trading platform to take new positions could potentially be lesser than what is required as per the new SPAN file. The clearing corps assume that the time the file is published by them is when all broking systems are updated with the latest margin requirement, which is impossible.

Extreme Loss margins on derivatives is a percentage of the contract value. What it means is that when contract value increases, so does the exposure margins. So if a customer had taken a position with sufficient SPAN+ELM, an increase in the contract value increases the ELM margin and hence the customer will be short margin when the peak margin penalty is calculated. Again, collecting any buffer margin doesn’t guarantee that it will be sufficient to avoid penalties as the derivative contract can technically go up to unlimited in value.

The industry is requesting for one of the following solutions which will fix the issue that you are highlighting.

The above is an issue only with derivatives and not with equity trading, even when there is a minimum VAR+ELM for equity. like SPAN+ELM for derivatives. This is because in equity a broker can collect a fixed 20% for all stocks and that ensures compliance to peak and end of the day margin requirement. This fixed 20% doesn’t change intraday and hence doesn’t lead to any of the issues mentioned above. So a simple fix to this issue is to follow a similar policy for derivatives. But the tricky bit with derivatives is that there is trading in index derivatives which require a much lesser margin than stock derivatives. So a single fixed percentage for stocks and index derivatives wouldn’t work, it will have to be two fixed values.

Today the CC looks at the 4 intraday snapshots or EOD positions, checks whichever needed the highest margin among them and a penalty is charged if sufficient margin isn’t present based on the SPAN+Exposure margin requirement at the time of taking the snapshot. For the purpose of calculating penalty, if we instead calculated margin for the peak position selected using the lowest SPAN+Exposure for the day (to cover for the intraday increase in margin), we can avoid the penalty issue. This will need CC to run the peak position selected from all customers through a process to calculate the margin for the same position using the lowest SPAN+Exposure for the day. This will require work from CC and will be the most efficient solution.

In the above solution, if selecting the lowest SPAN+Exposure for the day is a technological challenge, we could just use the beginning of the day SPAN+Exposure. The only issue would be that customers wouldn’t get the benefit of margins going lower during the day, which is an issue. But this is a fair compromise considering all the issues that the industry faces today.

Nithin,

Understand you are in talks with the exchange to get the issue sorted out - the fix may take say 1 to 2 months

What i am asking is the formula on how the exchange calculates the peak margin. Even a complicated derivative instrument like options has a formula calculator using which we can find the fair value

What formula does NSE use in this case - if i know it - i can be prepared mathematically.

Or else on what time frames does the exchange take the snapshot (this method is like slowing down your car when the speed cam is near) so that we can trim our positions in those window

I feel my issue is a bit different here. Penalty has been charged for keeping negative margin overnight (‘margin status’ being negative on margin statement) but it wasn’t being displayed as such on Kite.

Suppose I keep 6L as margin at EOD & the post-market updation decreases it to negative 5 L. That’s fine, no issue with it. But then, the ‘Available Margin’ section should also go to negative na? This wasn’t the case here. Plus, if margin is negative, the broker gives out a margin call also. This also didn’t happen.

The issue is the same. If the margins go up post 3.30 pm (in last EOD SPAN file), it wouldn’t show up on Kite. Margin call can’t be given out since this is post end of day. The best way to cover for this is to ensure that you have atleast 10% buffer margins. Higher buffer margins if you are trading volatile contracts. This should hopefully get fixed in the next couple of months.

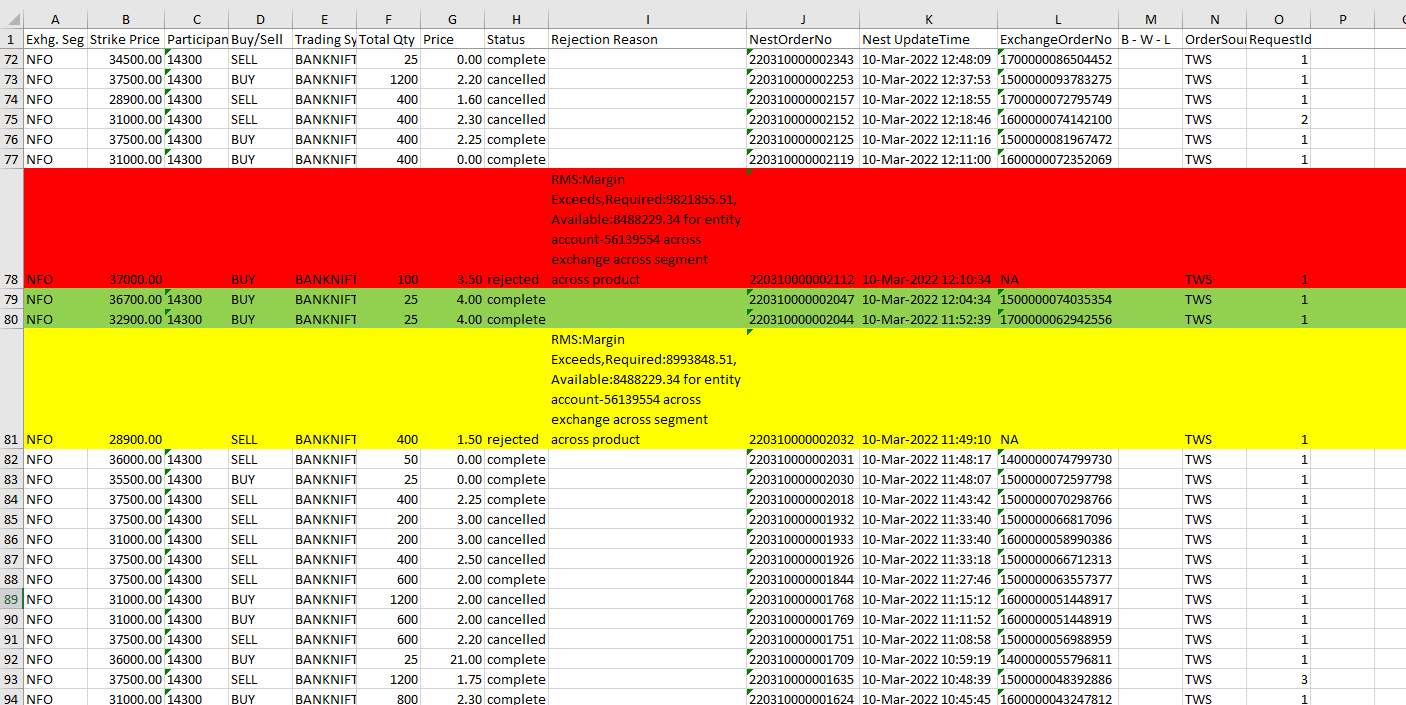

The yellow highlighted row shows i am unable to take a short position due to lack of funds at 10-Mar-2022 11.49.10 - the available margin is 8488229.34

The green rows shows the buy orders (long position) i have taken at 10-Mar-2022 12.04.34 & 10-Mar-2022 11.52.39 - which should increase the margin

The red row shows i am unable to make a buy order (long position) as suddenly the margin shot up to 9821855.51 at 10-Mar-2022 12.10.34

If you refer the trades i have done, there is no reason why an additional margin of 14 lakhs was blocked in 20mts period i am referring to

Surprised you said this because this just isn’t true. Margin available which is there on Kite at 3:30 pm is different from the margin which is there at say 4:30 pm. Like today, after the post-market updation, it increased by 45k, variation being a bit less since today the last hour or so was a non-volatile one.

Nithin

NSE provides mg13_p 1,mg13_p 2,mg13_p 3,mg13_p 4 files which contains our periodic peak margin value mostly by 4 pm.

Why doesn’t Zerodha share those values before EOD so that we can transfer funds and save ourselves from the peak margin penalty.

Forget EOD we are not provided with the peak margin data next day or in the coming week. We just understand that there was a peak margin shortfall when there is penalty entry in our ledger.

Do you think it is fair?

Can you also inform me whether it is OK with NSE if you report our entire pledge holding theoretical value (value before haricut).

If it is accepted by NSE, Zerodha can save us from the penalties and Zerodha can charge DPC on the difference between theoretical value (gross) and net value after haricut.

It would be a win-win situation for both of us.

Appreciate if you can clear this.

There is one SPAN file imported at around 3.30pm, which might update by 4 to 4.15 pm. What I meant was that post that last file update if there is any change in EOD SPAN file, that can’t really be shown today. But we are working on showing that as well.

According to peak margin penalty rules, you can’t transfer funds post a trade to avoid it. You need to have had the funds before the snapshot was taken by clearing corporation.

About peak margin penalty, we share whatever we can. There isn’t really much we get to know as well.

No, the haircut has to be compulsorily applied when a stock is pledged. Very soon it will be mandatory that when taking any position using pledged margin, the customer fund 50% in cash. Today we can fund it with a cost, but this will soon be disallowed.

But NSE margin reporting is done EOD value, and I have done many times in zerodha itself. When ever i expect I have exceeded the peak margin, I simply transfer an estimated amount and never get caught.

I am aware that haircut is done by NSE itself. Zerodha can report gross amount as client funds and avoid the penalties. That’s what I meant.

We have time till may for that, in the mean time we may avoid the penalty if you can consider.

U have been lucky that the peak snapshot wasn’t maybe taken at that time.

Ah no, that would be misreporting. Major penalties on the broker for doing that. In any case today all securities are pledged directly to CC, so they know what is the collateral margin after haircut.