IT day today. Index trend decider. One thing to note though is …Nifty IT has had a massive run up in anticipation of good results. I expect levels of 40000 in the best case scenario. Any minor disappointment can lead to a swift correction. Considering Risk reward , I will be very careful trying to long IT stocks now.

Infact I’m cautious on market itself at these levels.

Comments : Overall great result and results can be considered as inline with the expectations. Given the valuations, the reaction needs to be seen (neutral to slight negative very likely scenario given the response to other IT stocks)

Tata Metaliks

Net Profit at Rs 35.65 Cr (Down 53 % YoY), Down 35 % (QoQ)

Revenue at Rs 689 cr (Up 31 % YoY), Up 7 % (QoQ)

Margins at 9.83 % V 24.12 % (YoY), 15.5 % (QoQ)

Comments : Overall results seem sluggish as Raw material price rise impact was seen in the margin compression. Stock was up 6% from last 5 days. Need to hear from management on the quarter ahead.

Summary : The stock has been a laggard of late and with the above results which are decent may show minor upside in the short run ( Overall view is neutral to positive as market might await ICICI bank’s result before deciding a sustainable move )

HCL Tech

Summary : Looks like a mixed set of results with revenue and constant currency growth above estimates and margins below estimates. Stock price may follow in line with IT sector.

One observation that I can make from results of heavyweights like TCD,Infy,wipro,hcl tech and HDFC bank is that market is not reacting heavily on the results (both on the up and downside). It as if as market has factored in the results in most of the companies and therefore, is looking for fresh triggers for a drastic move.

Till then, it seems we will have ping pong in markets.

Summary : Company’s operating performance was poor and the bottomline was aided by tax credit. Volume degrowth and margin contraction was also seen in the last quarter. Mgmt commentary was optimistic. Optically the result may look good but overall it was poor. Stock price movement can be rangebound btwn 7000-8200

Angel Broking

Cons Net Profit Up 125 % at Rs 164 cr Yoy , Up 23 % qoq

Revenue Up 95 % at Rs 597 cr yoy ,Up 13 % qoq

Ebitda Up 121 % at Rs 234 cr yoy,Up 23 % qoq

Margins at 39 % V 34.5 % yoy , 36.22 % qoq

Summary : Great set of numbers. With LIC, NSE IPO coming up im personally expecting the stock to be mostly in positive territory.

Standard disclaimer (all posts) : No personal investment in any picks mentioned.

Assets Under Management grew up by 26% yoy to 1.81 Trillion

Asset quality improves as well.

Summary : Basically a bumper result on all fronts. Should definitely be a booster to the whole financial sector as well. If at all there is a results based volatility, this stocks definitely presents a buy on dip opportunity.

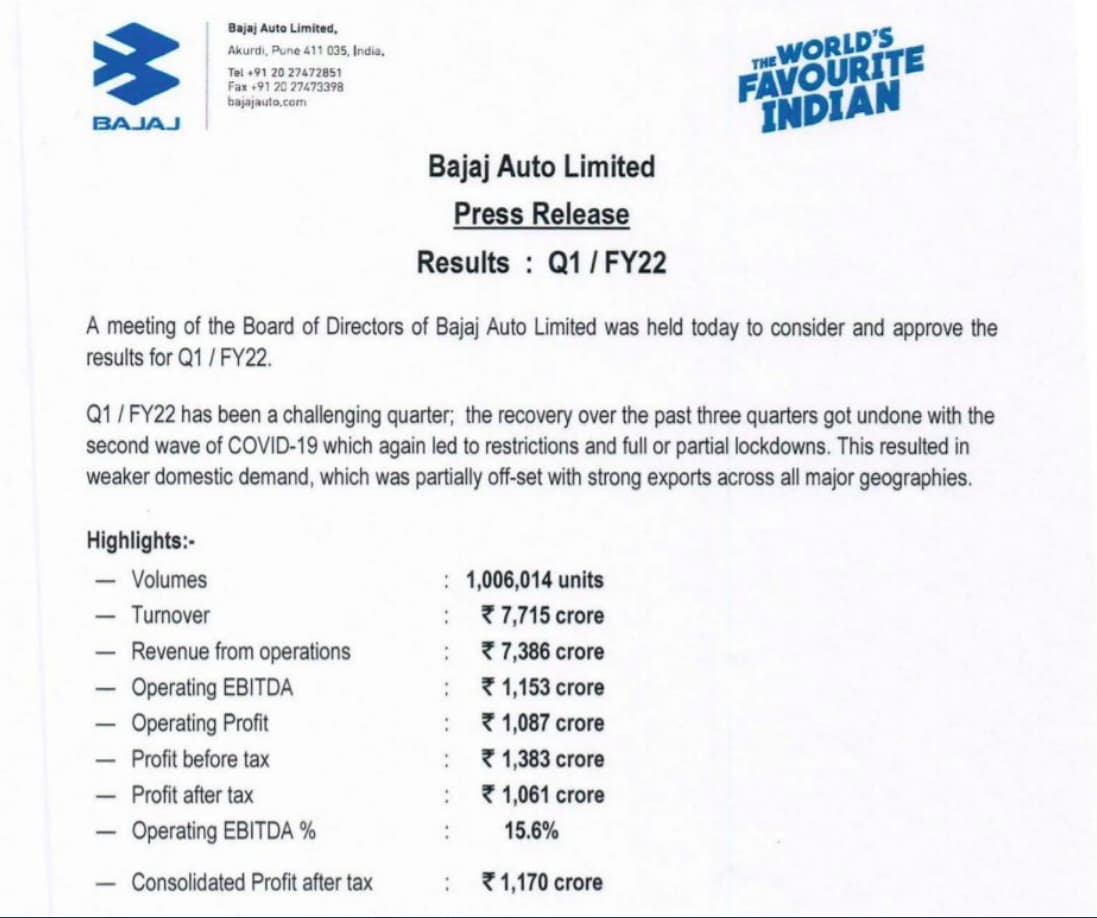

Summary : Although it was a challenging quarter for the company, it has exceeded the analyst expectations a bit. As auto sector is looking technically strong. It may follow the trend of the sector.

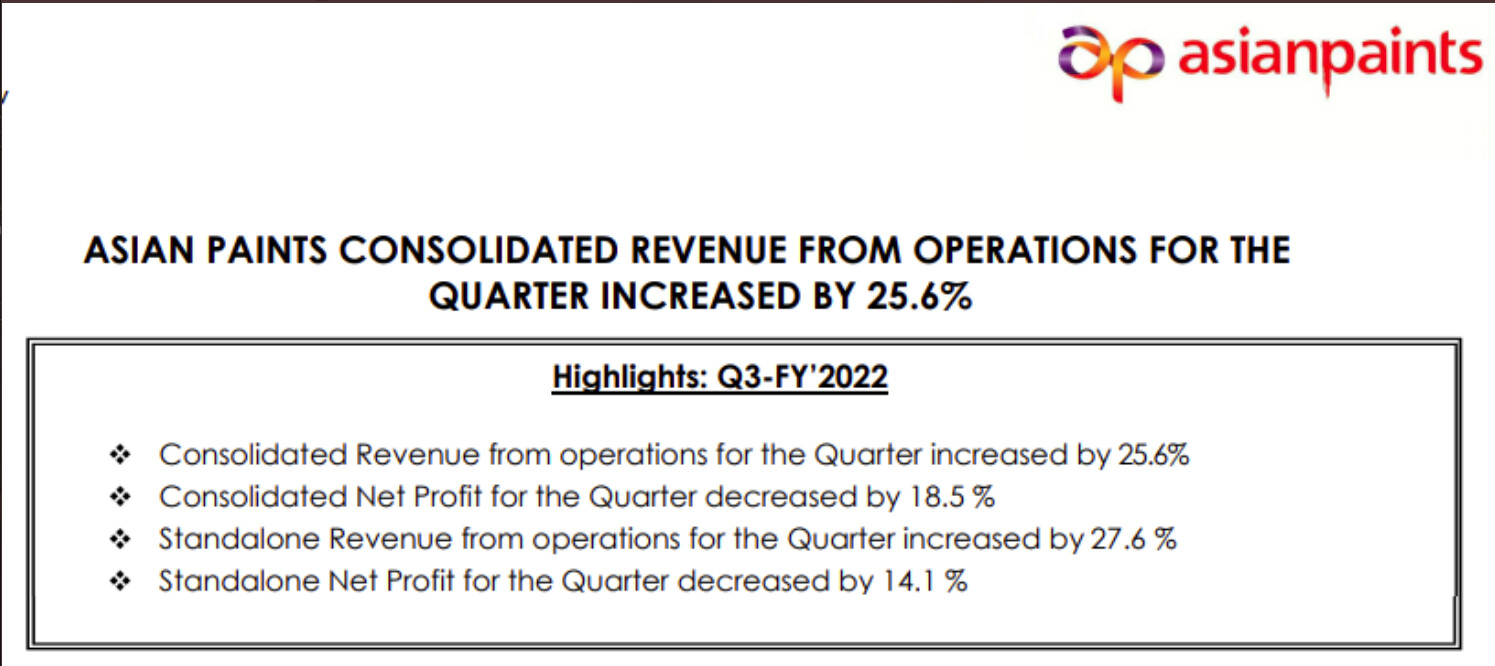

Summary : Raw material cost rise is going to most likely impact the demand going forward keeping the growth figures in check. Limited upside considering the fact that FMCG pack is usually High PE.

Summary : Margins have contracted and the demand outlook for the Jan was also weak as raw material price hike is more than 20% as per company’s concall. again limited upside potential.

Bajaj FInserve

Summary : Overall below estimate numbers due to the impact of slow auto sales, insurance business getting affected due to unseasonal rains.

The analyst expectations and the reaction aside, how crazy it is to see that reliance is growing almost like a small/mid cap when it comes to growth in the topline or bottom line for that matter.

Energy sector is doing good and the same should continue going forward in my opinion.

with renewables and green energy verticals getting added, Reliance as an investment is ready to fire on all cylinders.

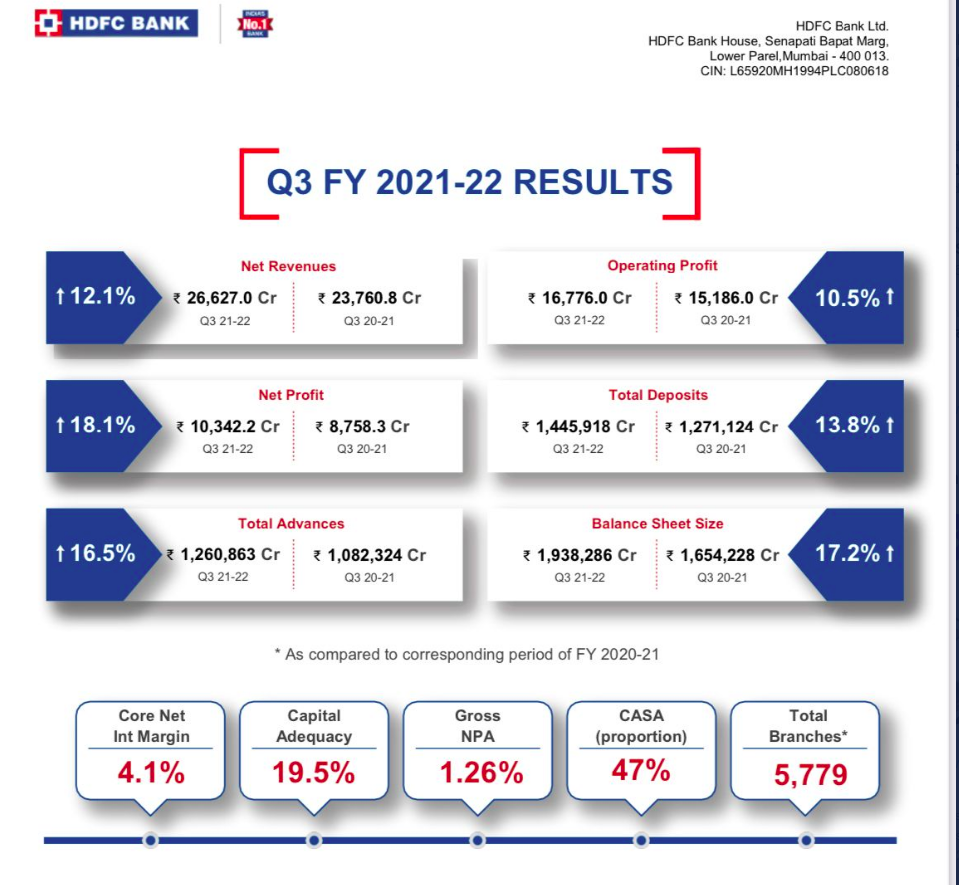

ICICI Bank

Superb set of numbers for the bank with NII growing 23% PAT growing 25% YoY to 6,194Cr ,CASA ratio at 45% , NIM was at 3.96% ,ROA came in at 1.90%

It has for sure become one of the leaders if not the leader in the banking space. Outperforming HDFC Bank

With market being in a precarious situation, I’m expecting the bounce to come with support of likes like Icici.

Summary : Although the YoY result looks good with rise in revenues and profits, QoQ, the margins have deteriorated sharply due to the massive rise in crude thereby leading to margin contraction. OMCs were amongst the top losers today.