For intraday trading major difference between backtesting and live trade seems to come from slippage (difference between last traded price and the price at which order gets filled at) at entry and exit. Is there any realistic estimate for stocks in nifty50 ? Or process by which one can calculate stock wise estimate using historical data.

I use fix percentage (e.g. 0.03 % for entry and exit for all stocks ) which is far from reality.

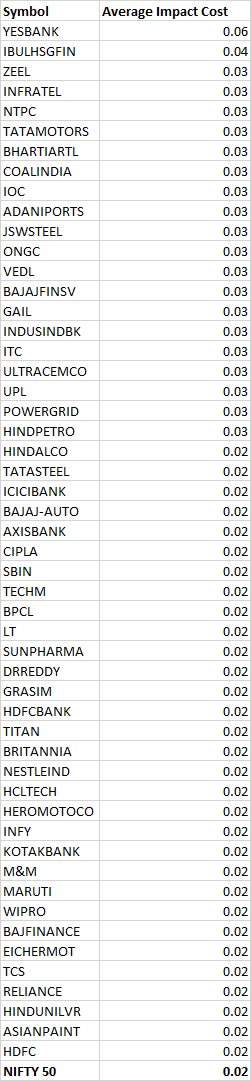

Impact cost gives you answer for this, check this for more. Also exchange gives impact cost for nifty stocks here, check under monthly reports.

@siva Can you please help to simplify this report in an understandable user-friendly and easy to read format?

The impact cost on the NSE website is a good place, to begin with. The exchange captures bid and asks at 5 different points during the day for Nifty 50 and Next 50 stocks for an order value of Rs 50L and publishes the monthly averages in this report.

Slippage could also differ if you trade futures over equity since futures are traded in standardized lot sizes.