And as default exchange means , default exchange for “holding price/value”

Lets say I select NSE then only NSE live price shows in my holdings

And

While clicking on “exit” button in holding , it first auto select NSE exchange to execute my order.

(As per norm it show BSE but price as per NSE and exit order execution on NSE if selected as default by user)

As per this (current mechanism in Zerodha), it shows only BSE price which is laggard because of low volume on BSE and

Another issue is when selecting “exit” in hurry , it auto select BSE and mostly miss to change exchange to NSE , which gives high slippages and loss.

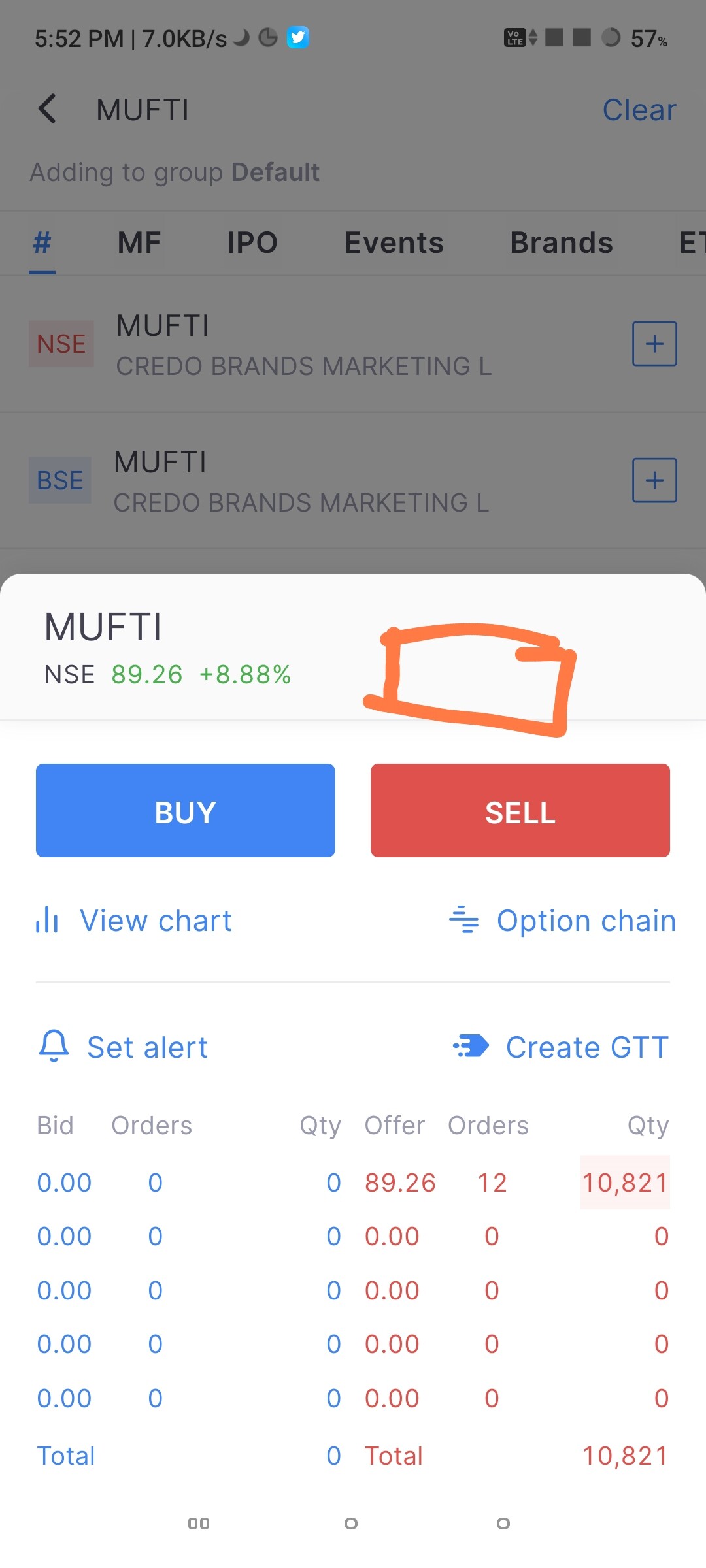

notice how bse first shown when exiting from holding instead of NSE where liquidity lives

don’t show best price or higher price that’s illiquidity , show price where liquidity available

what’s point of showing price of holding at BSE ~ 19.74 ( and next available would be ~19.67- 90 % of times ) when NSE ~ 19.73 or ~ .72 has huge liquidity available

Day 73: Why ‘Smart Order Routing’ (SOR) Doesn’t Fix the Holdings Bottleneck

@siva SOR handles where the order goes after it’s swiped, but it completely misses the actual issue: UI Latency and Liquidity Depth.

Display Mismatch: SOR doesn’t change the fact that the Holdings dashboard shows a stale BSE LTP. If the UI displays misleading data, my real-time evaluation of a fast-moving market is completely blinded before I even trigger an exit.

The “Best Price” Trap for Large Sizes: For a high-beta stock like JP Power, BSE might show a “best price” for a tiny 500-share retail lot. But when trying to offload 1–2 Lakh shares, BSE lacks the depth to absorb that volume. If an SOR system attempts to route a major block to BSE based on a superficial top-of-book price, the order will bleed through thin layers, causing massive impact costs.

Current Capital vs. Future Features: “Plans to bring SOR” is a long-term roadmap answer. Active traders are facing a ₹20,000–₹40,000 Opportunity Cost today.

We don’t need a complex routing overhaul to solve a basic visibility flaw. Give us an immediate primary exchange UI toggle so we can target deep NSE liquidity instantly. Exit precision cannot wait for future features.

@siva Why overcomplicate a simple execution reality? Just default to NSE. What is the point of showing a higher previous-day close price on the UI if the actual intraday liquidity isn’t there to absorb high-volume orders?

For anyone trying to exit large quantities with size, a higher price on BSE is nothing but a phantom price. It creates a temporary illusion of a better value on the dashboard, but the moment you try to hit the bid, the complete lack of depth results in immediate, heavy slippage.

Forcing an over-engineered backend rule onto a straightforward UX problem just makes things unnecessarily hard for anyone trading with volume. Real Volume > Phantom Prices. Stop over-complicating it and just give us an NSE default toggle.