Arbitrage funds offer almost 4% post-tax for a holding period of more than 1-year. Also, Arbitrage funds have slight fluctuation so the difference in returns would be negligible.

If liquidity is not an issue, are T-Bills safer?

I used to think Arbitrage Funds are safe until I read Arbitrage Funds – Varsity by Zerodha and came across Principal Arbitrage Fund and its DHFL bonds investment issue.

Fixed deposit is not an option as post-tax it goes down too much. Besides, I believe only deposits up to 5L are insured only. So I think T-Bills are better than FD if safety is a bigger requirement.

I generally do not see any specific value in individuals investing in T-bills. Selection of debt instrument is always a trade off between Safety and returns

For debt instruments, STCG is not 15% (that is only for equity). For debt it is at your slab rate, So taxation on T-Bill would be same as your FD.

Right now SBI is offering 5% on 1 year FD, and I would rate SBI FD almost as safe as T-bill. So FD would be better choice if you are looking for fix return and safety

If you are looking at returns and compromise a bit on safety, arbitrage funds are better choice, returns are slightly higher (historically) and they are tax efficient. One off cases of fund loosing money will always be there, but if you look at fund with sizeable AUM and good portfolio, such issues can always be avoided (or its impact would be minimal).

So in either case, investing T-bill does not really make sense as per me.

Sorry. I somehow missed that. With this info from a returns perspective, it won’t make sense to go for T-Bill now.

I was planning T-bill for a portion of the company surplus. Currently, I am keeping them split in multiple arbitrage funds with good AUM. I will continue with arbitrage for now.

I think only if for some reason T-bill yields go higher than FD/Arbitrage, it will make sense.

Ohkk, frankly I am not aware if corporate have some other advantage of investing in T-bill. I was just thinking from individuals point of view.

This is going to be very rare.

T-bill is most secured short term debt instrument (as it has sovereign guarantee). So basically that is the risk free return and rate on it will always be less than other higher risk products.

But again as I said, I am not aware about other advantages which corporates might have. So don’t go by my word

I think if you want to invest in T-Bills then liquid funds or overnight funds investing their money in the same instrument would be your best bet. Arbitrage can still provide negative returns in a quarter. See their volatility back in March of 2020.

Completely agree on it. Its unlikely to happen that something that is risk free will have better returns!

But again as I said, I am not aware about other advantages which corporates might have. So don’t go by my word

Corporates have less tax rate but between FD and T-bills its same. So no relative difference. Arbitrage still wins hands down in terms of better returns except for one-off March 2020 period as mentioned by @SMIFS_LIMITED

Won’t buying T-Bills directly be more efficient as mutual funds even direct ones will have expense ratios? Please assume for time being, the objective is to park some funds in T-Bills only and there is no requirement to redeem in between.

Arbitrage can still provide negative returns in a quarter. See their volatility back in March of 2020.

I am no expert but I feel in March 2020, there was too much selling and too less buying. For arbitrage opportunities to be present, buy & sell should be balanced.

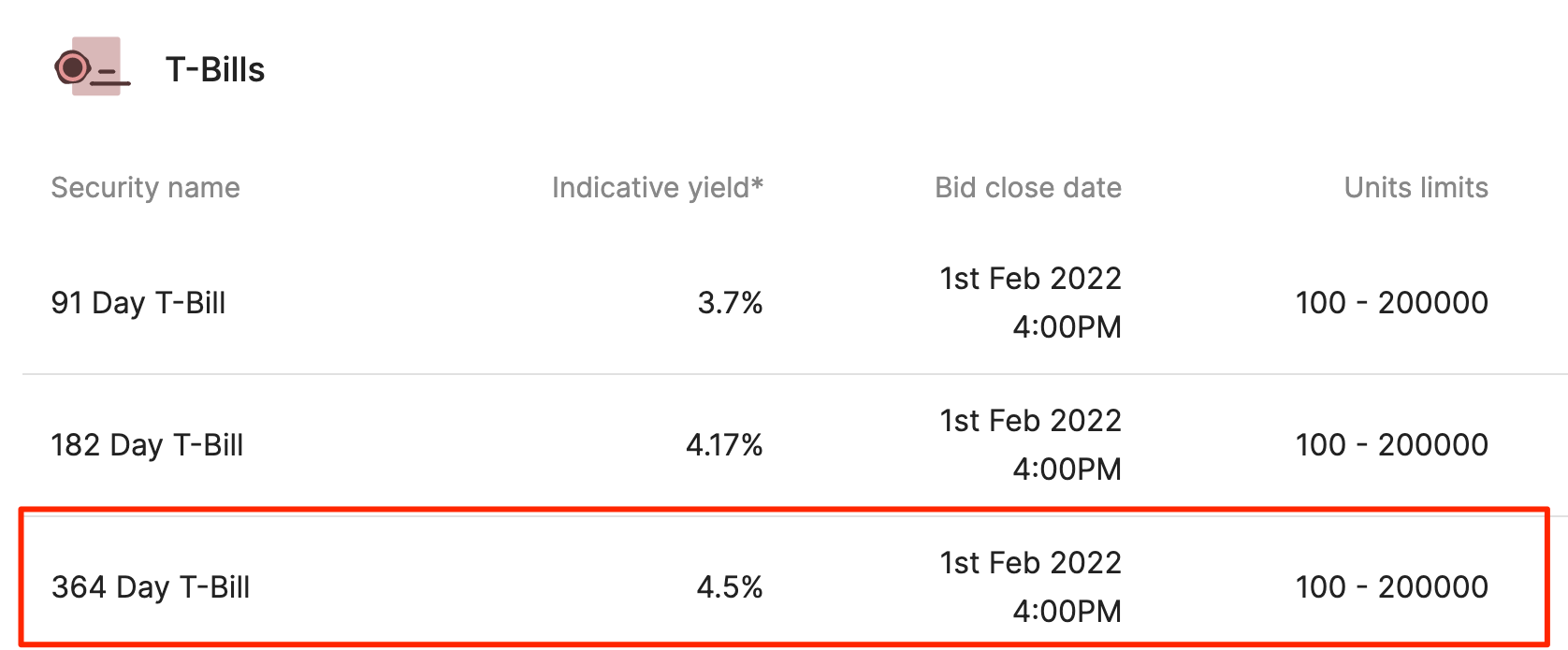

If I invest Rs 10,000 in 91 Day T-Bill and 10,000 on 182 Day T-Bill, it will generate some interest but this interest will be less than Rs. 1,00,000, for STCG to put 15% Tax.

Pls correct me if I am wrong, As per my understanding, If (Investing + Trading) profit are below Rs.1,00,000 for current FY , then Retail investors don’t have to pay any STCG or LTCG Tax during Tax filing.

The exemption amount of 1 lack is for LTCG only.

The limit applies for Capital Gain transaction and not applicable for interest as this will be taxed as per your income.

This is my understanding and I am sure experts will advise.

T-Bills are issued at a discount & redeemed at par. Hence, the appreciation is considered a capital gain.

As per your example, a 91-day T-Bill is considered a short-term holding, hence STCG is applicable and is taxed as per the applicable slab rate.

Only LTCG us/ 112A is exempt up to Rs. 1,00,000. Section 112A covers LTCG on the sale of equity shares, equity mutual funds & units of business trust. So, the exemption of Rs. 1,00,000 is not available on T-Bills.

I think it’s due to its shorter maturity. All securities need to be approved by the clearing corporation and maybe it’s too much of a hassle to keep approving and retiring the securities as they are issued and matured.

The Exchanges approved list is updated once a month & clearing corporations ask trading members to unpledge the securities one month before the maturity to avoid any issues wrt to settlement. So it is difficult to support T-bills. However, you can pledge long-dated G-SEC bonds.