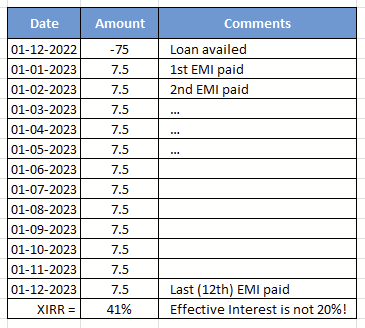

Well, i read it as follows…

- A 75K loan.

- 20% annual interest on it = 15K.

- Total repayment (principal + interest) in a year = 90K.

- 12 monthly EMI installments of 7.5K each = 90K.

Yes, IRR maybe different / much higher,

but this is how EMI-loans are pitched to end-users

to make the interest-rate seem lower than what it actually is, right?

Also add innocent sounding “processing fees” on top

and one is minting money providing such loans to unsuspecting folks.