Those are two separate points.

1 Like

I’ve heard about that too, a total scam as how can interest be demanded on the money you’re not actually getting? The interest shall be levied on the after-interest-cut amount.

Yes. Two sides of the coins

You just don’t understand how interest works. Do you?

Let me try once by one extreme example.

Let’s say you get a loan of 1cr at 1 percent interest per annum. But terms of repayment is that you have to repay 99,99,999 on the very next day and remaining 1 rupee you have to pay after one year.

At the end of the year you have to pay 1 rupee back along with 1 percent of one crore as interest. That is 1,00,001. Does it make sense to you?

1 Like

Thanks for making me understand

By your extreme example, this guy pays 74999 the very next day and 15k+1 at end of year ?

While writing the post ,I was uncertain about some aspects.Now ,I gotten some clarity.

Let,me reiterate the situation I am having in simple terms

Total Loan amount = 75 k

Total interest Rate = 20% per annum

Total amount to be paid in year = 90 k (75 k loan amount+ 15 k total Interest amount)

I think ,I have to earn 10 % per month of loan amount (75k)

Which is 7.5 k

I don’t want to know in-depth knowledge about EMI.

I simply wish to know ,it is possible to earn mostly from equity segment of 10% gain from the capital (75 k).

And thanks for your valuable feedback

Thanks for the clarification.

Glad to know that you aren’t paying 7.5K each month as EMI.

However, one fatal flaw in this scheme of yours

is that income from trading/markets is NOT guaranteed regular income.

There will be days (or weeks, or even months)

when there are no opportunities in the market for the strategies that one is aware of.

In such cases,

individuals expecting regular income often end-up taking riskier/nonsense trades

and losing most / all of their capital.

Hopefully, you can learn this from observing others

and avoid losing your savings/loans in the market to learn this.

Think of it this way.

If there was an opportunity to earn 10% per month (i.e. >100% in a year)

why would anyone loan you any money at 20% per annum ever!

They would simply double there money in the market themselves!

A major reason someone is willing to lend you money at 20% per annum interest,

is because they believe 20% per annum returns are less riskier than “investing/trading in the market”.

Also, whoever was planning to lend you the loan

if they were to know about this hare-brained scheme of trying to earn 10% per month, each month,

i believe they would NOT lend you the amount,

as it it almost surely going to be lost in the market in 1-12 months.

(unless you have some other asset to back the loan,

which they will happily claim when you inevitably default on the loan after losing 75K in the market)

2 Likes

![]() this

this ![]()

The subsequent discussion about whether the loan is actually 20% or 41% (depending on how it is structured) doesn’t really affect the answer to the original question…

Succeed?

IMHO, unlikely for the performance described in the original post of this topic thread.

Not sure what is it you want to highlight with this line of reasoning.

Sure, 3% per month (>36% per annum) is greater than 20% per annum.

But, there is no guarantee of a 3% income for the entire duration of the year.

AFAIK, OP doesn’t have some “sure thing” arbitrage trade

that is going to net them 3% per month, every month, for the next 12 months.

Is that even a realistic feasible expectation?

@VarunG From your earlier comment, i believe you agree that its is NOT a realistic expectation.

Definitely not for OP,

who has also shown to have insufficient risk-management in their trading record so far.

2 Likes

It was about the 15k interest he had to pay for 12 months. So he is effectively giving out 1.25% of interest

Ans you know what , I now know where the discussion went south.

There was another thread about borrowing 10 lakh from another individual. I was reading and commenting on these two threads simultaneously.In this thread , OP never said borrowing from ‘where’ !!

I confused and assumed it’s from an individual. Whereas OP only stated a ’ personal loan’ . Banks and NBFC’s loans work on how you guys pointed out. I was stuck with the flat rate that individual money lenders operate.

Anyways OP must have got more than what he had asked for .

Cheers bros

1 Like

WOW such a fantastic idea OP.

Why didn’t i think of this sooner.

Damn, you are really giving away money making secrets OP.

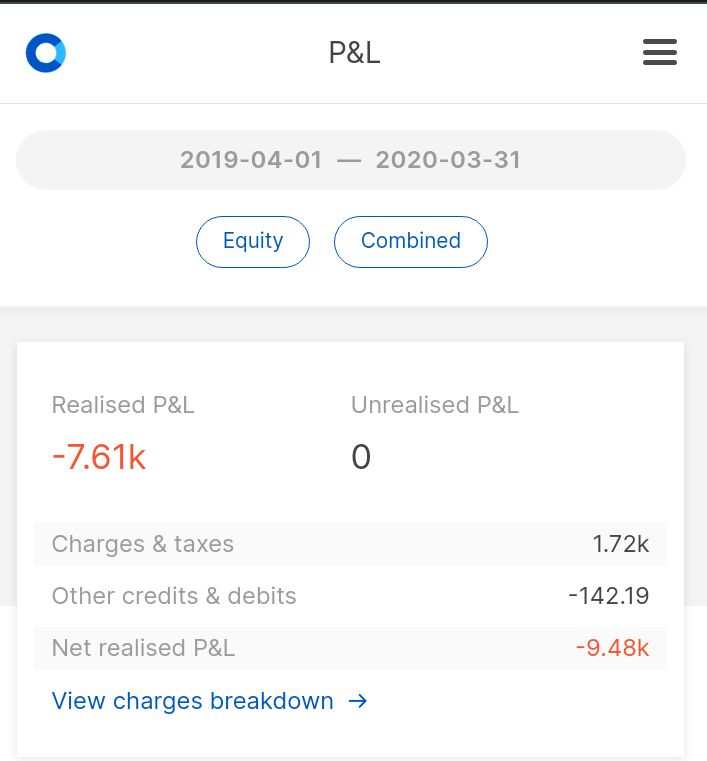

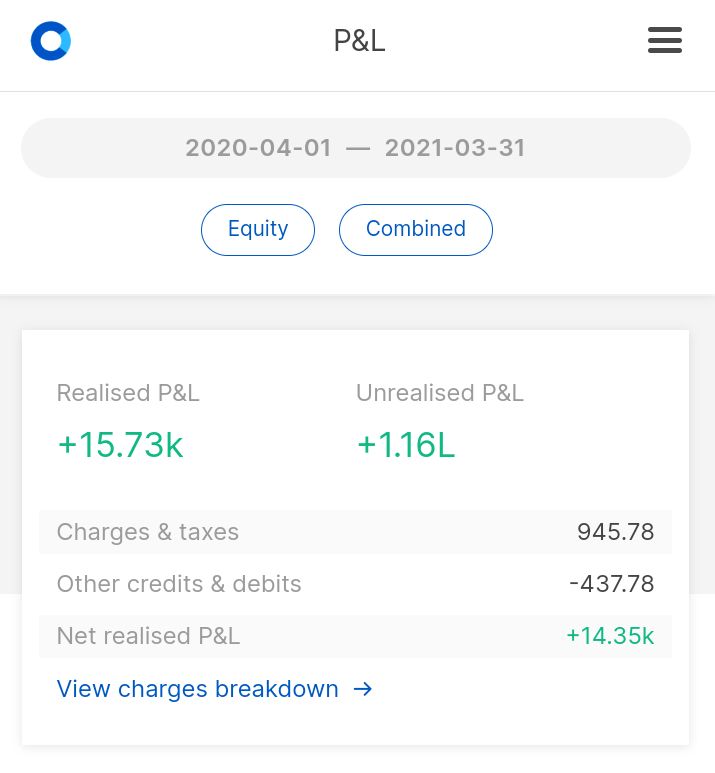

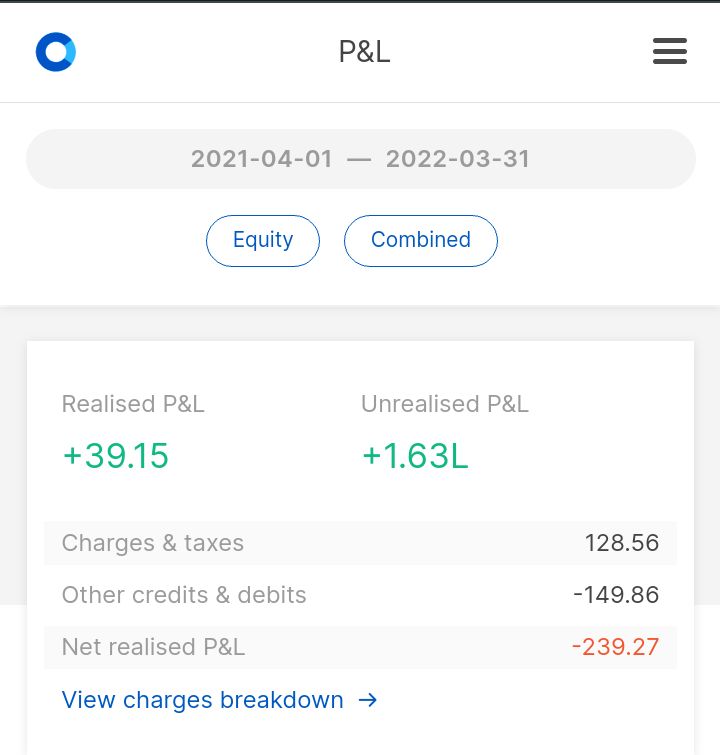

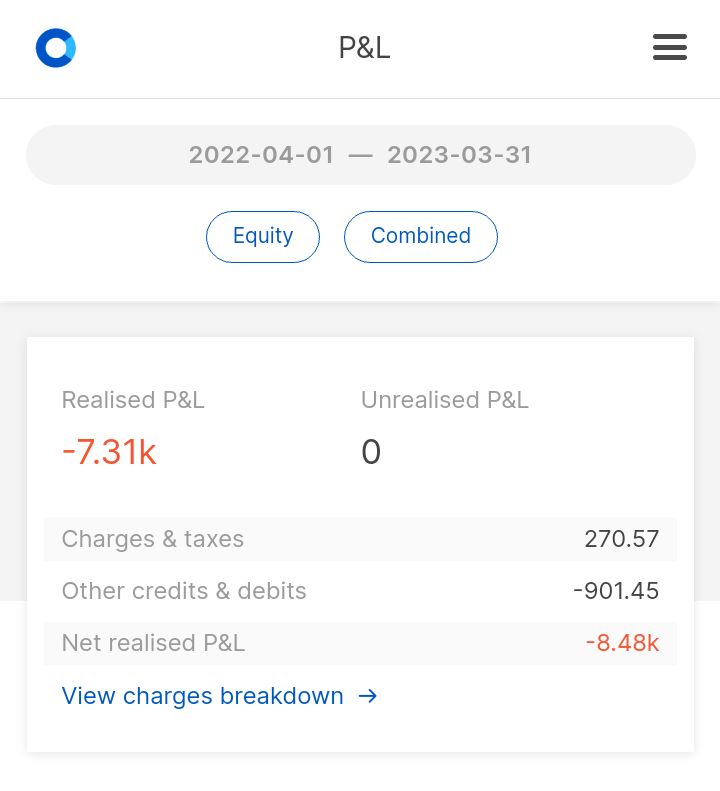

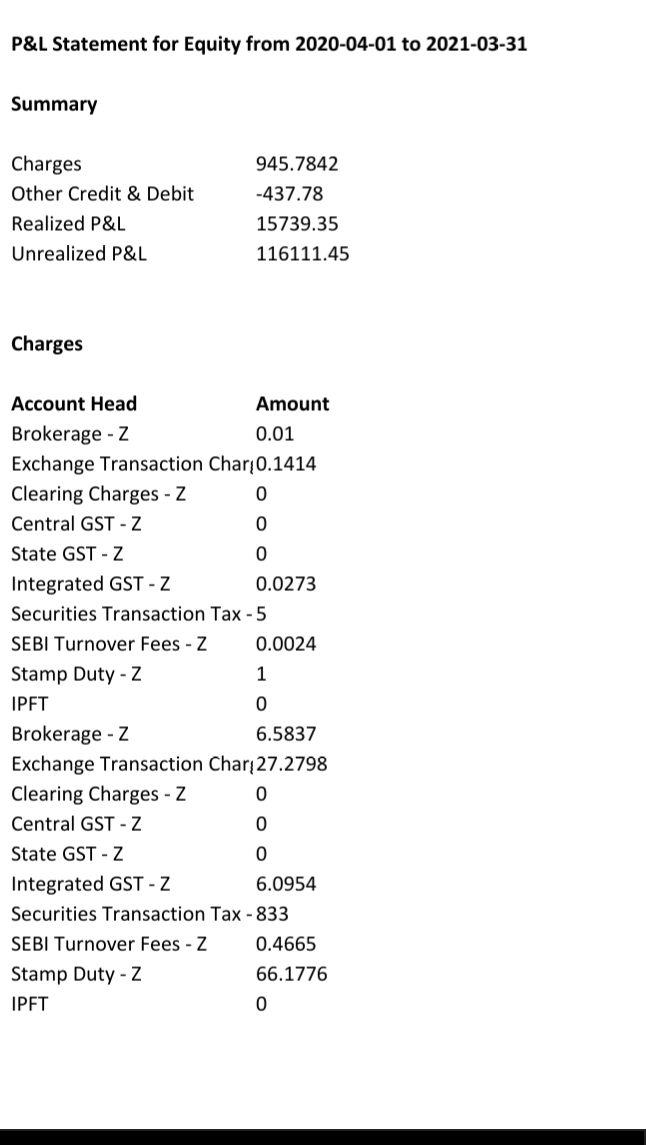

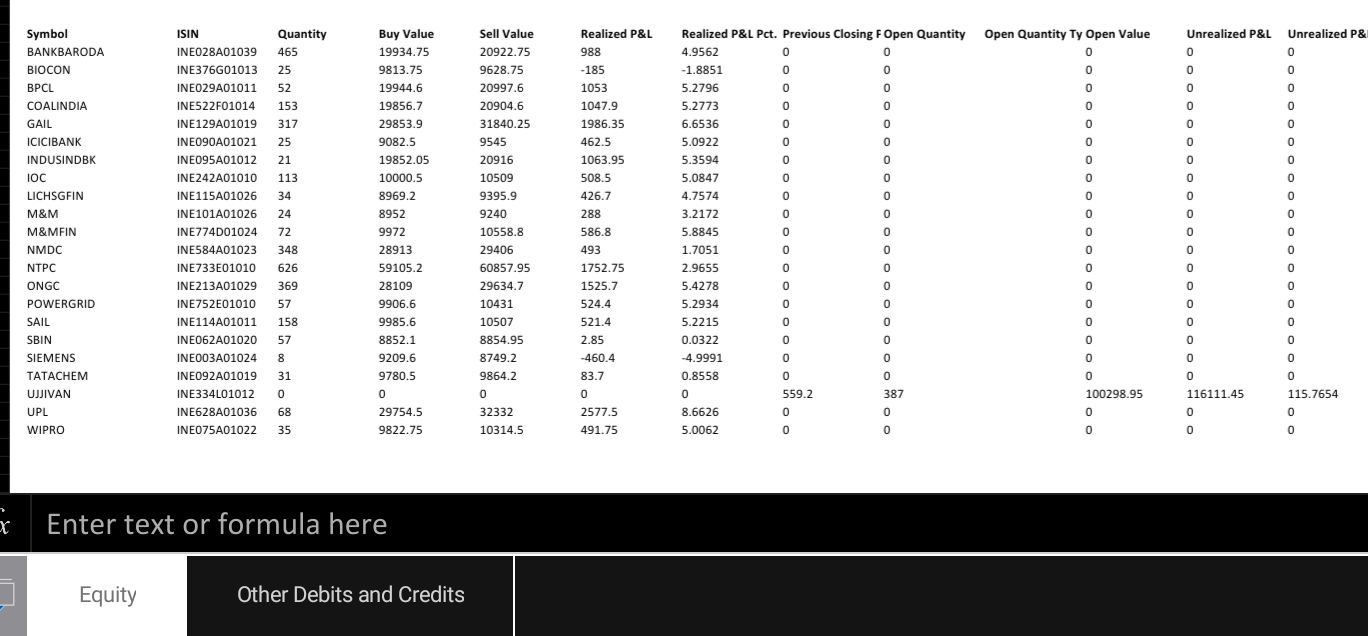

My Track records for Equity segment

From 2019 to 2023

Trading capital ranges from 10k to 50 k

Most of the time

Going by conventional wisdom,

taking a loan (at 20% interest) and trying to earn more than the interest payments is a fool’s errand.

And so far in this topic thread there is nothing to prove that you might be an exception.

@Sriram_Venkatesalu regarding the P&L summaries you posted,

whatever are the opportunities you utilised to generate the profits in the recent couple of years?

What level of confidence do you have that the same opportunities still exist,

and will exist for the next 12 months?

(till you generate returns from the market to repay the loan and still have something worth leftover)

Alternately, if/when such opportunities no longer exist in the market,

do you have the confidence that you will find other equally good

(or more lucrative) opportunities to trade?

If yes, then what gives you that confidence?

Is that irrational optimism or is there any prior experience backing that?

Did you understand what @Zodiac mentioned in their reply above ?

Do you still disagree with the assessment that you did NOT have sufficient risk management in place?

(…and hence attempting something similar with borrowed money, is going to be a disaster)

3 to 5% per year?

I gotten returns around 3% to 5 % per month in Equity segment. But it’s not a sure method in all the time.

1 Like

If you have a monthly compounding rate of 5% - then there is no issue in getting a loan for 20% interest. Because your equity returns ~ 80%. (https://www.thecalculatorsite.com/finance/calculators/compoundinterestcalculator.php)

A better way to approach this is use the margin trading facility. If you are sure your equity research and buy/sell decisions use MTF. Not sure if zerodha is providing it now, but other brokers charge you from 7 to 12% annual interest.

Stay away from FnO using loans even if you are able to generate 500 per day. Firstly a 75k top up is not going to do any value add for FnO activity. Secondly the risk is higher - a month’s earnings can be taken out in a day.

3 Likes

Taking loan for trading is one of the worst idea.

1 Like

Pure disaster. Even 100% successful strategy ppl should not take loan which is not payable by them in an instant.

Lots of things are there before trading.

#1 insurance

#2 emergency fund

#3 savings

#4 investment

#5 later comes the so called trading.

Orders should not be shuffled , item should not be ignored.

Trading with Bank loan is bad idea

Trading with NBFC loan is worst idea

Trading with loan shark loan is like surrendering yourself to them as a slave.

in case some emergency happened you are unable to trade, unable to earn, unable to pay, imagine a situation

Always simulate worst case scenario first then best case scenario assume both happens in ur life, think of managing both the situations. is it possible to manage ? ask yourself, you get clear answers