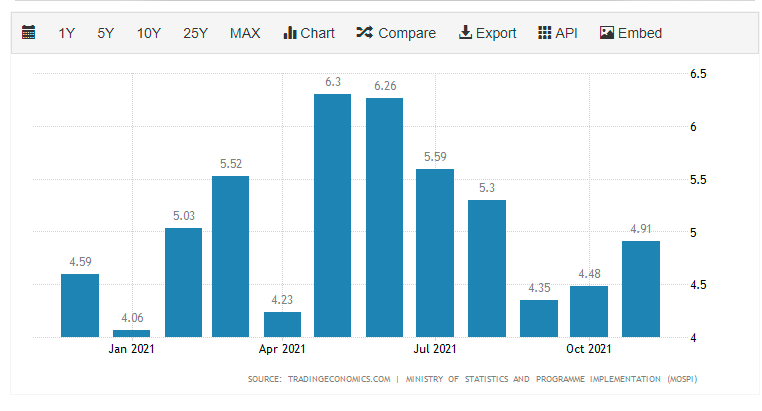

Inflation is the worry of the season. Just like all the major economies, India is seeing an inflationary spike.

Source: Trading economics

This is causing a lot of worry among investors because inflation reduces your real returns. But before we get down and dirty, just some basics.

In a very simplistic way, real returns = nominal returns minus inflation. For example, if Sensex gave 10% returns and the inflation was 4%, 6% is the real rate of return. The reason why it’s important to calculate your real rate of return is because inflation reduces the purchasing power of your money. Rs 100 in 2020 will be worth less in 2021 because prices would’ve risen due to inflation which reduces the purchasing power.

I just wanted to run a quick and dirty analysis of how the board asset classes would’ve performed. I have deliberately kept this simple because I wanted to look at this from the point of view of simple retail investors who invest through SIPs regularly.

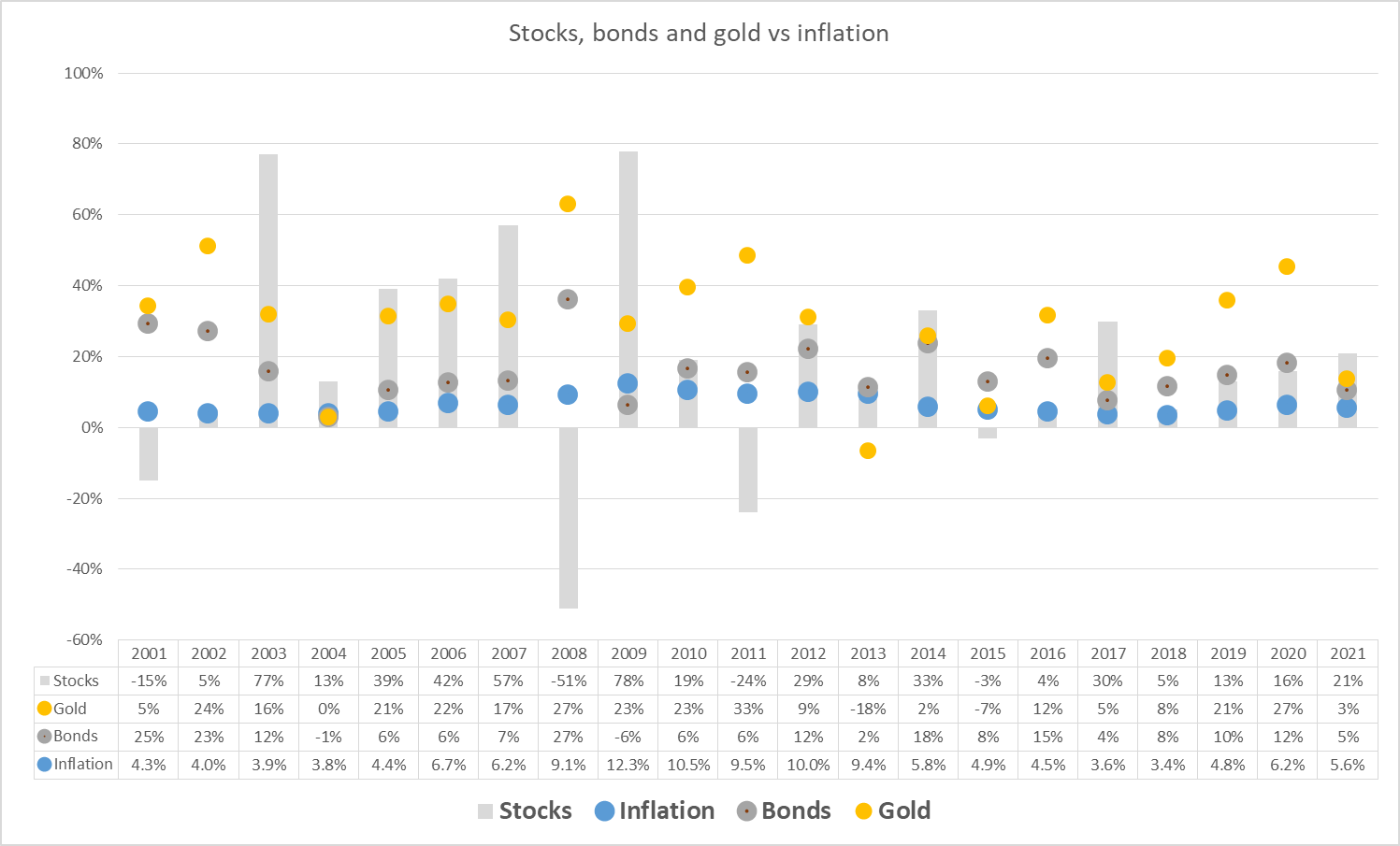

Here are the annual returns of Sensex, Bonds and Gold from 2001 across multiple inflation cycles.

Stock = Nifty 50 TRI Index. Bonds by the I-Sec Sovereign Bond Index/10-year constant maturity. Gold by INR Price of Gold/Goldbees

A few observations

- Equities are by far the best hedge against inflation

- Gold is good too but can go a long time doing nothing plus what this image obscures is that gold is quite volatile and can fall sharply as much as equities. So, do you want an equally volatile asset class in your portfolio is a question you need to ask yourself

- Bonds represented by long term bonds or gilt fund equivalents can be quite volatile. Apart from the interest rate risk, they have duration risk, so gilt funds aren’t for everyone. For most people, a mix of short/intermediate AAA bond funds are the best way to go.

- Don’t just go by the nominal bond returns. Real bond returns = bond returns - inflation.

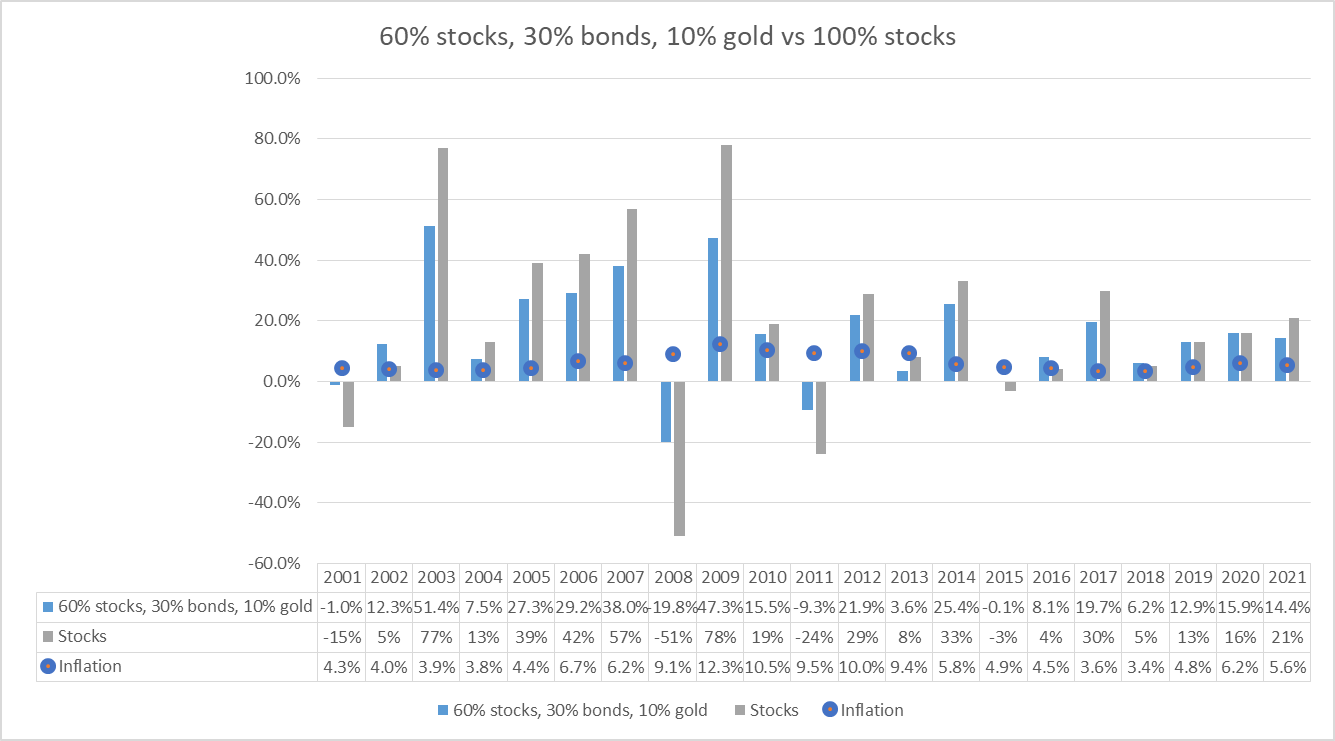

Next, I looked at how a portfolio of stocks, bonds and gold would’ve done. A hypothetical portfolio of 60% stocks, 30% bonds and 10% gold

Even in high inflation periods, this portfolio has done reasonably well. So, at least to me, the best thing for most retail investors to do is to ignore this inflation talk and just stick to basic diversified portfolio.

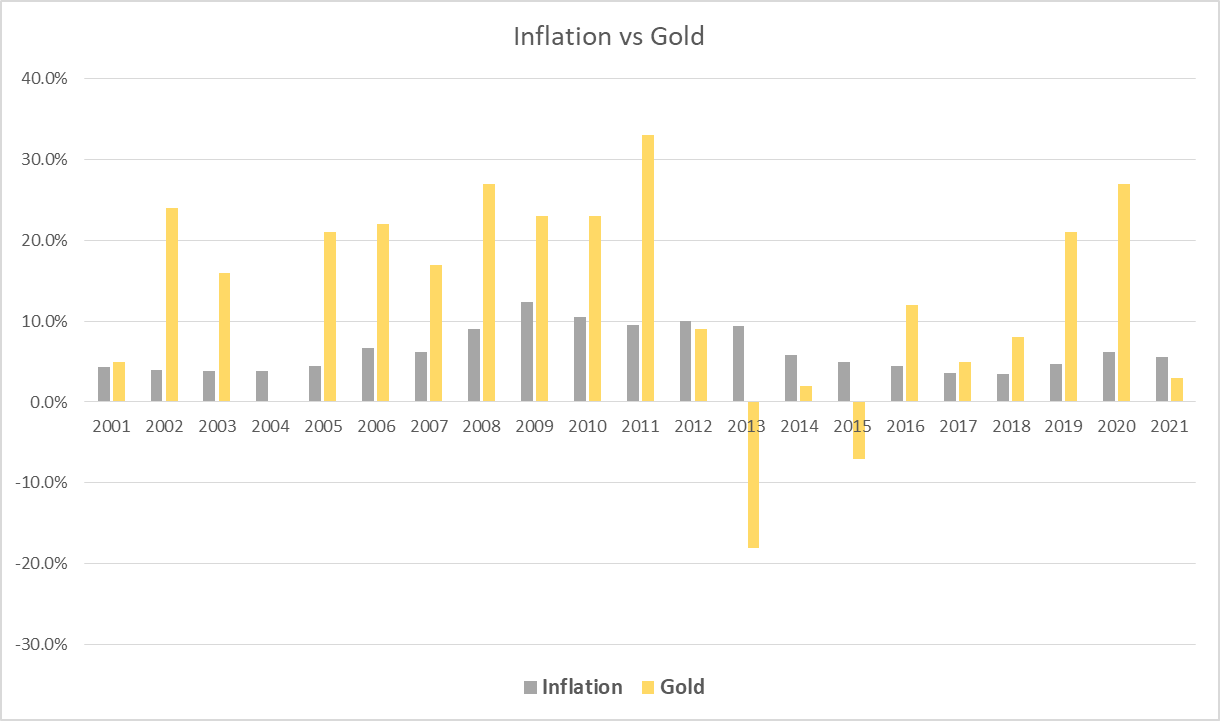

Just to reiterate, contrary to popular opinions gold isn’t a 100% inflation hedge. It can underperform for long periods even in inflationary regimes. The best example is 2020-21, gold is negative while inflation has been rising. So the best way to use gold is to not rally go overboard with allocating too much and mix it reasonably in a portfolio if you think it’s a good idea to have exposure.

The only exception to this is you jack up your exposure to gold if you are taking a tactical view on it.

A few other things

- This analysis was limited to 3 of the most common asset classes available to everyone.

- In times of inflation commodities have done well but they are quite volatile. Moreover, there’s no easy way for Indian investors to directly invest in commodities. One alternative is to invest in equities that are beneficiaries of commodities but the risk is that they can underperform severely for long periods of time if inflation doesn’t materialize.

- I have a feeling that tactical exposure to commodities through commodity sensitive equities like oil & gas stocks, minerals, energy etc can add some extra juice to your portfolio but I haven’t analysed this. By tactical I mean, you need to time your entries and exits. Buy & hold is a terrible strategy.

- In another post, I’ll try looking at how various sectors would’ve done in inflationary periods for a more granular look.

- I’m curious to see how these floating rate funds would’ve done.