We have been hearing a lot about strong sales across the board in the realty space and I was keen to read more on the underlying fundamentals that’s enabling this trend.

HDFC Securities shared a comprehensive research report on the Indian home loan market and here are some of the key themes and highlights from it:

Home loan market to double by FY28

-

India’s home loan (HL) market at INR 26 trillion and 17% of overall credit is poised to double by FY28E at a secular pace of ~15-16% CAGR during FY23- FY28E. Including the developer funding portfolio of ~INR3.5trn, the combined housing finance market is at ~INR 29.5 trillion.

-

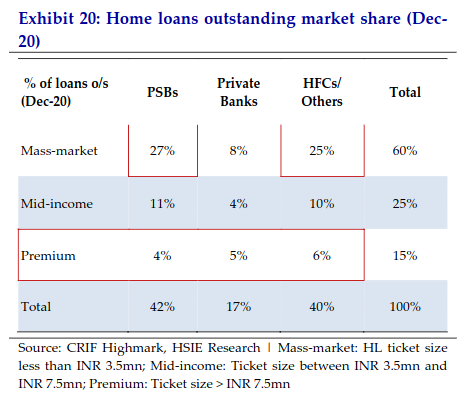

The HL market can be segregated across lender type (banks/HFCs), transaction type (primary/secondary) and customer profile (mass-market/mid-income/premium).

“Where are we in the cycle?”

Housing cycles could typically be broken into four key phases

a) Recovery phase—witnessing early pick-up in sales/prices, post a down cycle;

b) Expansion phase—steady traction in asset prices/sales;

c) Hyper-supply phase—increase in speculation activity from buyers as well as developers; d)Recession phase—correction in asset prices and slump in sales

What’s happening globally?

- Globally, there was a slowdown in housing after a strong housing upcycle. “Easy money” during the covid pandemic had driven property prices sharply across several markets. However, the sharp rate hikes in order to contain inflation has led to declining affordability with dampening of demand for property, leading to price corrections. With the tightening liquidity across the globe, several markets are now in the early stages of a recession cycle.

Low mortgage penetration, affordability remains key

India’s urban mortgage penetration remains significantly low. While housing demand continues to remain high, affordability and pace of urbanization remain the key for translating into housing purchases.These variables turned favourable during the pandemic with repo rate at 4% and a muted increase in home prices.

Compared to other countries, India’s low mortgage penetration, in terms of home ownership or housing loans, offers significant room for improvement on the back of rising affordability.

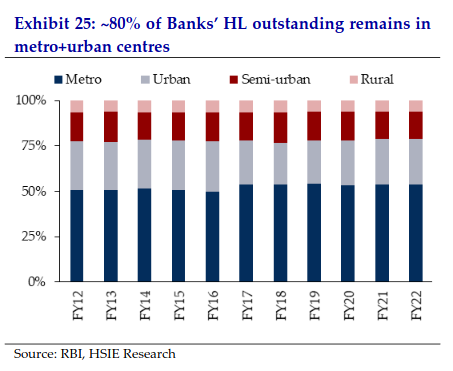

80% of housing loans come from metro+urban cities

Preference for luxury homes is on the rise

The revival of housing demand since the pandemic has been anchored on increased preference for home ownership as well as significant up-scaling/premiumisation among homebuyers with a preference for bigger houses and better-rated developers. This is reflected in increasing contribution of mid-income and premium ticket-sizes for both lenders as well as developers.

Commercial real estate (CRE) - An Overview

-

Bank credit to commercial real estate (CRE) has traditionally been limited to Grade-A/Large developers (few exceptions). With rising consolidation and increasingly disciplined approach by developers.

-

With the rise in demand for CRE, banks are incrementally gaining comfort in taking CF exposure to mid-sized and smaller developers.

NBFCs/HFCs - gradual revival from developer crisis

- NBFC/HFC developer book has come off significantly (by ~30-40%) since the 2019 crisis for several lenders. However, revival in housing demand, coupled with an increasingly disciplined approach by developers and wafer-thin margins in retail home loans, is leading to HFCs relooking at the developer funding space.

Banks are in the driver’s seat

Banks gained 6% HL market share during FY18-22 and are further looking to add onto their dominant ~67% market share.

Public sector banks are making a strong comeback

PSBs have been aggressively chasing market share gains in home loans, with surplus capital and deposits, little distraction from asset quality and growing impetus for credit growth. They have emerged the most aggressive on pricing (base home loan rates even lower than SBIN, nil processing fees, etc.) and loan-to-value.

Pace of rate hike transmission to customers

The sharp repo rate hikes during FY23 (250bps) have resulted in further margin expansion (spread over 1-yr TD rates in excess of 50bps) for the HL portfolio of banks and HFCs on the back-book as well as incremental home loans.

The share of loans priced below 8% has shrunk from ~82% in Mar-22 to ~13% in Dec-22, while the share of loans priced between 8%-10% has increased from ~12% to ~76% within the same period.

Home loans contribution to overall portfolio

Home loans constitute a lion’s share of banks’ retail portfolios with ~14% of overall loan book and ~50% of retail loan book as they generate healthy RoE, particularly for banks with strong low-cost deposit franchise (highlighted earlier), and strong underwriting (low credit costs).

Strong comeback by HFCs

- After a 3 year long under-performance caused mainly by the 2018-19 crisis, HFCs have gradually reverted to growth phase with strong housing demand, ceding of asset quality woes and relatively improving liquidity environment.

Regulatory headwinds and arbitrage for HFCs

- The slew of regulatory changes by RBI, post taking over as the regulatory authority for HFCs from NHB, has led to rising regulatory costs such as LCR norms, NPA recognition norms, floor for exposure towards housing finance etc., leading to a gradual impact on profitability for most HFCs.

-

HFCs have been kept out of the PCA framework compared to NBFCs.

-

However, home loan pricing continues to be the biggest regulatory arbitrage for HFCs compared to banks. Banks have to mandatorily offer external-benchmark-linked floating-rate or fixed-rate loans to retail/MSME customers, with no such restriction on HFCs. This arbitrage has significant implications, particularly in a declining interest rate environment, with lopsided monetary transmission for the customers of HFCs