@somnath248 Can an Indian citizen open an RFC account? I am confused about this because as per RBI (Reserve Bank of India - Frequently Asked Questions) it seems possible to do this (as per my limited understanding of the confusing legal language)

Q1. Who is a person resident in India?

Answer: Sec 2(v) of the Foreign Exchange Management Act, 1999 (FEMA) defines a person resident in India as:

(i) a person residing in India for more than one hundred and eighty-two days during the course of the preceding financial year but does not include-

(A) a person who has gone out of India or who stays outside India, in either case-

- for or on taking up employment outside India, or

- for carrying on outside India a business or vocation outside India, or

- for any other purpose, in such circumstances as would indicate his intention to stay outside India for an uncertain period;

(B) a person who has come to or stays in India, in either case, otherwise than-

- for or on taking up employment in India, or

- for carrying on in India a business or vocation in India, or

- for any other purpose, in such circumstances as would indicate his intention to stay in India for an uncertain period;

(ii) any person or body corporate registered or incorporated in India,

(iii) an office, branch or agency in India owned or controlled by a person resident outside India,

(iv) an office, branch or agency outside India owned or controlled by a person resident in India;

But when I checked different bank offerings (like ICICI, HDFC, Federal Bank, Bank of Baroda, IDBI Bank, etc) in this area, all seem to be catering specifically to NRIs or PIOs and not Indian citizens

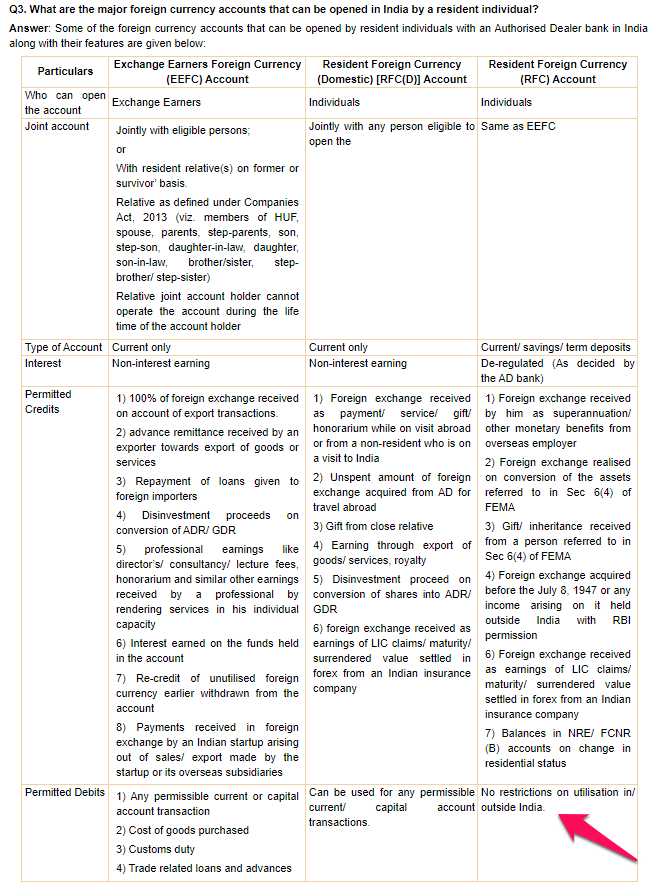

There is an RFC Domestic account (which @suryateja also mentioned in their post - referenced below) and it seems that it is possible for an Indian citizen to open that account (Axis Bank’s offering specifically mentions this is for Indian Resident and not NRIs)

But there are two major problems with RFC Domestic Account -

-

In the SBI offering, on their Terms and Conditions page, they mention -

Special Condition

Conversion of account balance:- As per RBI guidelines, the sum total of all the credits received in RFC (Domestic) account during a calendar month, less amount utilised, should be converted into Indian Rupees (crystallise) on or before the last working day of the succeeding calendar month after making adjustments for forward commitments.

This makes keeping foreign currency impossible for over a month in these accounts as they get auto-converted to INR.

-

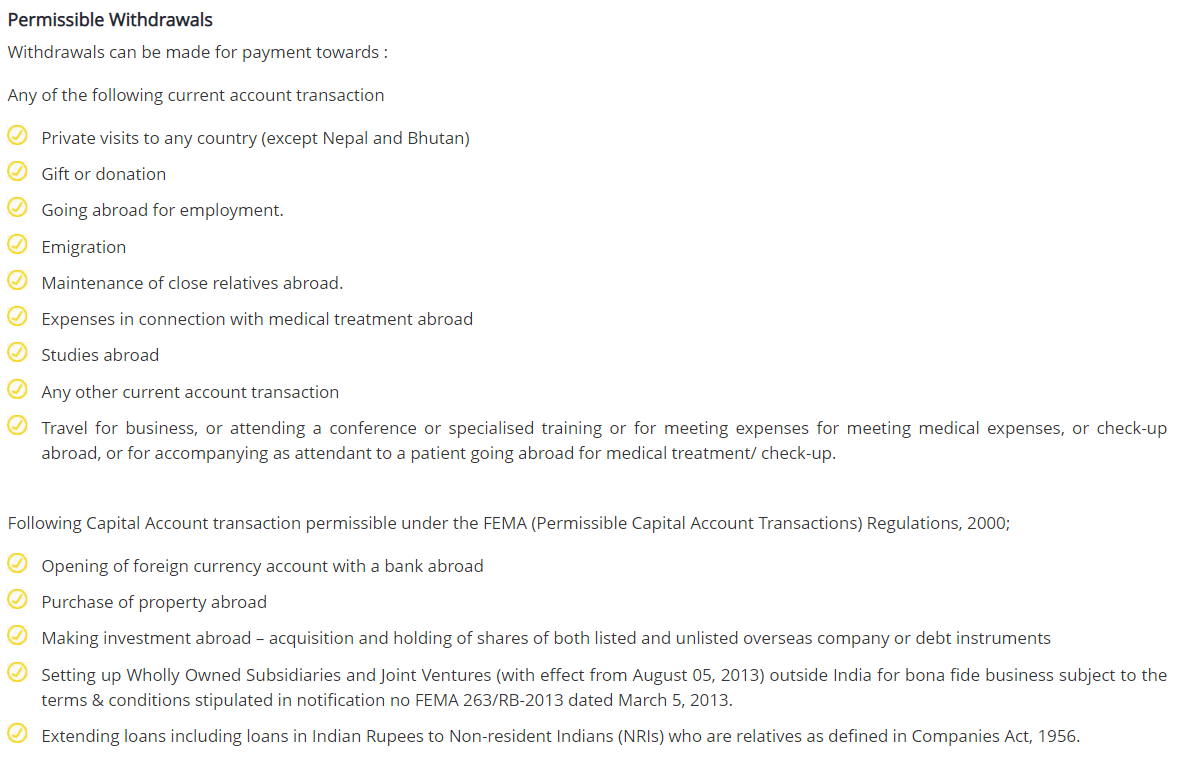

As per the RBI FAQ that I linked in the starting of this post and the RBI FAQ which @suryateja referenced in their post, only RFC accounts are given exemption from LRS and not RFC Domestic accounts (screenshot of the table highlighting the difference between these account types taken from the above RBI FAQ page).

The permissible debit transactions in an RFC Domestic account (as per SBI website) -

Hence using foreign currency deposited in an RFC Domestic Account for derivative trading doesn’t seem to be possible

I am an Indian citizen (aka a “Resident and ordinarily resident in India (also known as resident)” as per the Income Tax Law) and have a source of income through freelancing work for foreign clients. Mainly, I wanted to ask If it would be possible to deposit that income directly into an RFC account (which is exempt from the LRS limitations)?

In case someone is interested, a few news articles which explain the difference between various residential statues -

- https://www.business-standard.com/article/economy-policy/are-you-a-citizen-or-resident-of-india-115011900002_1.html

- Did you know: the difference between a resident, non-resident and resident but not ordinary resident | Mint

- income tax rules for nri: What are the new rules for determining NRI status in India and how income will be taxed - The Economic Times

On a concluding note, this hypocrisy about not allowing futures/options trades outside India is entirely on a different level. On one side, it is nearly impossible to trade derivates (outside India, especially the US) for an Indian citizen (except the few types which @namitjain2890 mentioned in regards with Interactive Broker - https://www.interactivebrokers.co.in/en/index.php?f=38144&p=tradingrequirements#trading-requirements:~:text=Limited%20option%20trading%20is%20also%20available%20with%20ANY%20Investment%20Objective but that also falls in a grey area of a sort) but people from other countries (aka FII) can easily participate in the Indian derivatives market and contribute a significant amount of the volume (https://www.motilaloswal.com/markets/derivative-market/FII-Statistics.aspx). Other than the SGX Nifty 50 Index Futures (whose volumes are growing continuously as per Singapore Exchange (SGX) and Singapore Exchange (SGX) ), NSE is also part of the Part 30 Exemption program of the CFTC which allows US investors to directly bet on Indian derivatives (NSE-BSE: Investing In India Made Easier For U.S. Investors ). Everyone outside India can participate in the Indian derivative market but Indians can’t participate in any derivative market outside India. I think it would be better for NSE/BSE to collaborate with Nasdaq/S&P 500 and introduce US market futures/options in Indian exchanges itself (like SGX did for Nifty)

@siva-reddy @nithin My other question is regarding buying ETFs. As you mentioned in one of the posts earlier, buying Inverse ETF might be considered legal (sort of a grey area). Would it be legal to purchase leveraged ETFs like the ones mentioned in Most Traded Leveraged ETFs for Q4 2022?