A thread for discussing your trades, strategies, ideas, news, stories, etc.

Here’s what the markets were up to in the week gone by;

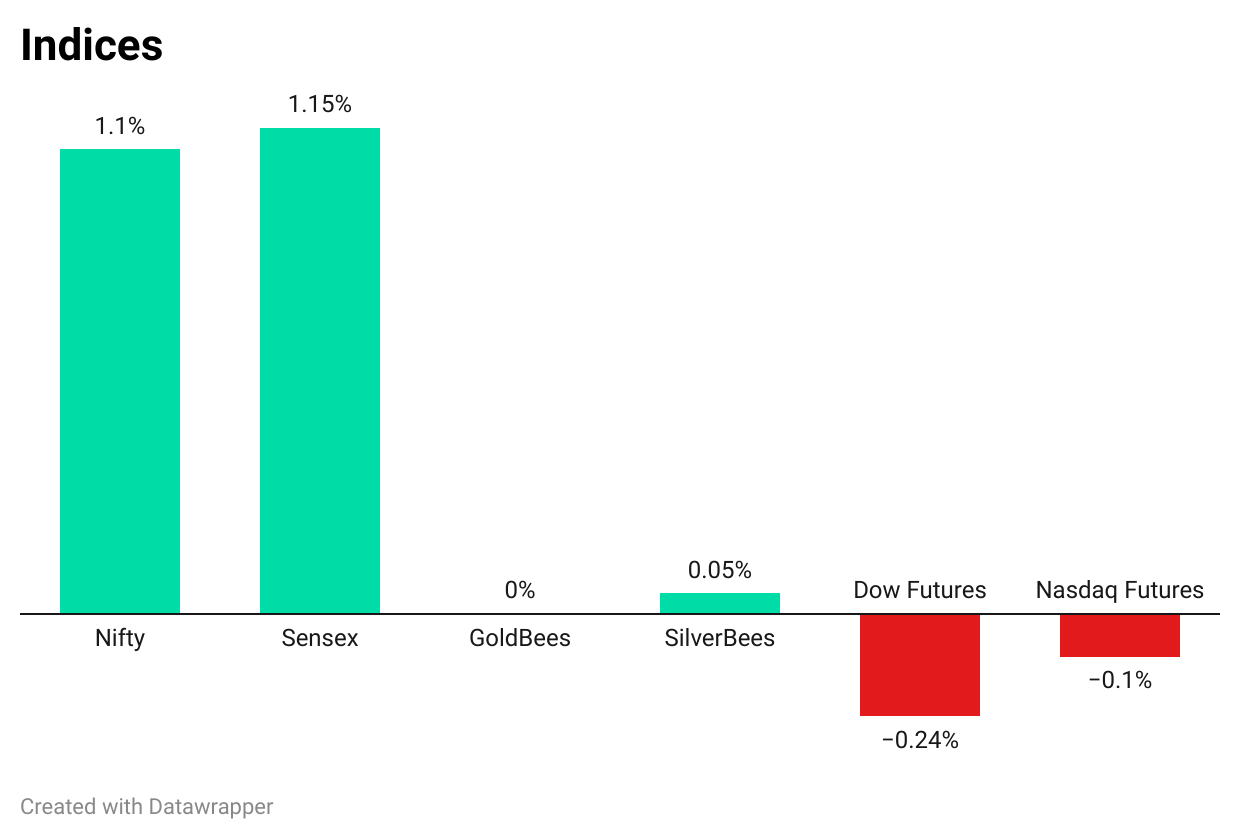

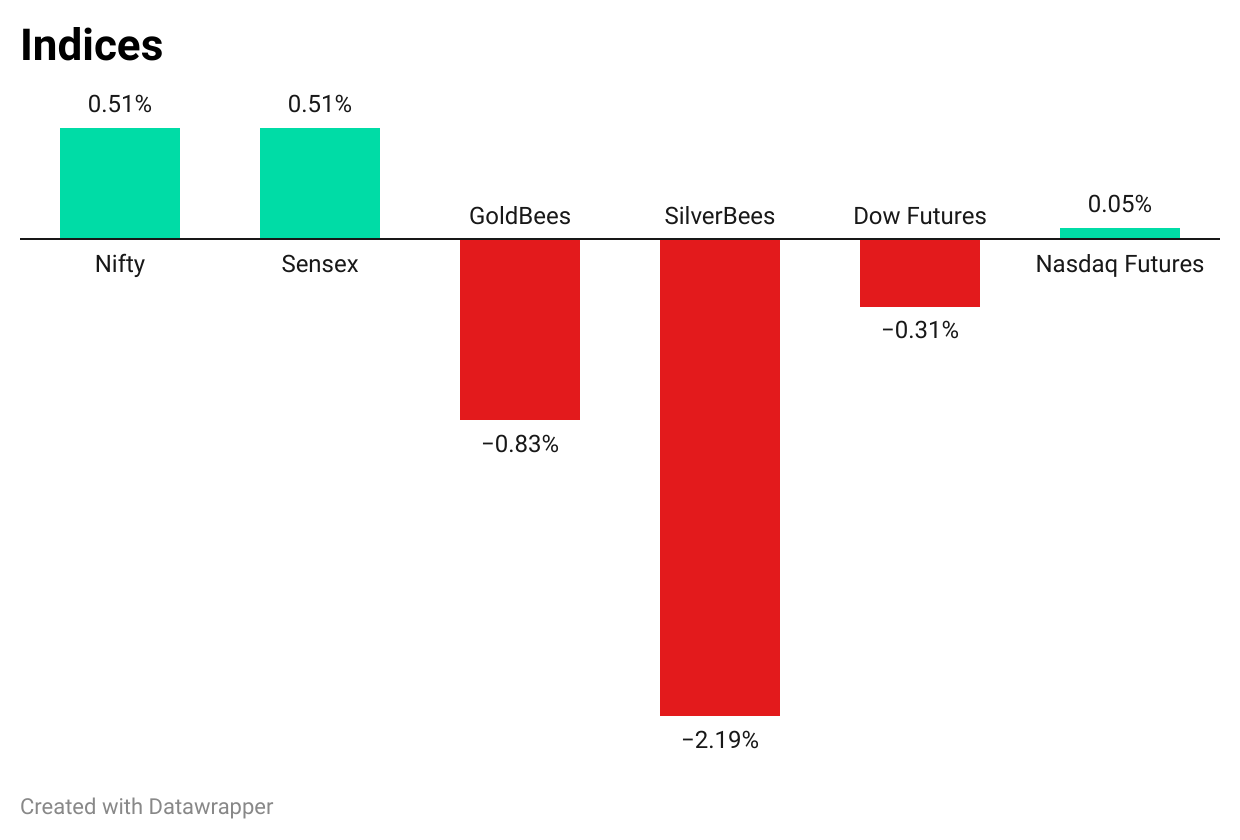

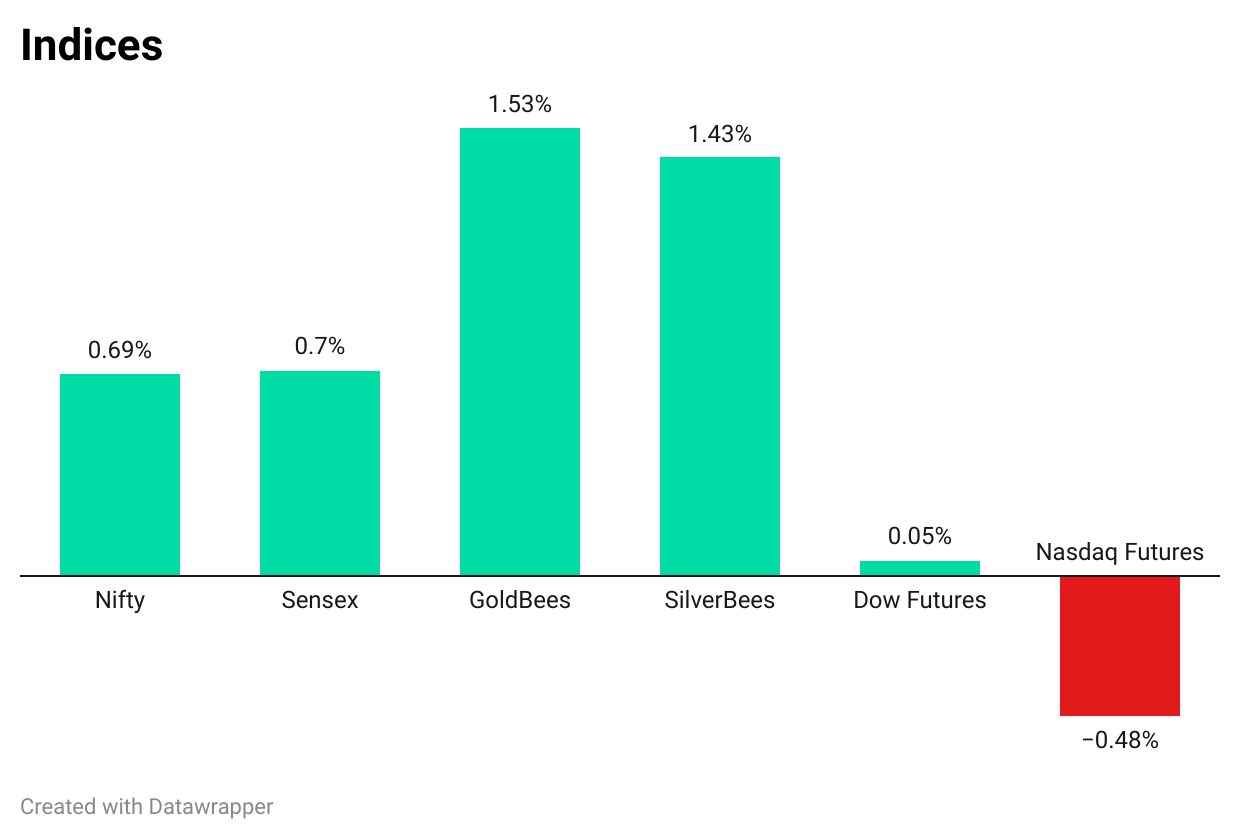

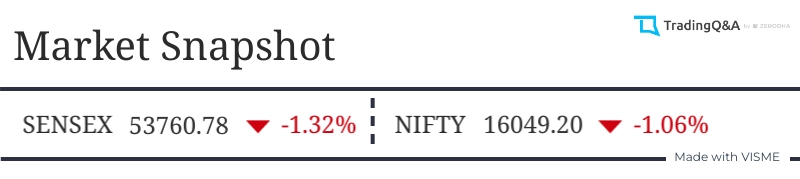

Benchmark indices snapped their three-week winning streak with Sensex dropping by around 1.3% and Nifty by around 1%.

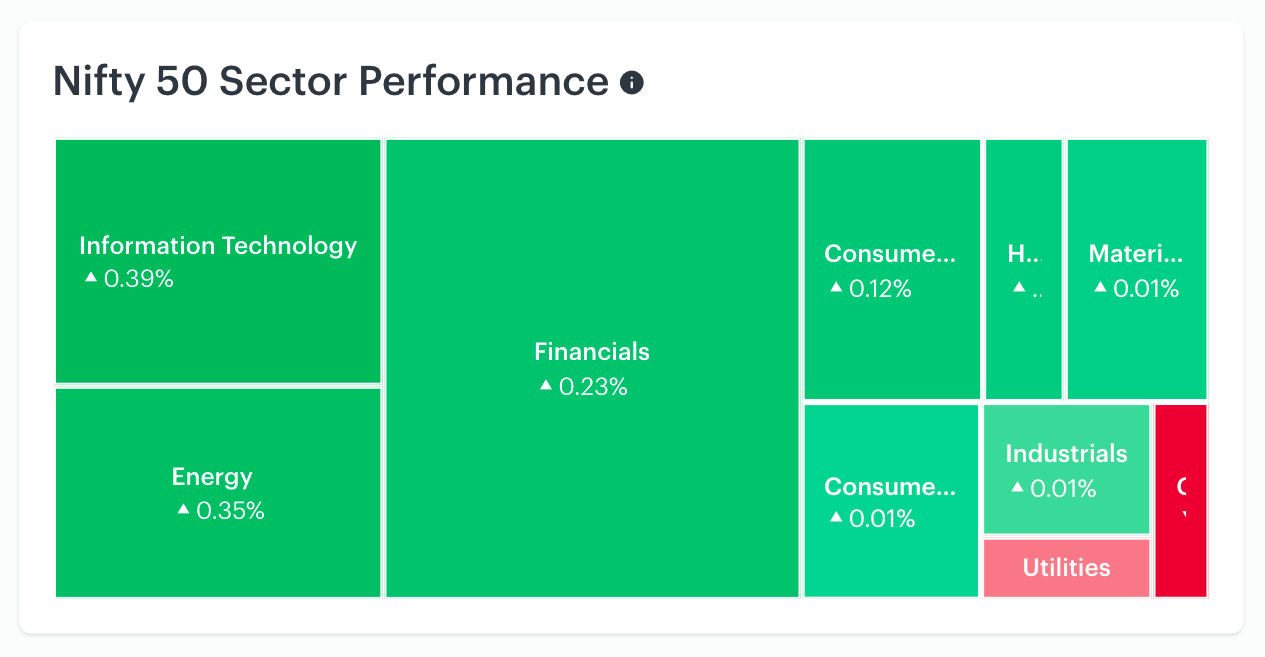

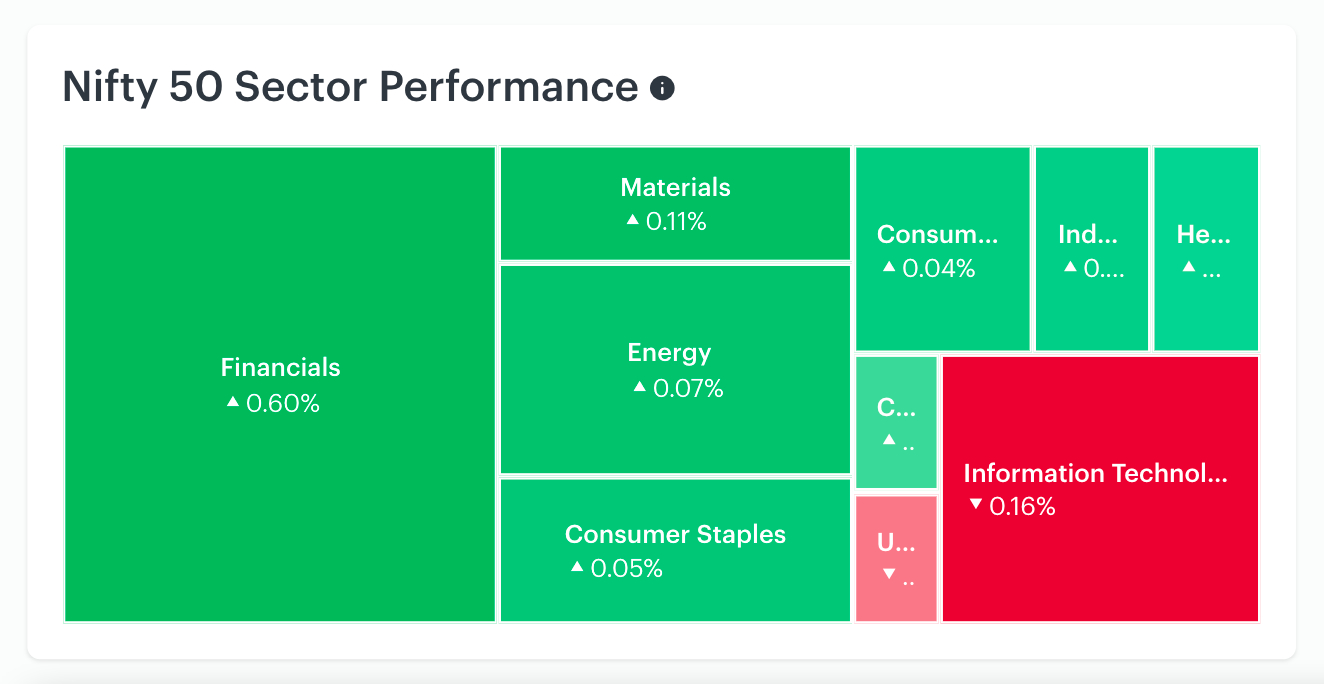

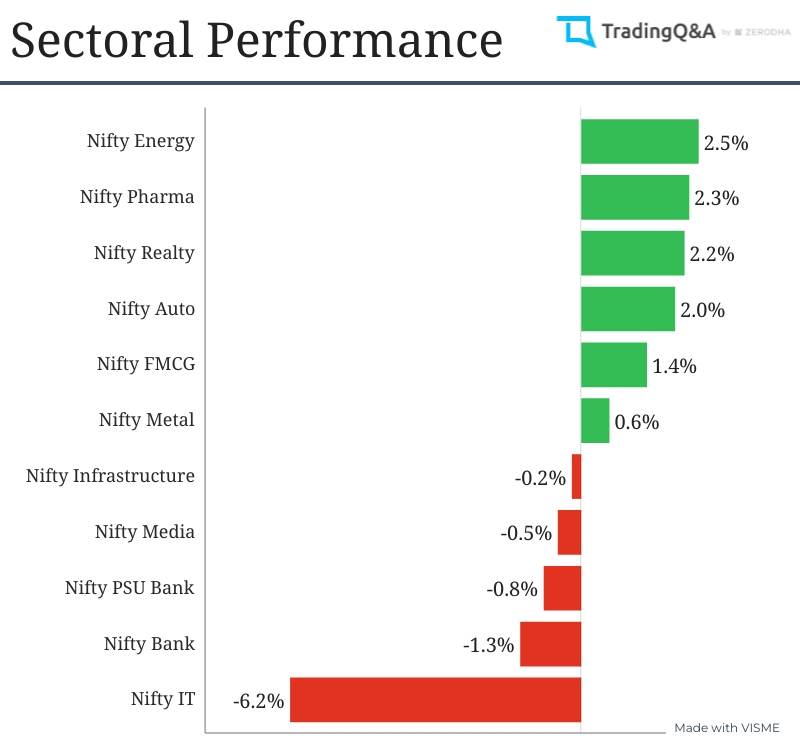

Here’s how the major sectoral indices fared. Nifty IT was the biggest loser, sliding over 6% for the week.

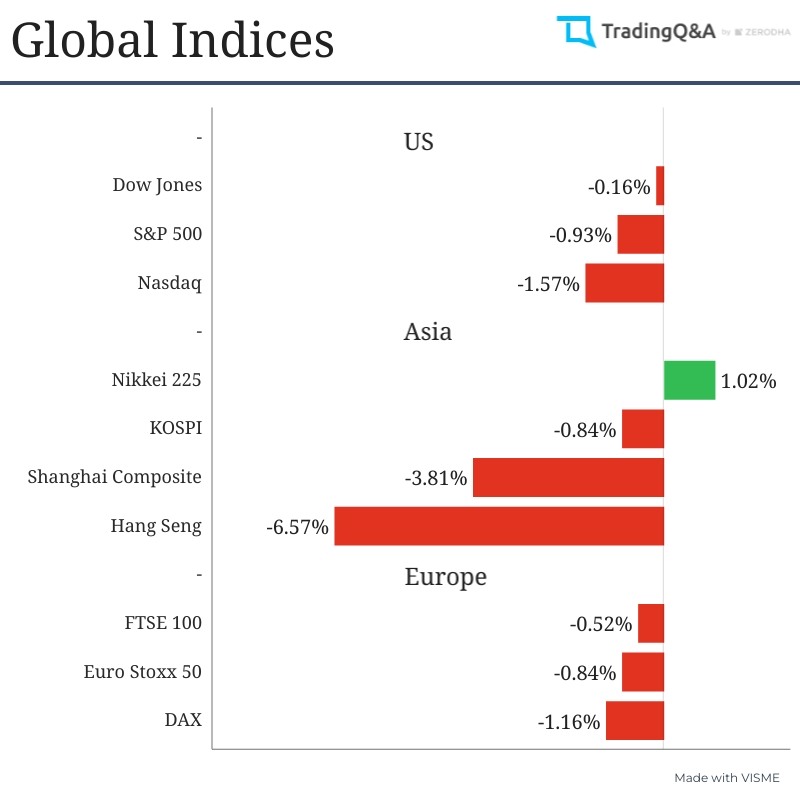

On the global front, Chinese markets were the top losers, Hanf Senf index fell over 6.7% amid a sell-off in Chinese Tech stocks. While the Shanghai Composite Index was down about 3.8% amid disappointing Chinese GDP numbers.

Inflation in the US soared to 9.1% in June. US markets however recovered from weekly lows, though ended the week in the red. Here’s how the major markets around the world fared;

Things to watch out for in the coming week;

Earnings

A busy week on the earnings front as quite a few big names will be releasing their Q1 earnings. Most notably, Hindustan Uniliver on 19th July, Wipro and IndusInd Bank on 20th, Reliance on 22nd, ICICI and Kotak Mahindra Bank on 23rd and Infosys on 24th July.

| 18th July | 19th July | 20th July | 21st July | 22nd July | 23rd July | 24th July |

|---|---|---|---|---|---|---|

| Ambuja Cements | Ceat | Can Fin Homes | Reliance | ICICI Bank | Infosys | |

| Hindustan Unilever | Havells India | Cyient | Atul Ltd. | Kotak Mahindra Bank | ||

| L&F Finance Holdings | IndusInd Bank | Hindustan Zinc | JSW Steel | |||

| Network 18 | OFSS | JSW Energy | Coforge Ltd. | |||

| TV18 Broadcast | Tata Communications | MphasiS | UltraTech Cement | |||

| Au Small Finance Bank | Wipro | PVR Ltd. | Bandhan Bank | |||

| ICICI Lombard | Syngene International | SRF Ltd. | HDFC AMC | |||

| HDFC Life | Gland Pharma | RBL Bank | ||||

| Polycab |

Key macroeconomic events to watch for

On the macroeconomic front, eyes will be on the European Central Bank as the interest rate decision is scheduled on 21st July. The Euro has been under pressure, dropping to 20-year low and reaching parity against the US Dollar. YTD the Euro is down over 11%.

| 18th July | 19th July | 20th July | 21st July | 22nd July | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Eurozone | CPI Inflation (Jun) | UK | CPI Inflation (JUN) | Japan | BoJ Interest Rate Decision | Japan | CPI Inflation (JUN) | |||

| US | Home Sales (JUN) | Eurozone | ECB Interest Rate Decision | Eurozone | Manufacturing and Services PMI (JUL) | |||||

| Crude Oil Inventories | US | Jobless Claims | US | Manufacturing and Services PMI (JUL) |