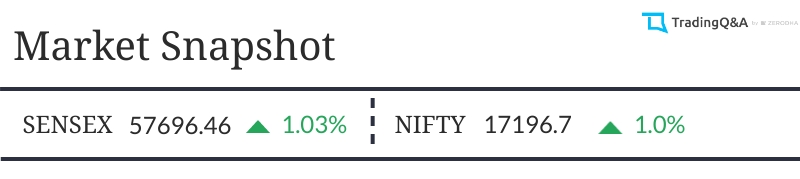

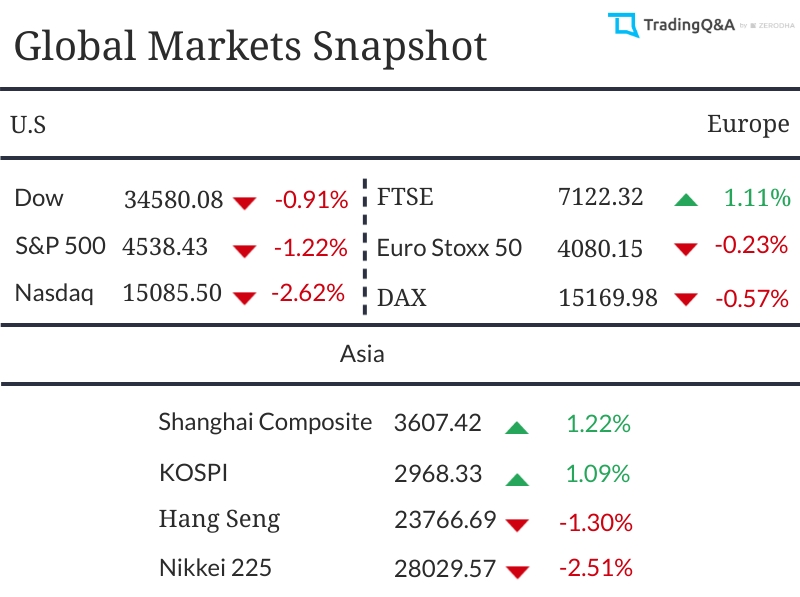

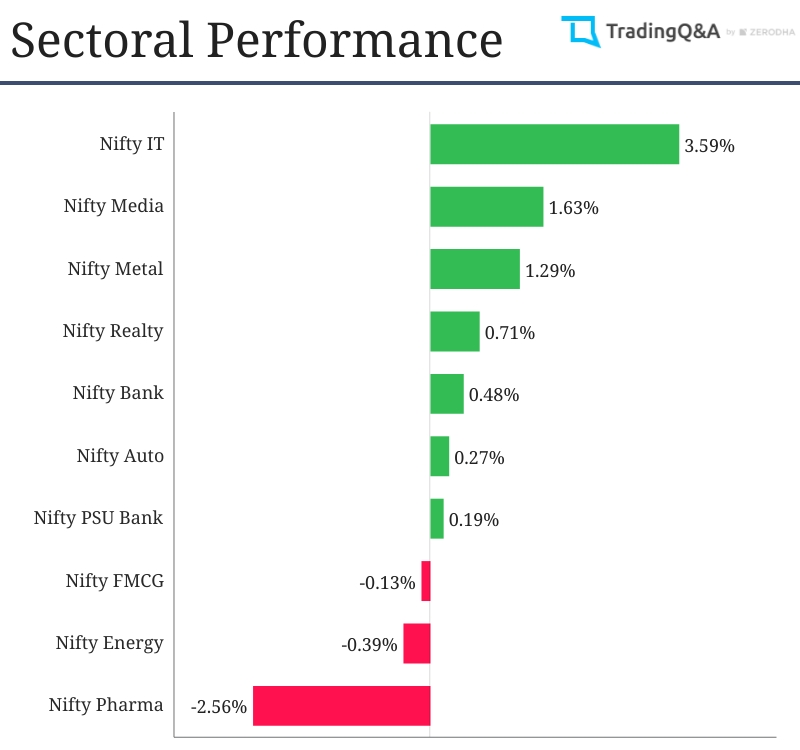

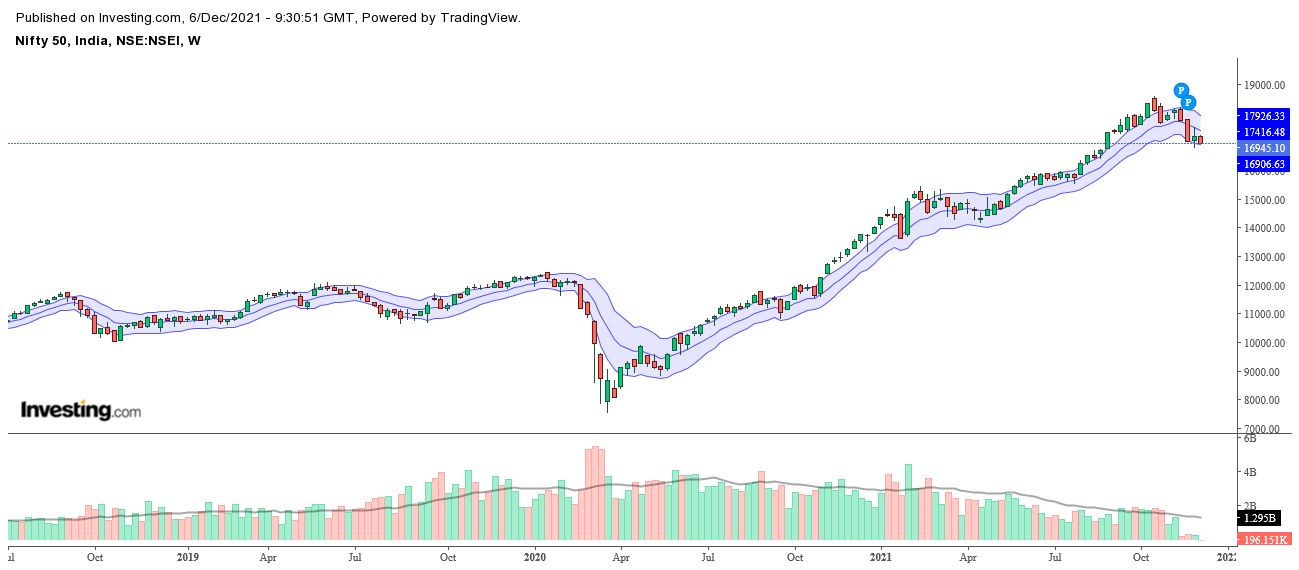

Rising spread of the new COVID variant Omicorn globally kept markets on edge in the week gone by. Nifty and Sensex managed to end the week up by around 1% snapping the two-week losing streak. Though things were not the same globally where most of the major markets ended the week in the red.

With RBI Event this week, I will be looking for buy on big dips and sell on big rise till the event is done. I think Bank niftymay outperform nifty till the event. Lets see

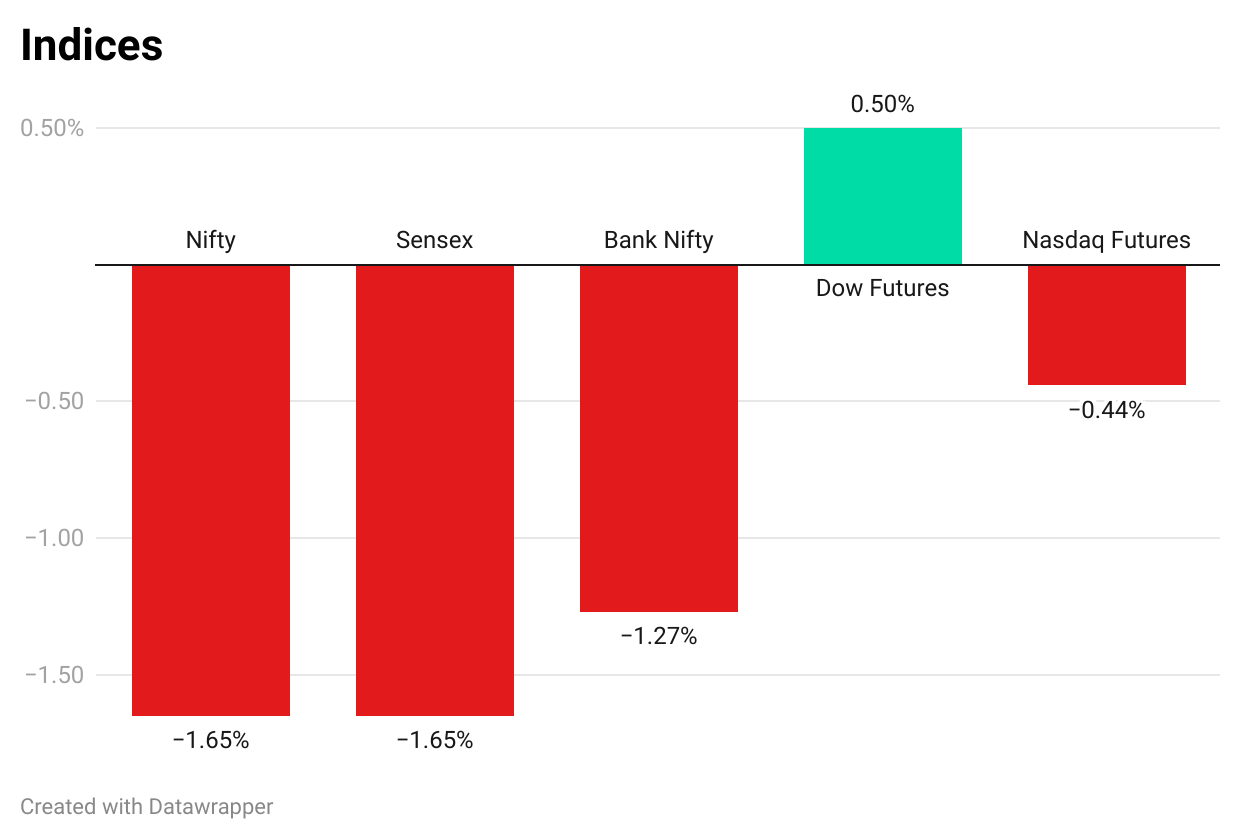

As all the major global indices are green or flat today, the fall was Indian markets specific. The below mentioned news maybe the reason for this fall.

FIIs may have pressed the panic button and sold off heavily due to this news which creates some short term uncertainty.

The markets continued their slide for the second consecutive session with Nifty and Sensex both tanking over 1.6%. US markets look set for a mixed start according to Dow and Nasdaq futures.

Brent Crude: 71.73 +2.66% USD-INR Spot: 75.42 +0.34% India 10Y bond yield: 6.36% -0.14%

Looks like we will have an inside bar candle today. Sell on rise and buy on big dips and overall within the range. This is usually what happens when there is an event. Big guns prepare and position themselves for the event.

Reliance and Abu Dhabi’s Ta’ziz to launch chemical project joint venture worth $2bn in Ruwais, UAE.

FMCG companies, Britannia, ITC, Nestle, HUL amongst others received approvals for their applications for investment under the PLI scheme in food processing.

Strong premium growth for Life Insurance Companies in November; Industry premium up by 42% YoY, Pvt. insurers premium up by 59%.

Vodafone Idea to deploy blockchain-enabled enterprise platform; partners Tanla Platforms. More here.

Around the World

India, Russia ink 28 agreements, decide to expand cooperation in defense, space & oil: More.

Evergrande bondholders yet to be paid as crucial debt deadline passes. Story here.

View of inside bar candle kind of failed yesterday as previous days high was broken intraday yesterday and then it closed 80 points below from highs.

Global markets are on fire and Nifty actually is kind of still underperforming the globe.

I’m expecting and preferring sector specific movement to index movement today…considering the events lined up ryt from today (with RBI MPC meet to Fed’s meet next week)

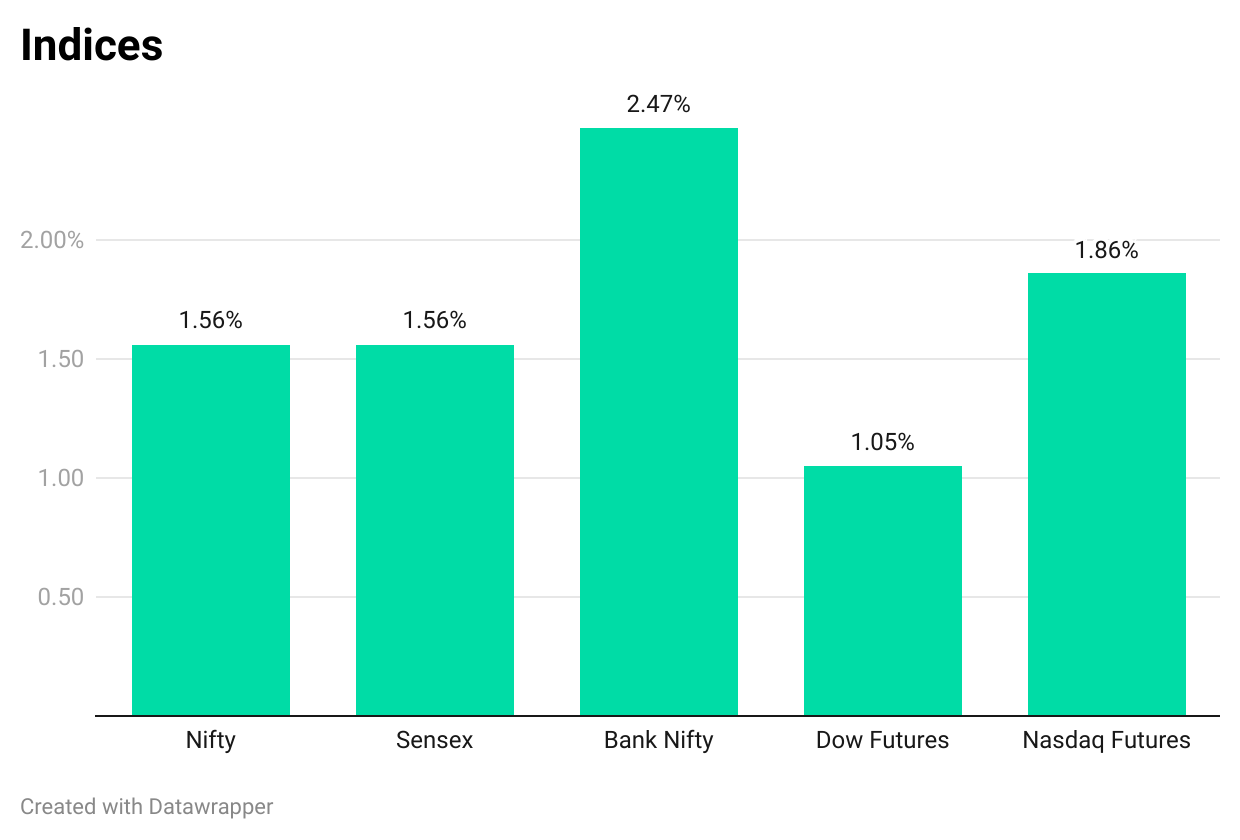

Markets climbed for the second straight day as RBI left key rates unchanged and maintained its accommodative stance. Dow and Nasdaq futures indicate a mixed start for US markets.

RBI keeps key policy rates unchanged; retains GDP projection at 9.5%: Key takeaways

Vedanta announces commitment to invest $15 billion in manufacturing display screens and semiconductors in India.

M&M signs pact with Jio-bp on EV and low-carbon solutions.

Automobile retail sales in the country dropped by around 3 percent in November as chip shortages and heavy rains in South India impacted sales across various segments: FADA

Fitch Ratings cut India’s growth forecast to 8.4% for the current fiscal; More.

Hindustan Zinc board approves interim dividend of Rs 18 per share for FY22

Around the World

Eurozone inflation will take longer to fall back to 2%, says ECB.

German Parliament elects Olaf Scholz to succeed Angela Merkel as Chancellor; Story here.

Tata Motors to invest Rs 7,500 cr in commercial vehicles in next 5-5 years, focus on EVs.

ITC will hold its first analyst’s meet on December 14.

PLI scheme in food processing: Parle Products expects 20-25% growth in exports.

Board of Bajaj Electricals authorized review of corporate restructuring. This will allow the company to unlock growth and value creation for all business segments.

Paytm Payments Bank receives scheduled bank status from RBI.

Around the World

Italy’s antitrust fined Amazon $1.28 bn for alleged abuse of market dominance.

Fitch downgrades Chinese property developers Evergrande and Kaisa Group to restricted default: Story here

Australia proposes new laws to regulate Crypto and BNPL: More

For 3 hours, market is absolutely in a range and has not moved anywhere. Trending move can start only if sustained below 17450 levels

The undertone of the mrkt is cautious as US is said to announce inflation data tonight which is supposed to come as one of the highest ever inflation number.

Indices rebounded from the day’s lows to end the final trading session of the week marginally lower. Surging by around 1.7% for the week. Dow and Nasdaq futures indicate a positive opening for US markets.

Brent Crude: 74.91 +0.66% USD-INR Spot: 75.765 +0.32% India 10Y bond yield: 6.37 +0.35%

India’s index of industrial production (IIP) grew by 3.2% in October, according to the data released by the MoSPI on Friday.

Star Health Insurance debuted at a discount of over 6% to the issue price.

Shriram Properties issue closed with a subscription of 4.6 times. The retail portion was subscribed by over 12 times while QIB 1.85 times.

Passenger vehicles sales dip 19% in November as chip shortage woes continue: SIAM

LIC received approval from RBI to hike its stake in IndusInd Bank to 9.99%.

Around the World

U.K October GDP disappoints as supply chain issues and sharply rising input costs hit key sectors such as construction and car retail.

The Consumer Price Index (CPI) of the USA is forecast to rise to 6.8% (YoY) from 6.2% in October. Meanwhile, Core CPI is expected to rise to 4.9% from 4.6%.