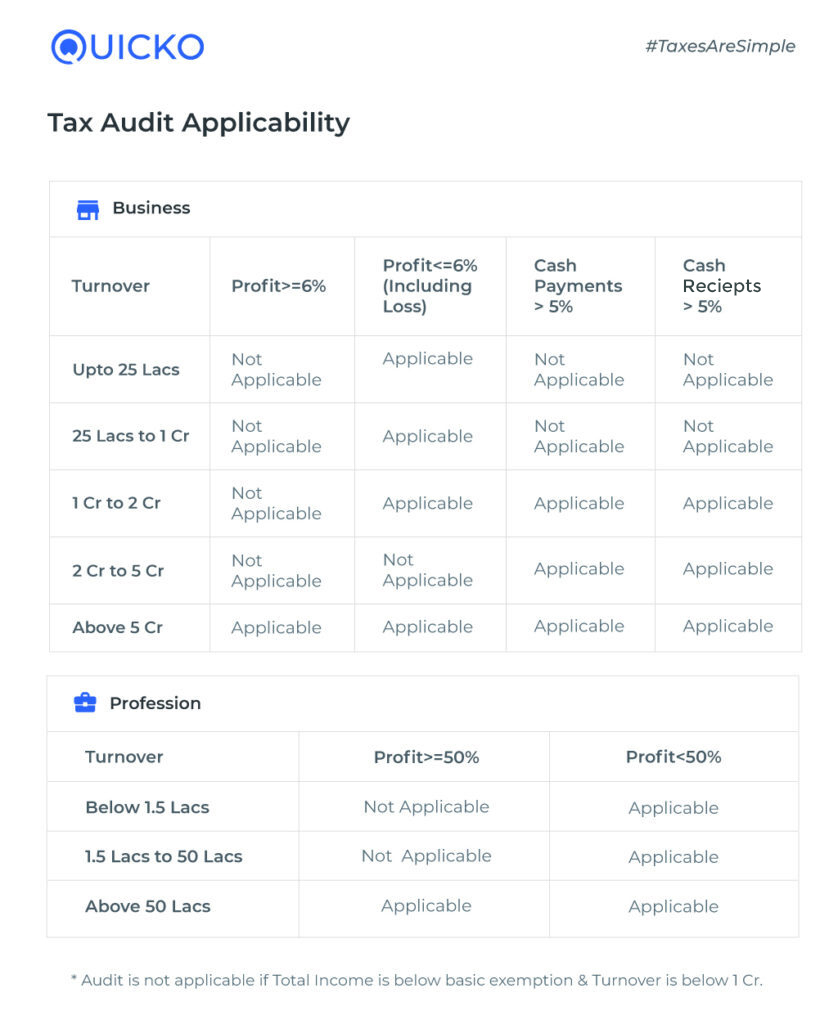

Audit applicability can be determined as follows:

- If turnover is less than INR 2 crores, Tax Audit as per Sec 44AB(e) is applicable if there is loss or profit is less than 6% of Trading Turnover and total income exceeds the basic exemption limit unless you have not opted for 44AD in any 5 previous years.

- If trading turnover is more than INR 2 Cr and up to INR 5 Cr, a tax audit is not applicable irrespective of profit or loss.

- If trading turnover is more than Rs. 5 Cr, tax Audit under Sec 44AB(a) is applicable irrespective of the profit or loss.

Further, If turnover is up to 2 crores you can opt for section 44AD if you wish to declare profits of more than 6% of turnover. No Audit is required here.

Moreover, If you do not opt for 44AD, you need to file ITR-3 along with the Profit and Loss account and Balance Sheet and take the benefit of carrying forward of losses.

Learn by Quicko – 1 Jun 20

Learn by Quicko – 1 Jun 20

Read about provisions of Tax Audit under Section 44AB of Income Tax Act. Check when Tax Audit is applicable to a business or profession.