Indian IT firms are one of most favorite investment destinations in today’s age of digitization and automation. This industry generated over $200B revenue in FY20, as per NASSCOM data. With the pandemic creating havoc across the world, let’s look at the sector-wise impact on the IT sector in the current financial year.

BFSI

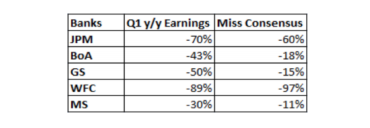

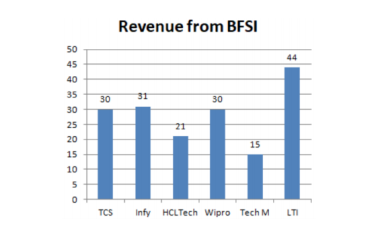

The Financial Services sector, contributing more than 30% to revenue of TCS, Infosys, and Wipro, can have an adverse impact from the decline in interest rate across the developed and emerging economies as net interest margin is severely compressed. The banks are also expected to see an increase in loan losses over the next two to three quarters, which will have an impact on their profits. Insurance may also see increased pressure due to higher claims. Global banks had poor Q1 and consensus expects that the next couple of quarters may remain weak.

Short-term pain due to BFSI, but long-term gains visible

Though the new order flow might remain low in 2020, post-pandemic technology development can prove a silver lining for India’s IT sector. BFSI expects a great opportunity for cloud, data services, and new digital bank capabilities after the pandemic. In April, JP Morgan released its annual financial report for 2019, disclosing that it would increase its technology spends by 4% versus the last year, despite the pandemic. Of this, 50% would be dedicated to ‘new’ capabilities. The other big banks such as Bank of America and Citigroup also suggested in their annual reports that their investments in digital initiatives will increase efficiency and reduce costs.

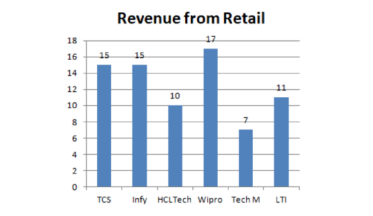

The Retail sector

This contributes more than 15% to revenue of top IT firms, has been hit hard. Non-grocery, apparel, lifestyle and fashion, and logistics companies have taken a hit globally. In the last 3-4 quarters, there was a healthy deal from this segment but we expect significant pressure on spend for the segment in the coming quarters. Though the sector’s deal pipeline is strong, the conversion rate is expected to slow down.

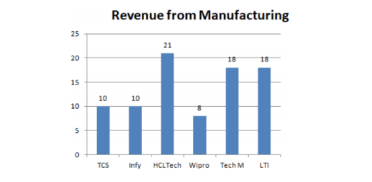

The Manufacturing sector

Manufacturing recorded a decent growth in the last few quarters. COVID-19 spread exacerbated by supply chain disruptions has resulted in a widespread closure of production facilities globally. The possibility of reduced travel in the near future will also affect the auto and aerospace industries. TCS, Infosys, and Wipro have ~10% of revenue from these sectors but HCL Tech and Tech Mahindra derive ~20% revenue from this sector.

Energy and Utility

These will be hit hard with low energy prices and demand and supply chain issues in other sub-segments. Companies in this sector are likely to see an impact on multiple fronts, including staffing, revenue, and customer preferences. Lower crude oil prices and declining demand can hit the top-line as well as bottom-line. So, they are likely to cut spending.

Travel and Hospitality

Travel and Hospitality is under severe pain and is probably the worst-hit sector due to the pandemic. Countries are under lockdown and people are traveling only if it is unavoidable. There is no tourism activity. As per the International Air Transport Association (IATA), in 2020, the industry passenger revenue could be down to $252B (44% down y/y).

With the summer months accounting for 60–65% of their yearly business, most travel businesses have already gone into huge losses. Also, the recovery is expected to be slow as people will be hesitant to travel and tourism will be very low at least for a few more months. Midcap Indian IT firms such as Mindtree and Hexaware derive more than 10% of revenue from this sector.

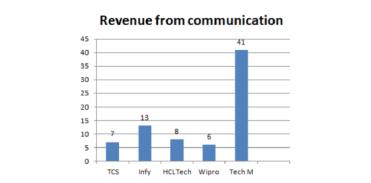

Communication

This sector is expected to have a relatively stable performance. Spend on 5G roll-out and B2B use cases of 5G may get delayed as industry players reassess capital allocation priorities. Though revenue from this segment is relatively less for TCS and Wipro, Infosys has 12–15% revenue from Communication, while Tech Mahindra derives around 40% revenue from telecom players. Tech Mahindra has a strong presence in 5G. Telecom is a relatively defensive sector in the current environment and hence telecom technology spends will be resilient. Operators across geographies have pointed to a benign impact on the low-margin handset business and on roaming charges. At the same time, the sudden shift to online sales channels and negligible customer churn due to the lock-down will aid operating margins.

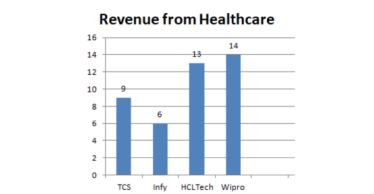

Healthcare

In Life Sciences, cancellation of elective surgery can have an impact on many sub-segments such as medical devices and even certain specialty hospitals and facilities. Overall impact will not be significant on IT spending by the Healthcare sector. In the medium term, there are significant opportunities in Tele-medicine services and virtual consultations.

Looking Ahead

Consensus expects margin to hold even when top-line growth is weak due to following reasons:

-

Deferral of wage hikes and lower hiring.

-

Lower sub-contracting cost

-

Lower travel cost due to international travel restrictions

-

INR Depreciation

-

Low marketing spend

The Indian tech industry has quickly cut cost by deferring salary increments and transitioned to work from home. Most companies are planning to permanently shift a substantial part of their workforce to work from home, which could help them save a lot in terms of infrastructure cost. Also, travel during the year will be minimum. In addition, companies are likely to choose digital meet over travel in the coming years. Depreciating INR can improve margin. Consensus estimates that a 1% depreciation in INR aids the EBIT margin for IT companies by 20–30bps.

For the detailed report, visit www.marketsmithindia.com.