Just wanted to clarify one thing before answering the query : Wint Wealth is not raising money via bonds, rather its enabling other financial institutions to raise capital via senior secured bonds. The capital thus raised the by the financial institution is thereafter utilized by them to give loans to their borrowers. The credit risk for the investors is on the financial institution which is raising the money.

To reduce risk for the bond investors the bonds are backed by loans (which comprise the security pool). Each transaction has its own eligibility criteria which defines what kind of loans can become part of security pool. These criteria(s) can include things like maximum tenor of underlying loan, maximum ticket size, borrowers from any sectors that we may want to include, concentration caps, loan to value ratio caps and so on.

I heard the bond was sold at higher price on launching day in zerodha platform.

Can u elaborate what really happened?

The ceo letter also asked apology for that

Thankyou for your reply. If you could please answer these:

a) How do you decide which financial institution can raise capital via senior secured bonds on your platform?

b) Do you have any control on whom the raised capital will be given out as loans to?

c) Does every loan have a collateral? if not what percentage of the loans have that?

d) If I am to invest money through your platform, will I be provided information as to which company my money will be raised by and where it will be lent?

e) How does the financial institution which is raising money decide whom to give the loans?

f) The prospectus does not provide the funding plan, the project appraisal plan and the schedule of implementation. How to get these information?

Thanks.

Not for all the users but for a small portion. When we ran out of the inventory, there were few users who had placed buy orders at “market price(and not limit)” while few investors had placed sell orders at price higher than Par. For such users trade got executed at prices slightly higher than Par.

Its a learning for us also. We are trying to avoid such cases in the future by (1) Educating investors so that only limit orders are placed and (2) Not allowing “market orders” at least for trades which are being routed via our website directly.

a) We do a diligence on the financial institution before onboarding them on Wint platform. This includes analyzing their financial health, systems, processes and operations. We prefer entities where 1) Financial leverage is on lower side(compared to industry) so that margin of safety is high for bondholders 2) Which are backed by Private equity funds and are not entirely promoter run 3) Have diversified existing lender base. Some of these points have been covered in our blog Which NBFCs Does Wint Wealth Choose to Work With? - Wint Wealth

b) No, we dont have direct control to which borrowers the money would be lent to. However, there are covenants placed in terms of asset quality that entity has to maintain which ensures that portfolio quality remains good. An example of such covenant is: If PAR 90 crosses 5% the bond would have to be prepaid.

c) Yes, all loans have collateral.

d) Yes, while investing you will have the details of the institution, the details of the underlying security cover etc

e) They have their internal risk policies and underwriting frameworks. This varies entity to entity and sector to sector. The framework can include details like fixed obligation to income ratio of the client, income levels, may be credit score, quality of collateral etc.

f) The funding isn’t happening towards development of any specific project. Rather money is being lent out to a financial institution. The information about entity is provided in the prospectus. You can also refer to the rating rationale. Link : https://www.acuite.in/documents/ratings/revised/27695-RR-20211011.pdf

In this market, if any bond is offering a rate of 10.5% approx when the Bank FD is between 5 to 6%, is this not “Too good to be true”.

The way I understand this product is that the financial institution are securitizing their existing loans and being sold to investors via bonds. This created additional cash for the financial institution for continuation of their business. Previously these financial institution used to issue NCD to meet their funding requirements. Now this. Is this not something called 'covered Bonds" If the collateral/security offered are of such superior quality, why are they not approaching a bank to get finance at a lower rate.

In this market bankers are running after good quality customers to increase their credit growth. When this is the situation, why are these bonds issued to retail investors.

Who are these financial institution, I am sure these are not top notch ones. The security pool etc is all good optically, how efficiently and effectively will these securities can be sold and cash realized in case of an eventuality - only time will tell. The role of the trustee holding the security is another thing which need to be tested.

Wint is just a platform or an enabler and does not take on any responsibility. It will be the bond holder vs the financial institution in the end.

I hope an investor understands all the risk of this product and then take an informed decision.

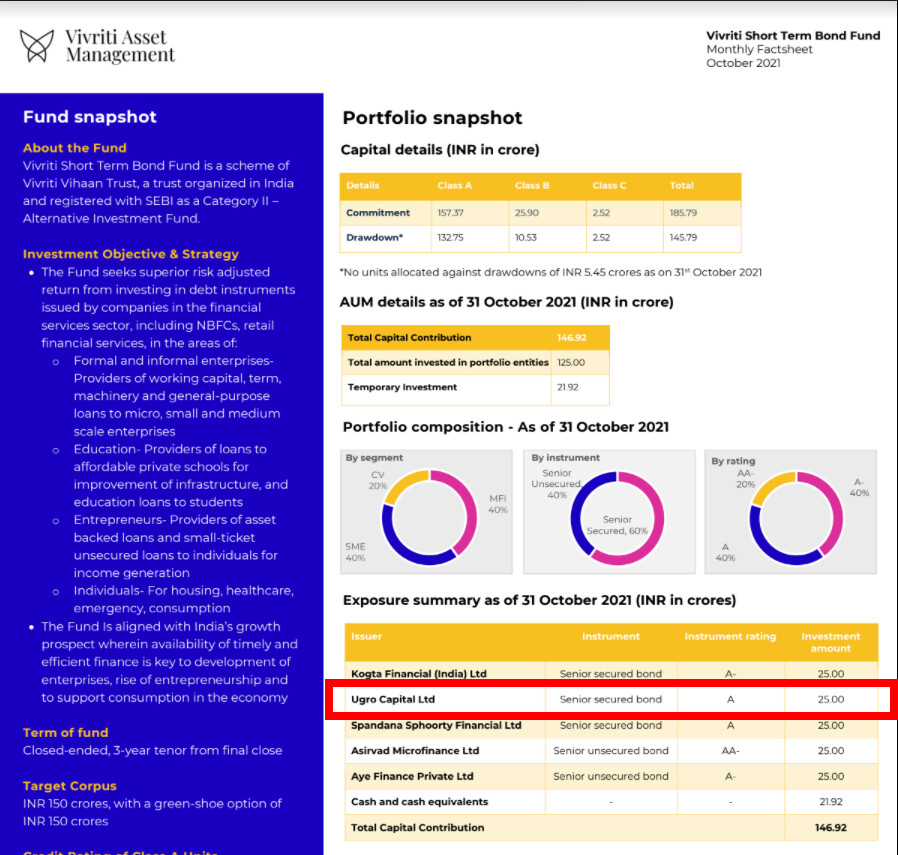

But Wint says that it has partnered with the capital raising firm UGro, what does this partnership entail @anshulgupta ? Is it just for raising the amount?

I think the partnership is to raise money while wint doesn’t take on any liability. So we need to be vigilant about nbfc while considering wint as just a broker

The live product is a secured bond(NCD) and not securitisation or covered bond.

Most financial institutions prefer having diversified sources of funding - banks, foreign investors, HNIs, retail investors, large NBFCs etc., Present NBFC also has existing lending relationships from many of the banks (they have 25+ existing lenders) - this transaction is an additional diversified source of funding.

Another benefit which many NBFCs see by raising capital from retail investors is that in addition to raising capital, it also builds brand/awareness about the entity in the retail market.

Your point is valid that even though Wint has done its diligence, the credit risk is on the financial institution and the risk/returns are much higher than risk free instruments like government securities/FDs.

If anybody is looking for similar investment avenues with equal or greater ROI and more safety then check out TradeCred.com

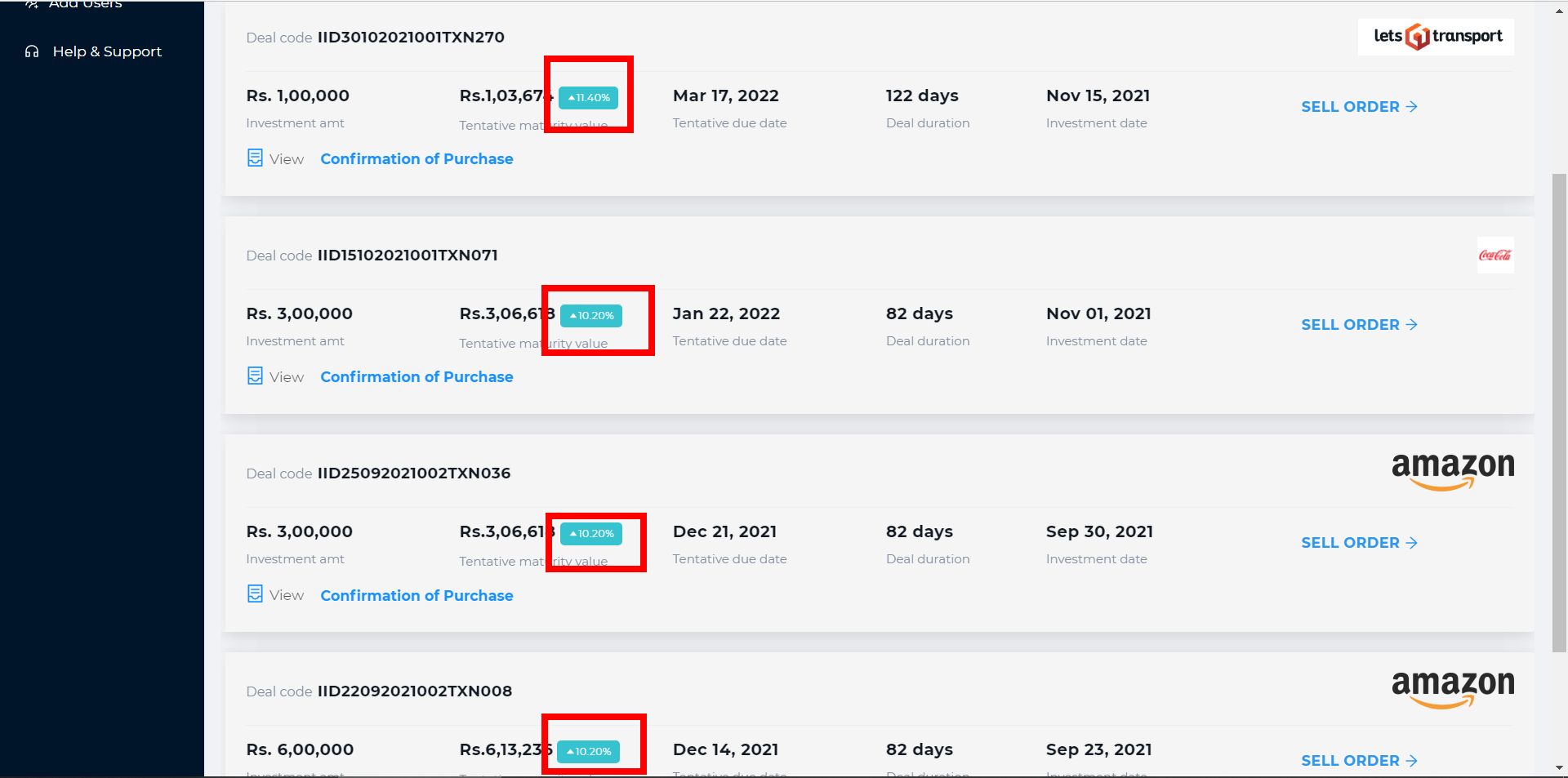

I’ve invested and they pay on time and have had zero defaults in 2 years since they started. Its an invoice discounting platform where your money is invested for 82 days and the invoices are payable by reputed companies like Coca Cola, Amazon to name a few. Since period is lower and companies are reputed, credit risk is close to zero. Trade cred pays out higher interest to the tune of 11.4% in case of vendors who are owed by lesser known companies. In case of ones like Amazon one gets paid 10.2%

Wint’s current offering is lending to UGrow Capital, which is also raising capital from Vivriti Short Term Bond Fund via senior secured bonds ( which is an Category II Alternative Investment Fund . i.e. a fund for Ultra HNI clients as min investment is 1 Cr. And I’m sure rich people do very thorough due diligence compared to us retail folk)

That being said the idea of SEBI keeping the ticket size to 1 Cr for such product is to make sure retail folk don’t invest as the inherent risk is much higher than other debt instruments.

The way I understand Invoice Discounting is, X who owns a shop might have supplied something to Amazon or via Amazon and he in return will get a Invoice with a commitment to receive payments from Amazon after 120 days. These invoices are then discounted with Banks who pay them and collect the money on the due date when Amazon pays. Generally credit risk is low as payments of invoices from these amazons are on time and hence banks are generally happy to discount these invoice and give cash to X immediately.

Amazon is not paying 10.2%. It is the X who holds the invoice will be paying the 10.2% as he needs the cash in advance.

I guess i should have worded the message more carefully. I wrote companies instead of vendor, I’ve corrected that line in the post above.

Yes the money which is due to the vendor ‘X’ is collected from the company (Amazon, Coca cola etc) by Tradecred and the rate of interest one gets paid at is 10.2%. This interest amount due at 10.2% is deducted by Tradecred in advance and the balance invoice amount is paid to the vendor who needs the money today hence is willing to part with the interest amount. Obviously the vendor doesn’t have good creditworthiness so he borrows from Tradecred instead of a bank.

Once the invoice amount is collected from the company, Tradecred pays the principal amount back to the investor along with the interest amount.

Main point being you get interest at 10.2% and since the money is payable by a reputed company its relatively safe, so i personally feel its safer than Wint. There are less well known companies where you get paid a higher interest rate of 11.4% to 11.6%

Its an individuals call whether he/she wants to invest based on their risk profile, i was merely offering an alternative.

Full Discosure: I am not affiliated in any manner with either Tradecred or Wint and get no kind of compensation monetary or otherwise for my post. Screenshot above is my personal investment.

I agree with you. As it is invoice discounting the tenor will be lower too

The risks are

It is assumed by investor that tradecred has done all the due deligence on the transaction and they have vetted the documents. It is assumed that the documents are genuine and X has shipped the goods to Amazon. There are instances when bogus invoice is raised without any goods being shipped or delivered and forged Amazon acceptance is also taken.

Also the money from Amazon is collected by Tradecredit and passed on to the investor. So the investor should do a due deligence on Tradecredit to repay the money. From the snapshot it appears that the ticket size is in lacks.

In case Amazon does not pay on the due date, the investor will lose the entire capital as he will not have any recourse until and unless Tradecred will file a case against Amazon. This is because the invoice I am sure will be payable to Tradecred.

I believe just like Wint, Tradecred is an enabler only.

Again, when you have a receivable from Amazon, why would anyone i.e X here would go to this site to discount the same when he can get the same done at any Commercial Bank. I do agree that getting limit sanctioned in commercial bank is a long process but I am sure If I get a Invoice from HUL, TCS or any such company, I will run and get it discounted and give a reduced rate.

Anyways this is something new I learnt today. Generally these products are offered by Commercial Bank under their Trade Finance Division.

@_satya - Thank you for posting this, learnt something new.

I am still unable to wrap my head around the very high-interest rate which is offered here. If I am willing to hold the instrument till maturity and provided the risk measures shown on the website are in place then this return is too hard to pass up.

It is indeed a risky investment, so invest a very small portion of your corpus in such investments and also diversify that across the different companies listed at Tradecred. I have only invested an amount I am comfortable losing in case of default.