From my research I found out below info regarding tax audit -

Info from income tax website - “ As per section 44AB, following persons are compulsorily required to get their accounts audited :

• A person carrying on business, if his total sales, turnover or gross receipts (as the case may be) in business for the year exceed or exceeds Rs. 1 crore. This provision is not applicable to the person, who opts for presumptive taxation scheme under section 44AD and his total sales or turnover doesn’t exceeds Rs. 2 crores.

Note: w.e.f. Assessment Year 2020-21, the threshold limit, for a person carrying on business, is increased from Rs. 1 Crore to Rs. 5 crore in case when cash receipt and payment made during the year does not exceed 5% of total receipt or payment, as the case may be. In other words, more than 95% of the business transactions should be done through banking channels.“

No where is it mentioned that you need to get an audit if your turn over is less than 1 Crore and if your income from salary is more than 2.5 lakhs.

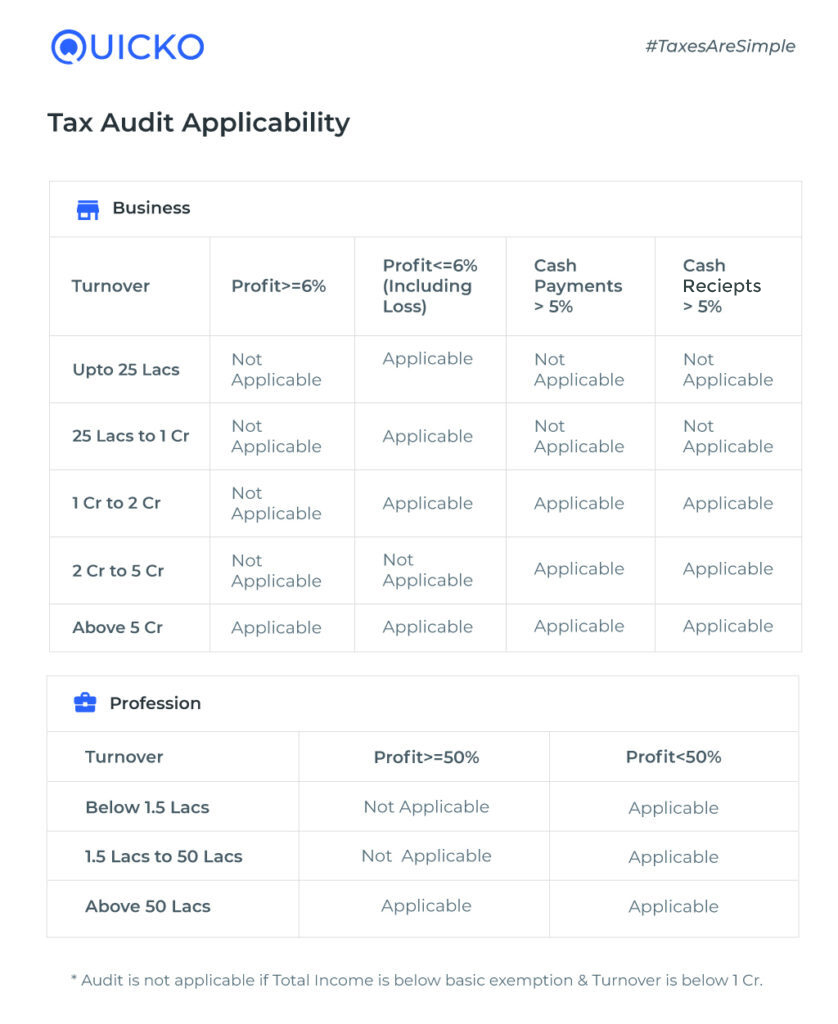

Now this is what Quicko says - “ * If the taxpayer has incurred loss or the profit is less than 6% or 8% of Turnover / Sales, and the Total Income is more than Basic Exemption Limit, Audit as per Sec 44AB(e) is applicable. The taxpayer should file ITR 3.”

This is what Section 44AB(e) states - “Each Person carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

get his accounts of such previous year audited by an accountant before the specified date.”

Section 44AD sub section 4 - “ Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1).”

But 44AD is all about presumptive taxation. So if this is the first time I am filing taxes for FnO category, I would have never used 44AD section at all. So, no need to get audited.

I think all of the new FnO traders are getting played.