you pay over 2% of your option premium as charges vs only 0.24% if you have good size.

i.e, you’re paying almost 10x of the charges if you trade 1 lot vs 36 lots

Even with free brokarge, you’ll be paying significantly higher with small size but it will help

(yeah, very unfair but that’s the way it is)

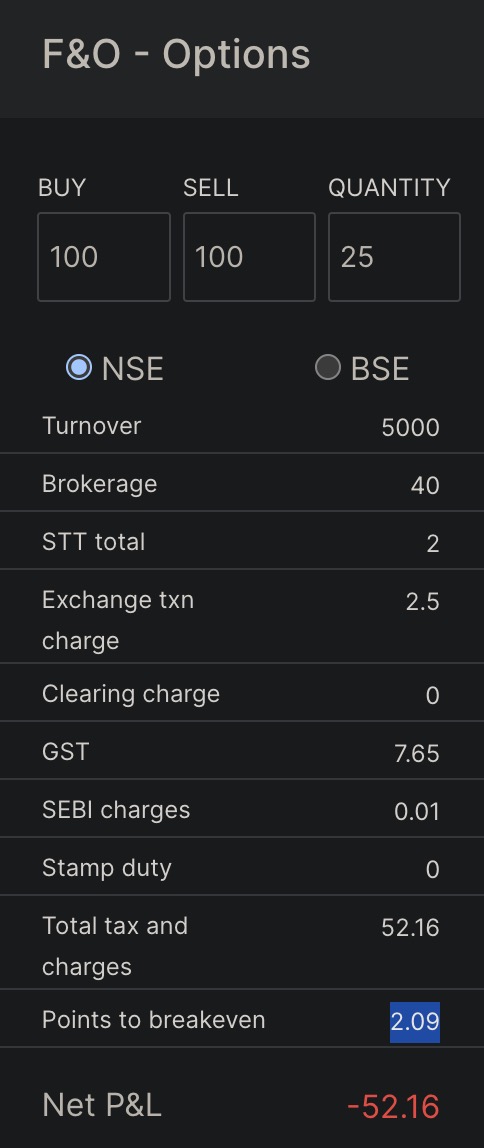

Ok. I am an option buyer. You have quoted the breakeven, and I am not sure how much it would come help for me , since I am a buyer.

What I saw is, I get 4.5 RS as STT and transaction charges for X25 quantities

And 146 stt and transaction charges for x900 quantities.

Does that mean , quantities have no advantage when it comes to lowering charges, when you are a buyer ?