Today on 23rd May 19, nifty 50 stocks were going record high, some by 3% some by 5%. But most of the call options of those very stocks were either falling badly or they were having a miniscule growth.

Can anyone elaborate why so? Why are people not interested in Options even though there is a full week left for monthly expiry and as expected election results?

After the exit polls, stocks and options were going parallel up or down. But today was just strange.

Anyone who trades options knows about this typical phenomenon. What you are seeking to understand is called volatility crush. Just search this term on YouTube and you will have plenty of videos explaining it.

Firstly to put things in perspective options are a different ball game altogether compared to futures and cash segments. Options have various advantages that a retail trader generally doesn’t understand, options are used by various hedge funds and traders.

(TIP - You want to learn about options refer this - LearnApp - Explore 250+ courses around trading & investing)

Let’s get down to your question -

In your case volatility plays a crucial role. There are other factors which include Delta, Theta(time) etc, but for our better understanding lets keep it constant.

(TIP-To understand volatility Volatility Basics – Varsity by Zerodha

In a nutshell volatility increases when there is an event around the corner.

Generally, the retail traders (option buyers both Call and Puts)will pay the premiums without considering valuations of Option strikes, which in turn increase the volatility and rewards the smart money ( options sellers).

( TIP -To know about options strikes refer the following -

Let me give an example -

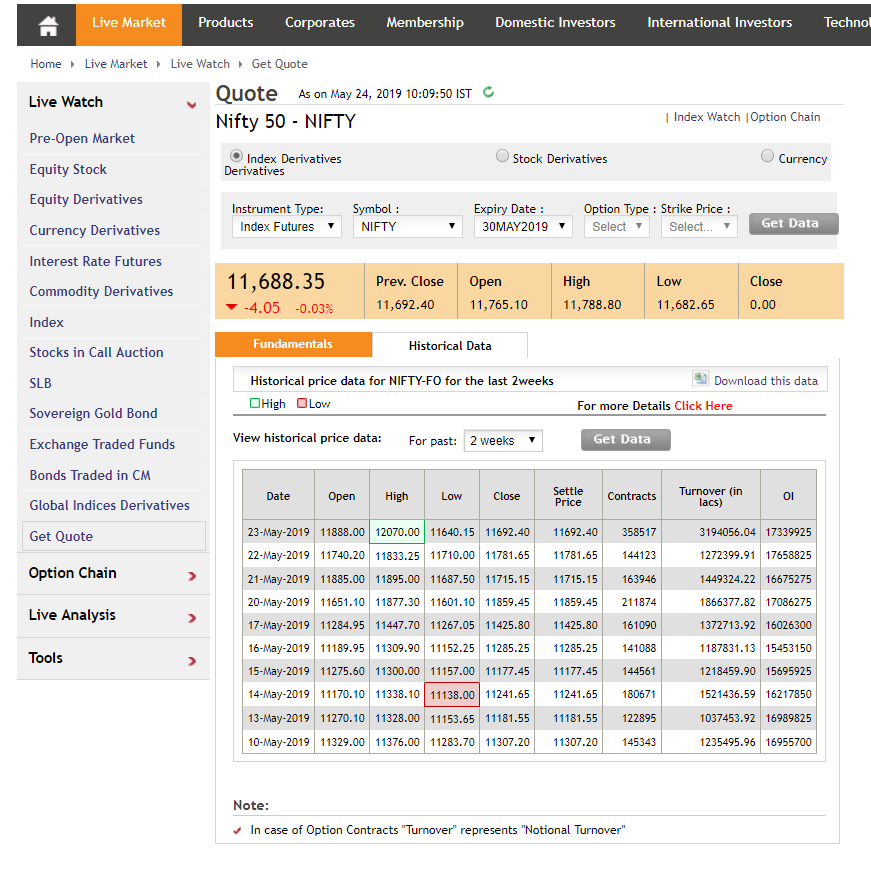

Nifty has historic volatility of around 18-20. (Data from NSE India)

3 days prior to exit polls volatility was in range in 60 to 70, a day prior to the election result volatility was in the range of 90. This clearly implies that volatility has been on the rise, specifically 4.5 times more than a normal day.

(TIP-To know volatility levels and various data facts which most people do not use refer this - https://sensibull.com/) )

Most of the traders were expecting an NDA government which in turn meant the market would gap up and hence options buyers would benefit.

On 23rd the start clearly suggested that an NDA had a clear momentum over its competitors, this ideally had to benefit the option buyers as the market had a gap up. Comes into picture volatility which took a nosedive, due to this drop the premiums also fell alongside, which ideally perplexed quite a few people but benefited the option sellers.

Even though the market was in favor of the call option buyers which ideally means that the option premiums increase as and when the markets go up but the blind spot was the volatility which was ignored by the buyers which in turn helped none other than the sellers. Another important factor to consider was that these premiums were pertaining to the weekly expiries.

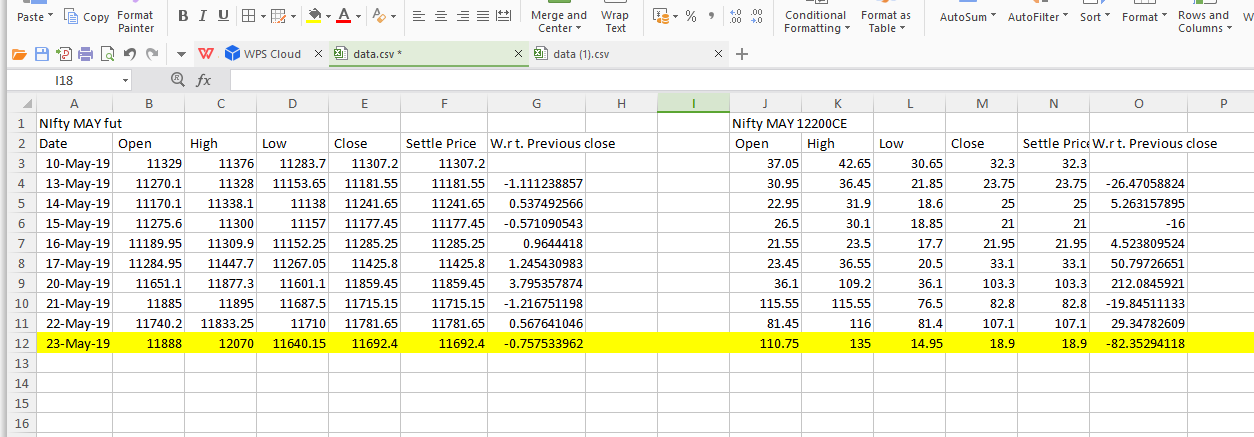

Now let’s do a comparative and behavior analysis with respective closing price movement between Nifty future and Nifty options

Now let us explain how Nifty strike 12200CE of 30th May expiry behaved in last 10 days with respect to Nifty MAY FUT

Now let’s do a comparative and behavior analysis with respective closing price movements between Nifty fut and Nifty options

Usual Behavior

On 13th May, negative 1.1% of future change proportional to negative 26% of options change

On 14th May, 0.5% of future change proportional to 5.2% of options change

On 15th May, negative 0.5% of future change proportional to negative 16% of options change

Prior to exit poll:

On 17th May, 1.2% of future change proportional to 50% of options change

Day after exit poll:

On 20th May, 3.7% of future change proportional to 212 % of options change

Unusual Behavior

On 21th May, negative 1.21% of future change proportional to negative 19% of options change

On 22nd May, 0.5% of future change proportional to 29% of options change

And on event day,

Let us explain the 23rd-day movement, Nifty had an up move initially of 2.5%, which means ideally premium should have spiked up at least 100% compared to the previous close, whereas premium moved only 19%.

On 23rd May, negative 0.75% of future change proportional to negative 82% of options change

In the image above the monthly option has been taken as the weekly option charts aren’t available.

Monthly options and weekly options can be correlated for analysis perse.

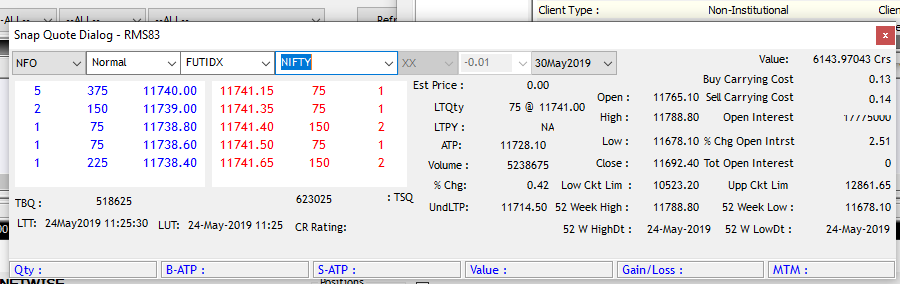

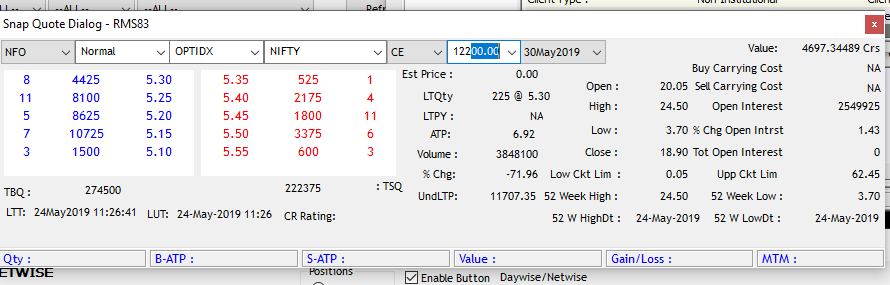

Next day of the event,

24th May, as of now(11:25 AM) 0.4% of future change proportional to negative 71% of options change, Please refer to the screen shot below.

Concluding all of this -

On any event-specific day, the smart money dumps their position and reap the reward, by doing so there will be a drastic fall in volatility.

The market did go up option buyers had to benefit, premiums had to increase long options had to make money but as the saying goes

Market does what smart money wants it to do.

So ask yourself do you want to be with the smart ones or against them.