There are a lot of perspectives to this passive vs active debate. I’ll try to briefly answer this to the best of my knowledge

The core idea behind passive investing is that markets price most of the information at any given point of time. John Bogle, the father of Index and founder of Vanguard investing puts this succinctly

The markets are highly efficient — although, importantly, not perfectly efficient. Sometimes they’re very efficient and sometimes they’re not. It’s hard for we poor souls on Earth to know which is which

This doesn’t mean that no one can outperform the market, but the number of people who can is very less. This put in real-world context means that you don’t know in advance who can beat the market. When you are investing in a mutual fund, you are essentially betting that the fund manager can beat the market and you have no way of knowing in advance whether he will be able to.

Now, you can either bet on the fund manager or follow the passive investing belief, that the market is supreme and invest in an index fund.

The advantage of an index fund is it offers a lot of benefits

- Total or extensive diversification

- Takes away individual stocks risk

- No emotions involved and hence no bias

- No fund manager risk

- Wide exposure major sectors and hence the chance to exploit growth across

- Most importantly low costs. I cannot stress this enough

Of course, the disadvantage is that you will be missing out on the chances of outperformance, but if you analyse funds, Indian ot otherwise, the alpha they are generating is consistently decreasing. Here are some data points

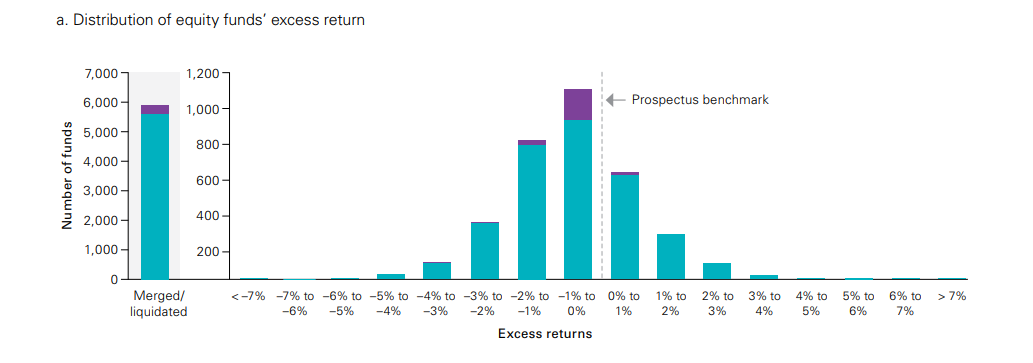

In the United States

As you can see that very few funds were able to beat their benchmarks.

Also, as markets develop the information asymmetry also decreases. This means that every fund manager will be privy to the same information and this edge will just fade away.

Check the return against the Total Returns and Index and you will see the outperformance if any reduces if not any altogether. Also, in India, our genius fund managers were all these years measuring performance vs the Index and not the total returns index. If you aren’t aware of the difference would suggest you read this post where Karthik has explained it beautifully. If you measure the returns vs the TRI index the resulting alpha substantially reduces and in case of some funds disappears altogether.

The question you should ask yourself is, should I pay a fund manager 2 to 2.5% just to deliver index-like returns when you could have achieved the same returns by investing in an index fund at a fraction of the cost (0.15% to 0.50%)

The second thing, is most fund managers in India are closet indexers or benchmark huggers. top 5 holdings of 53%. It also has one of the highest index weights in Nifty 50.

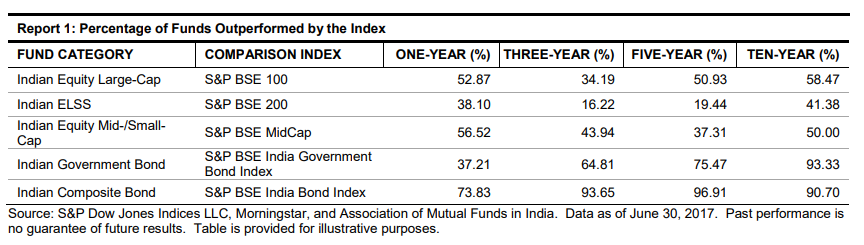

Quoting from the SPIVA report

Indian Large-Cap Equity Funds: Over the 1-, 3-, 5-, and 10-year periods ending in June 2017,

52.87%, 34.19%, 50.93%, and 58.47% of large-cap equity funds in India underperformed the S&P

BSE 100, respectively. Over the 10-year period studied, survivorship rate and style consistency

were low, at 66.1% and 28.81%, respectively. Over the same horizon, the asset-weighted fund

return was 79 bps higher than the equal-weighted fund return, and the return spread between the first and the third quartile break points of the fund performance was 3.11%.

Well, it’s easier said than done. Did you know that the funds you analyzed would beat the index 5 years ago? If yes, then please manage my money ![]()

One of the most prevalent biases in the market is the overconfidence bias, the belief that we know better and can hence perform better. Nothing could be farher from the truth.

It’s simple. Beating the market is hard and costly.

If you want to learn more about pasive investing and indexing.

- This episode of Freakonomics podcast is highly recommended - The Stupidest Thing You Can Do With Your Money.

- The case for low-cost index-fund investing - report by Vanguard

- Setting the record straight: Truths about indexing report by Vanguard