“Investing in mutual funds is subject to market risk, read scheme related documents carefully” is a disclaimer that investors receive when buying a particular mutual fund. This means that though mutual funds are regulated investment, the returns that an investor gets are not risk-free and are dependent on market conditions. Along with market risk, investing in mutual funds, comes with specific risks like any other investment,

Let’s understand the five key kinds of mutual fund risks that investor need to know while investing in mutual funds and what are the ways to overcome these risks:

Inflation Risk: During the current pandemic, enormous amounts of fiscal and monetary stimulus have fuelled inflation. Over the long term, companies try to cope with inflationary pressures by passing on the increase in input costs to consumers. This, in turn, erodes the purchasing power due to rising prices of goods and services. Inflation can also have a significant impact on the real or inflation adjusted return of an investor’s investments.

How to cope with inflation?

Traditional investments like Fixed Deposits have not kept pace with inflation. On the other hand, price of gold generally increases with the value of inflation because it is a dollar-denominated commodity. Gold prices have kept pace with inflation and returns from Equity-oriented mutual funds have the potential to outperform the rate of inflation. So, to cope with inflation, investors need to diversify their allocation into equity, gold and other asset classes.

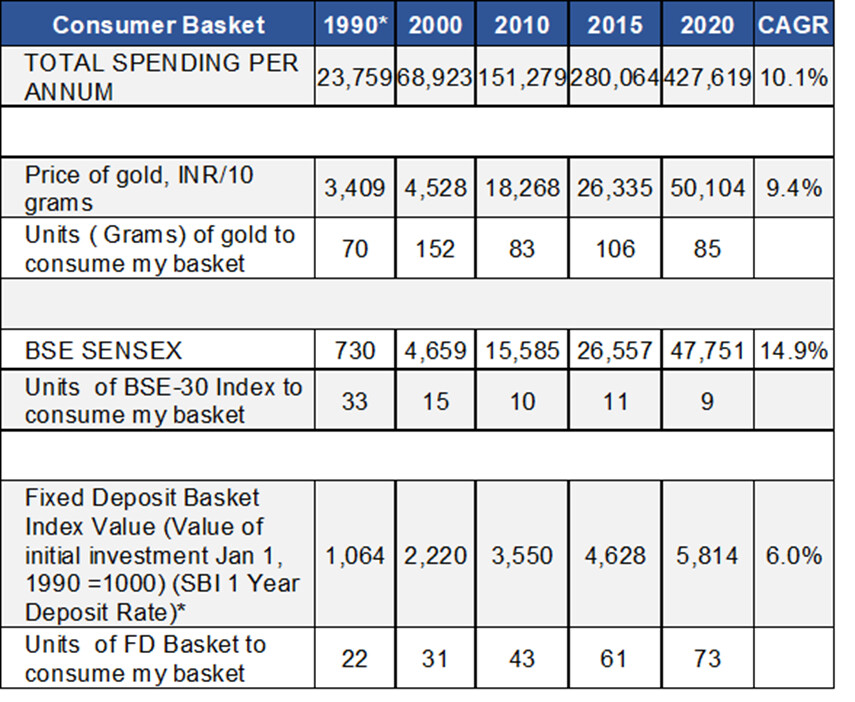

Illustration 1: Impact of inflation on the real return of your investment

Quarterly compounding and Tax rate on Fixed Deposit assumed to be 30%

Data as on December 2020.

Past performance may or may not be sustained in the future

2. Interest rate risk:

One factor which correlates with inflation is the interest rates. The rise in inflation rates could typically push up interest rates and vice versa. Accordingly, in Fixed Income, returns can change depending on the movement of interest rates. Interest rates inversely impact Debt funds. If interest rates go up, yields of instruments in a portfolio will go down, leading to a fall in net asset values (NAVs) and hence the returns. On the other hand, NAVs will go up if interest rates fall. The value of equity funds could also be impacted in the short term due to interest rate changes.

How to cope with interest rate risk?

The way to avoid interest rate volatility in fixed income investors should choose debt funds with lower maturity as usually, longer the maturity, greater the degree of price volatility.

3. Liquidity risk

Liquidity risk refers to the inability to liquidate an asset at the desired price. For example Fund manager is unable to sell the debt paper due to non-availability of buyer. Liquidity risk could occur due to various reasons, including demand and supply conditions, an increase in interest rates, change in the credit rating of the underlying instrument, and so on.

How to cope with liquidity risk?

One way to overcome liquidity risk could be to diversify across asset classes and invest in funds with liquid underlying instruments.

4. Credit risk

Credit risk refers to the risk of default on payment by the issuer. Bonds are given ratings by SEBI registered Credit Rating Agencies.

How to overcome credit risk?

Investors can select debt funds with low credit risk that comprise of high-quality instruments such as government securities or AAA rated PSU bonds that are generally reckoned to be safe and have low credit risk.

Investors need to look at its credit rating before they invest in a debt fund.

5. Concentration risk

This means the underlying portfolio has too much exposure to a particular instrument or securities and fails to diversify.

How to overcome concentration risk:

To manage fund level concentration risk, financial experts recommend that investors should diversify their portfolios. Similarly, investors need to diversify their debt fund investment as per maturity and issuer to overcome the risk of concentration.

Investors can also resort to prudent asset allocation strategy to diversify their portfolio across equity, debt and gold assets. Alternatively, they can invest in a multi asset fund of funds where the fund manager balances across equity, debt and gold assets to lower the risk of downside arising from allocation to a single asset class.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.