Now I think this is the best time to tell about this collapse.

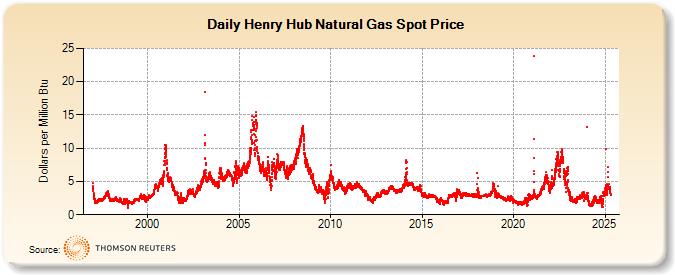

Natural gas movement in this week.

The text below is generated by ChatGPT

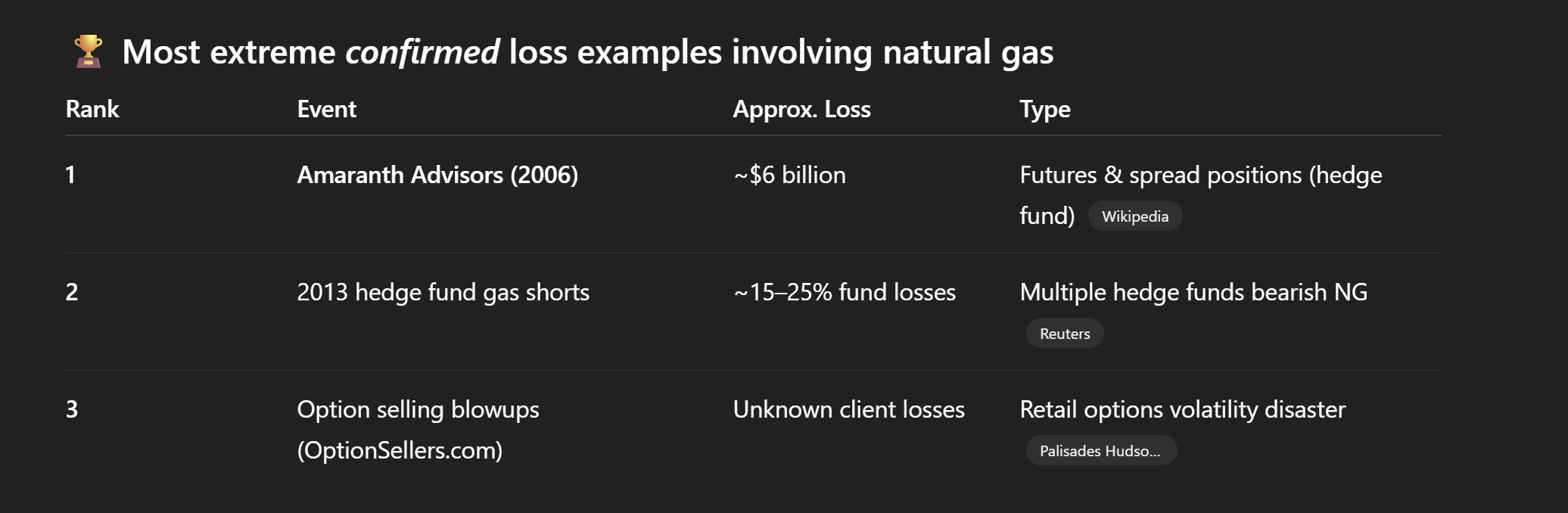

The largest known single speculative loss in natural gas history is Amaranth (~$6 billion) in 2006 — across both futures and options spread positions. This dwarf’s the typical cyclical losses traders see in a volatile gas market, because that blow-up combined huge leverage with concentration and liquidity fragility.

Alright — this one is the canonical case. I’ll keep it tight, factual, and technical.

Amaranth Advisors (2006): what actually went wrong

The core trade (not just “short gas”)

The core trade (not just “short gas”)

Amaranth wasn’t simply short outright gas.

They ran massive calendar spread trades in NYMEX natural gas futures.

Main position:

- Long: Winter contracts (Nov–Mar)

- Short: Summer contracts (Apr–Oct)

Thesis (reasonable on paper):

- Winter demand is volatile (weather risk)

- Summer demand is stable

- Therefore winter–summer spread should widen as winter approaches

This trade had worked for years.

The scale (this is where it turns lethal)

The scale (this is where it turns lethal)

By mid-2006:

- Amaranth controlled 30–40% of open interest in some NG contracts

- Notional exposure ran into hundreds of billions USD

- Fund AUM ≈ $9–10bn

- Effective leverage on some legs: 20–30×

At that size:

- You are no longer trading the market

- You are the market

What broke the model

What broke the model

Three things hit simultaneously:

(a) Weather regime shift

- Summer 2006 was mild

- Hurricane season (Katrina-style repeat) did not materialise

- Storage levels stayed comfortable

![]() Winter risk premium collapsed instead of expanding

Winter risk premium collapsed instead of expanding

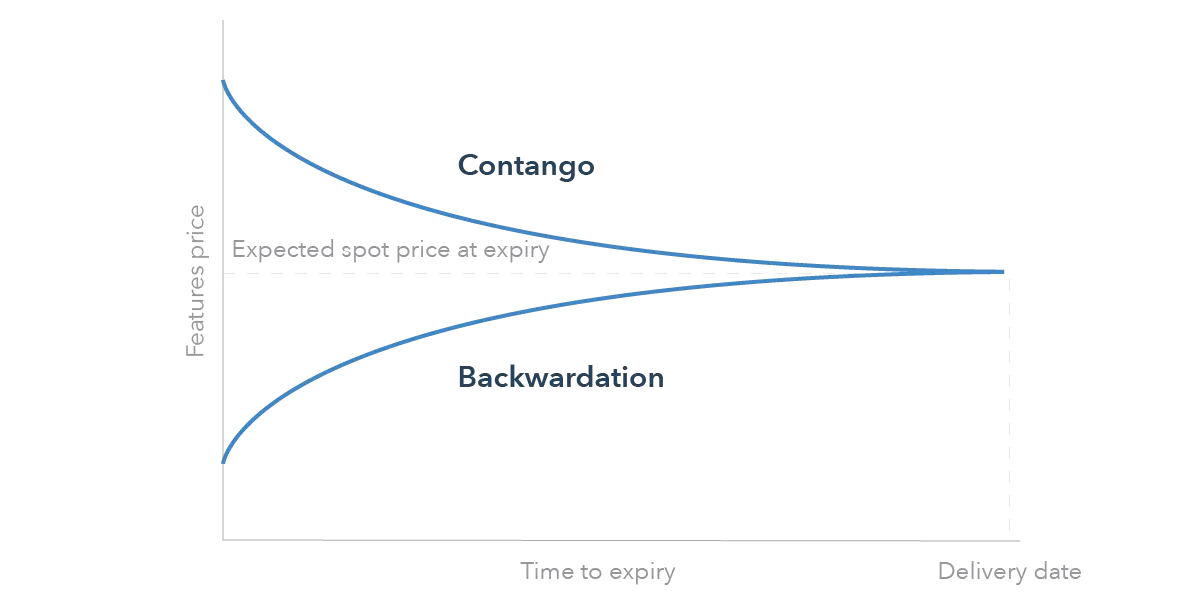

(b) Curve behaviour flipped

- Winter–summer spreads compressed sharply

- Losses came from spread convergence, not just outright price moves

(important — many people miss this)

(c) Liquidity illusion

- Spreads look liquid

- They aren’t when one fund owns the book

As prices moved:

- Margin calls rose daily

- Forced liquidation pushed spreads further against them

- Feedback loop kicked in

Why losses exploded non-linearly (key insight)

Why losses exploded non-linearly (key insight)

Calendar spreads feel “safer” than outright futures — but:

- Margin is charged on both legs

- Correlation assumptions broke under stress

- Volatility rose → margin requirements jumped

- Exit liquidity vanished

So P&L looked roughly like:

small move → manageable loss

medium move → large loss

forced unwind → catastrophic convex loss

This is exactly how short-vol structures fail.

The numbers (what we know publicly)

The numbers (what we know publicly)

- ~$6 billion lost in weeks

- ~65% of fund wiped

- Positions transferred to JPMorgan & Citadel at fire-sale terms

- Fund effectively shut down

Trader often cited:

Brian Hunter (not solely responsible, but central to the strategy)

Why natural gas is uniquely dangerous

Why natural gas is uniquely dangerous

Natural gas combines:

- Extreme weather convexity

- Non-storable short-term supply

- Violent seasonality

- Thin liquidity in spreads under stress

That’s why gas earned the nickname “widow-maker”.

The big lesson (still relevant in 2026)

The big lesson (still relevant in 2026)

Amaranth did not die because:

- “Gas went up”

- “They were stupid”

They died because:

They mistook historical stability for structural safety

In derivatives terms:

- They were short tail risk

- With size

- In a market where tails arrive via weather

Why this still matters today

Why this still matters today

Every modern gas squeeze (including recent ones) echoes this pattern:

- Large speculative net shorts

- Weather shock

- Liquidity evaporates

- Forced covering accelerates price

Different players, same physics.