Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Why is the Taiwan Dollar going wild?

- The taxman is after Samsung

Why is the Taiwan Dollar going wild?

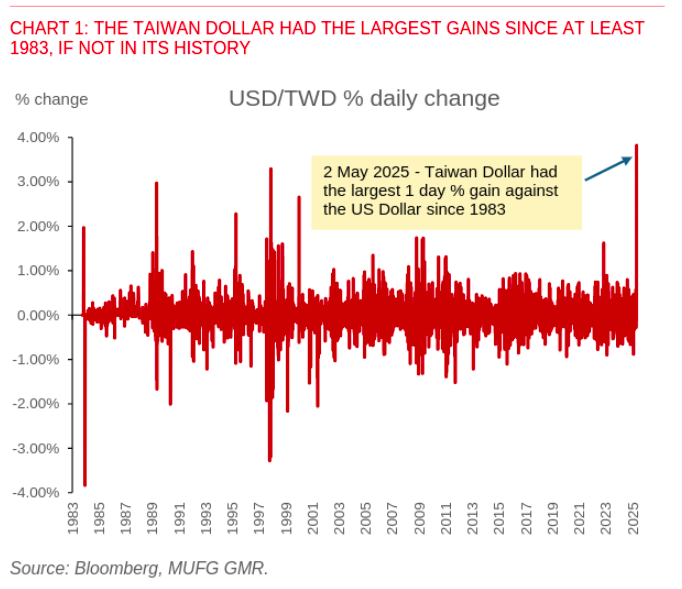

The Taiwanese dollar (TWD) did something in the past few days it has not done since the late-1980s: it jumped more than 6% against the U.S. dollar.

For a currency that normally wiggles by a few tenths of a per cent each day, that is quite literally a once-in-a-generation leap.

But before we get into why this happened, and everything you should know around it, let’s give you a quick explainer on how currencies move.

When one says the Taiwanese dollar “appreciated,” it means it became stronger relative to other currencies, usually the US dollar (USD). So, for example, if it took 33 TWD to buy 1 USD last week, and that now only takes 30 TWD, the TWD has strengthened (appreciated) over the last week. Conversely, the USD has ‘depreciated’ relative to the TWD.

These movements matter a lot. A stronger currency can make a country’s exports more expensive and imports cheaper. It also affects all sorts of other money decisions — like financial flows, investment returns, and hedging strategies.

Taiwan’s glaring USD exposure

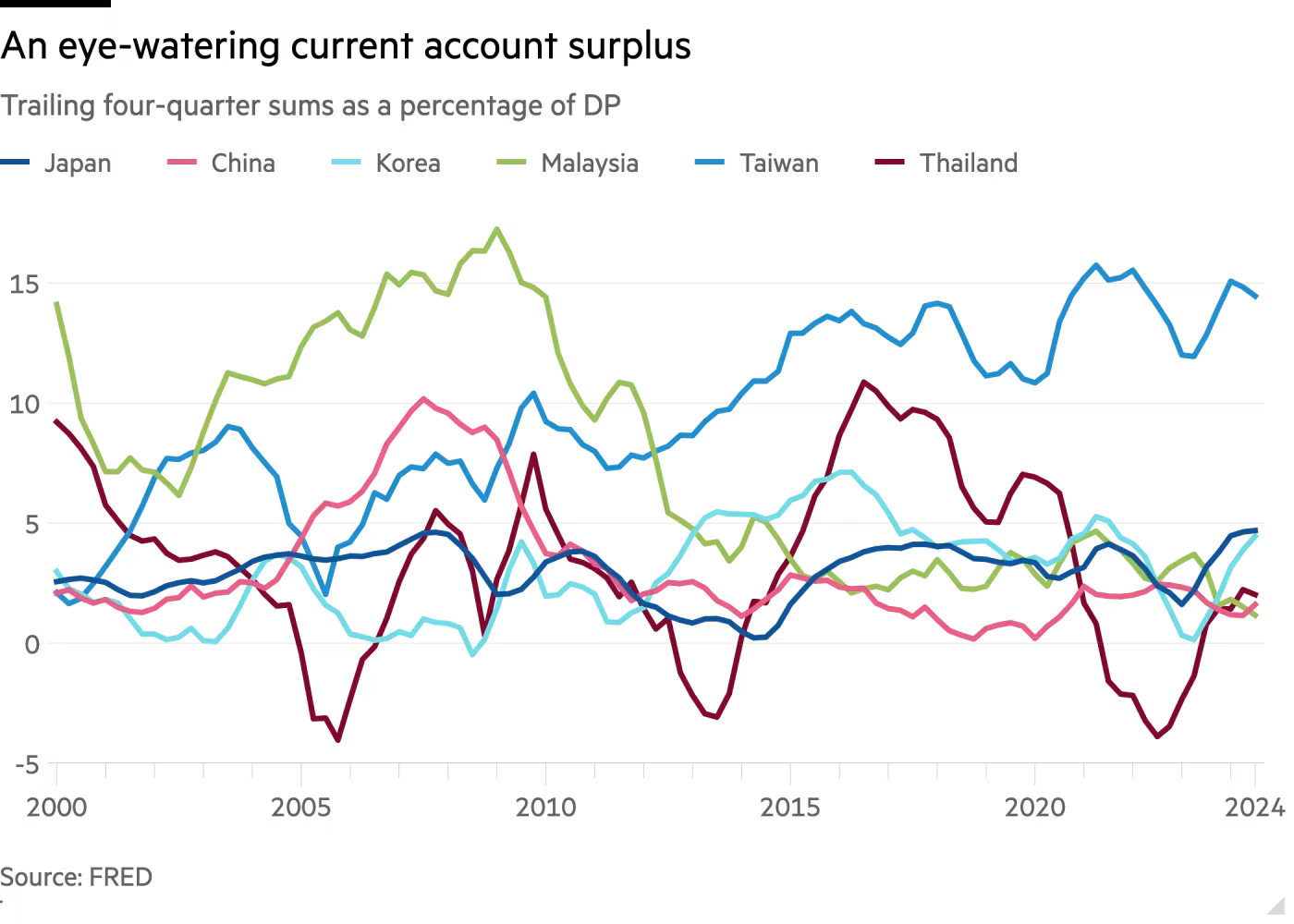

To understand this, we need to look at Taiwan’s current account surplus , which has been unusually large for many years—at times over 10% of GDP.

That’s massive .

Taiwan essentially constantly exports far more than it imports, especially in high-value sectors like semiconductors and electronics. This surplus means that the country is constantly accumulating foreign currencies like the USD.

But there’s a twist: unlike countries that recycle these dollars into their central bank reserves — something we do in India as well — Taiwan does something unusual. Much of this surplus foreign exchange has been channelled through its enormous life insurance sector.

Confused?

See, Taiwanese life insurers are global financial powerhouses. They manage nearly $1 trillion in assets. But here’s the problem: Taiwan’s domestic capital markets are too small to absorb that much money. Its domestic bond market is tiny, the stock market is not nearly diverse enough, and local real estate is already expensive. Then where do insurers park their money?

Well, they pour these savings abroad, mainly into US dollar-denominated bonds: treasuries, corporate bonds, and “Formosa bonds” (US dollar bonds issued in Taiwan, often by foreign issuers).

A huge chunk of Taiwan’s economy is tied up in this. According to the Financial Times, foreign investments by insurers add up to more than 60% of Taiwan’s GDP. This is why the USD-TWD exchange rate is so systemically important to the country.

Taiwanese insurers are basically sitting on a horrible currency mismatch.

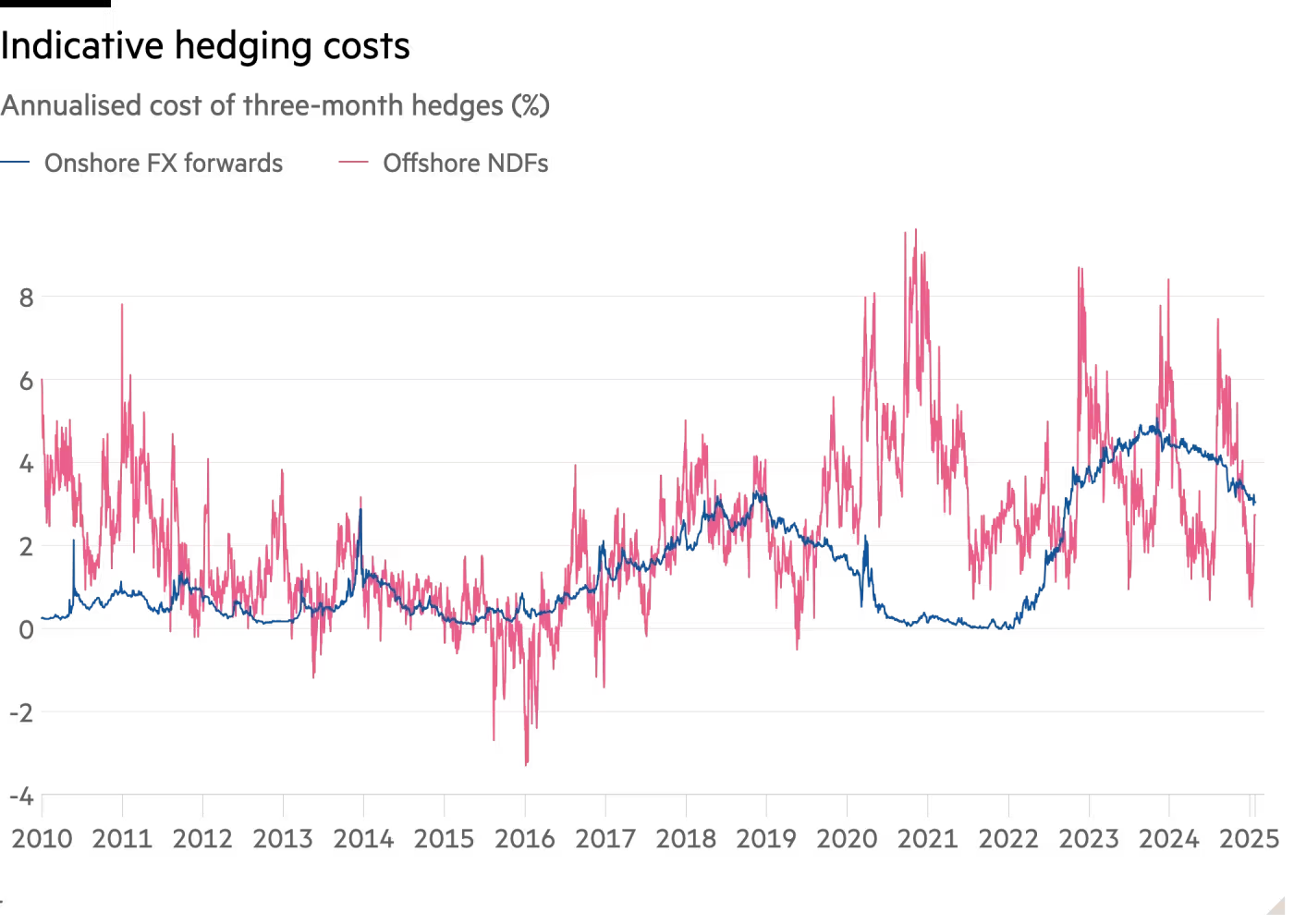

They sell policies in Taiwan dollars, but invest in USD-denominated assets. This creates a ‘currency risk’ — if the TWD strengthens too quickly against the Dollar, the returns from their dollar investments could suddenly disappear. To protect themselves from such a possibility, they hedge their Dollar exposure using foreign exchange derivatives like FX swaps and forwards, locking in preferred exchange rates.

Why the Taiwanese Dollar is shooting upwards

That brings us to the first set of reasons behind the Taiwanese dollar’s recent surge.

In early May 2025, the US dollar weakened globally. We all know why. At the same time, reports suggested that Taiwan’s government might allow its currency to strengthen as part of ongoing trade negotiations with the US.

This speculation triggered a wave of reactions.

Exporters, who earn much of their revenue in US dollars, rushed to convert those dollars back into TWD, worried that their dollar earnings would soon be worth less in local terms. Consider the stakes here for a company like TSMC. Most of its operations are in Taiwan, while a large chunk of its sales are usually made in dollars. A stronger currency directly erodes the value of its US dollar–denominated revenue**.** In fact, every one percentage point of appreciation in the Taiwanese dollar cuts its operating margin by about 0.4 percentage points, according to estimates by Counterpoint Research.

Meanwhile, insurers, sitting on vast US dollar portfolios, ramped up their hedging activity to protect themselves against these currency swings.

Essentially, major Taiwanese businesses of all sorts were scrambling for Taiwanese Dollars to protect their own finances. This sparked a big surge in demand for TWD, causing its value to rise sharply.

This whole problem was compounded by thin market liquidity. The Taiwanese foreign exchange market isn’t as deep or liquid as the big global markets like the euro or yen. When many players rush in at once — whether exporters, insurers, or speculators — they can’t find counterparties for their trades easily. Price moves can quickly become exaggerated.

That’s what we saw. Without enough market depth, the rush for TWD became a rout.

Adding to this were two other factors fuelling the TWD’s rise:

- One, in the background, a broader regional shift was underway. Across Asia, central banks and financial institutions have gradually been reducing their US dollar exposure — partly because of global trade tensions, and partly out of concern for the Dollar’s longer-term trajectory.

- Two, Taiwan’s central bank appeared to step back. Historically, it has actively intervened in forex markets to prevent the TWD from appreciating, so that Taiwan’s exports remain competitive. But this time around, it was noticeably absent. That hands-off stance fueled market speculation that the authorities were ready to tolerate a stronger TWD, maybe to boost Taiwan’s bargaining position in trade talks with the US.

A deeper background

But beyond this, it’s worth looking at the deeper, structural backdrop — courtesy of a fantastic paper by Brad Setser, a Senior fellow at the Council for Foreign Relations.

Until around 2020, Taiwan didn’t disclose how much it was intervening in the currency market, especially in derivative markets. Setser’s paper, “Shadow FX Intervention in Taiwan,” showed that its central bank was secretly one of the world’s biggest FX derivatives players. It ran exposures as large as $130 billion (about 20% of Taiwan’s GDP at the time) on these trades. Essentially, Taiwan’s central bank was using swaps and forwards with local banks and insurers to absorb dollar inflows and prevent the currency from appreciating.

Why all this hidden intervention?

Taiwan’s life insurers were shovelling massive amounts of money into overseas US dollar assets — we’re talking hundreds of billions of dollars. On paper, these insurers promised payouts in Taiwanese dollars to local policyholders. But as we mentioned before, their currency mismatch was a crucial risk: one large forex move could ruin their entire business.

To manage this, the insurers had to hedge: they needed to lock in the future USD-TWD exchange rate, so that a rising TWD wouldn’t crush the value of their USD assets.

But that created its own problem: the size of the hedging demand was so enormous that it would have swamped Taiwan’s onshore derivatives market, driving up the value of the TWD. And because Taiwan depends so much on exports, that was precisely what the central bank wanted to avoid. So the central bank itself quietly stepped in as the counterparty to Taiwanese insurers, effectively absorbing the hedging flows through foreign exchange swaps and forwards.

But crucially, it didn’t report this activity in its official reserves.

And it didn’t have to. After all, it was uniquely shielded from the International Monetary Fund’s (IMF) disclosure requirements.

See, the IMF has guidelines — backed by increasing global pressure — around what counts as “foreign exchange intervention” and the disclosures a country’s central bank is expected to make. Typically, countries on the IMF’s Special Data Dissemination Standard (SDDS) are required to report detailed reserve data, including forward and derivative positions.

But here’s the catch: Taiwan wasn’t signed up to the SDDS at all . After all, most countries in the world don’t even recognise Taiwan’s existence, because of its history with China. It couldn’t conceivably become a member of the IMF.

But that very fact also gave the Taiwanese central bank a legal loophole.

Because it wasn’t bound by the same reporting standards as other countries, Taiwan wasn’t technically required to disclose its derivative positions or forward book. So even though it was carrying out massive interventions in the FX market, it didn’t have to show these activities in its official reserves. This allowed it to by-pass international scrutiny.

This mattered enormously. If Taiwan had included those derivative positions in its formal reserves, its reserve pile would have looked outsized relative to the size of its economy, instantly drawing attention from international monitoring systems and setting off alarms in places like Washington. Under US trade policy, if a country runs a large current account surplus and shows evidence of persistent, one-sided currency intervention to hold down its exchange rate, it risks being labeled a “currency manipulator” by the US Treasury. But Taiwan’s weird, twilight status as a non-country gave it a workaround.

By intervening quietly through derivatives and by staying off the list of countries that had committed to full disclosure, it avoided bloating its reported reserves and remained below the radar of both IMF surveillance and the US Treasury’s currency watchlist.

Brad Setser’s work was critical in exposing this. His paper highlighted that Taiwan was one of the very few major surplus countries where official reserves dramatically understated the true scale of FX intervention. Once his research became widespread and external pressure mounted, Taiwan began disclosing its forward positions starting around 2020. The world finally got a clear look at just how deeply involved its central bank had been in managing the currency behind the scenes.

When the Fed hiked rates towards the end of COVID, the USD became relatively expensive. Hedging costs soared — sometimes hitting 5% a year. Insurers pulled back on some hedges. The central bank scaled down some of its interventions, letting more market forces come through.

Fast forward to today, and you get the perfect storm.

A structurally strong currency because of the current account surplus, insurers rebalancing their hedges, exporters dumping dollars, a broader regional retreat from the USD, thin liquidity amplifying every move, and a central bank sitting on the sidelines.

And that’s how you get a 6%+ surge in just 2 days.

The taxman is after Samsung

Samsung, one of the world’s largest electronics brands, is currently caught in a serious legal and financial battle with Indian authorities.

At its heart, the dispute is about how a certain part was classified in Samsung’s import paperwork. But don’t dismiss it as being unimportant; the sheer scale of the dispute makes it something worth taking note of. The Indian government has asked Samsung India and its officials to pay a total of $601 million in taxes and penalties. That’s around ₹5,000 crore. To put that in perspective, that’s more than 60% of everything Samsung India earned in profits last year.

Clearly, this is not something to ignore. So let’s talk about it.

What is this about?

This dispute is all about taxes. More specifically, it’s about how Samsung classified a certain type of telecom equipment — something called a ‘Remote Radio Head’, or RRH — when it brought them into India between 2018 and 2021. These RRHs are essential components used in telecom towers. Samsung imported $784 million worth of these RRHs from its factories in Korea and Vietnam, and supplied them to Reliance Jio, which was then in the middle of rapidly expanding its 4G network.

Now, when companies import goods into India, they have to pay ‘customs duties’. These, much like the tariffs that Trump has made so famous, are basically a tax for bringing things into the country. But how much duty a company pays depends entirely on how the item is classified.

That’s what makes tax policy so complex — if you want to know how much tax you have to pay for imports, you have to go through this ~900 page file, and try and figure which among its nearly 12,000 items your imported product resembles most closely.

As a thumb rule, though, the Indian government is a lot more forgiving if you’re importing components than completed goods. When it comes to the kind of telecom equipment Samsung dealt with, a complete machine attracts a 10-20% duty. If you say it’s just a ‘part’ of a machine, the duty could be much lower — sometimes even zero.

This is where the entire fight lies.

Samsung calls its imported RRH units as “parts” of a telecom system — not full-blown transceivers or communication devices. And so, it paid little to no customs duty on them. But the Indian customs department doesn’t agree with their characterisation. They say these RRH units aren’t just parts, they’re actually complete transmission and reception devices, which means they should’ve attracted a much higher import tax.

The Customs department thinks Samsung misclassified these items on purpose to save money, avoiding taxes. The department also alleges that Samsung’s paperwork for its imports are “false documents” that it tried to dupe the government with. And for all this, it slapped a demand of around $520 million on the company — for the unpaid tax money, combined with a 100% penalty. On top of that, they’ve also slapped an additional $81 million in penalties on seven senior employees of Samsung India, accusing them of scheming to wilfully avoid the duty.

Samsung, of course, isn’t happy. It has gone to the Customs, Excise, and Service Tax Appellate Tribunal, or CESTAT, asking it to quash the order. Essentially, it wants the customs department to legally be told to back off.

To really understand what’s happening, though, you need to get to the heart of the technical disagreement here — what exactly is a Remote Radio Head?

(Hint: it isn’t an amazing art rock band.)

Pictured: Not Remote Radio Head.

Think of how mobile towers work. These towers aren’t just tall poles. They have all kinds of electronic equipment mounted on them, which constantly talk to your devices. The RRH is one such piece of equipment. It sits close to the antenna, usually on top of the tower. Its job is to take digital signals from another device — the ‘Base Band Unit’, or BBU — convert them into radio signals, and then transmit them to your phone. And when your phone sends signals back, the RRH captures them, cleans them up, and sends them back to the BBU for further processing.

So in a way, the RRH both transmits and receives signals. Technically, it contains both a transmitter and a receiver, the two things that make a “transceiver”.

That’s the crux of the customs department’s argument. They say, if something sends and receives signals, it’s a ‘transceiver’. And a ‘transceiver’, to the department, is a complete, stand-alone communications device, which should be taxed accordingly. They even found internal documents from Samsung, dating back to 2020, where Samsung reportedly described the RRH as a ‘transceiver’ in letters sent to Indian government departments. That, according to Customs, is proof that Samsung knew what the device was all along, and still tried to classify it in a way that avoided taxes.

Samsung disagrees. They claim the RRH alone cannot function like a proper transceiver. It needs to be connected to the BBU to actually do anything useful. Without the BBU, the RRH can’t talk to the network, can’t process data, and can’t function independently. It’s just a high-tech component, not a complete machine. And therefore, it should be classified as a ‘part’ of the system, not a full transceiver.

That should tell you how murky it all is. Should a single module used in telephone towers be seen as a standalone device? Or should it be seen as a component of something larger, given how you can’t use it by itself? That’s the 600-million-dollar question.

Samsung’s defence becomes more complex when you look at the role of Reliance Jio.

From 2014 to 2017, before Samsung started supplying these RRHs to Jio, Reliance Jio was importing similar equipment in its own name, and it was classifying them in the exact same way. According to Samsung, customs didn’t raise any red flags back then. And if the department had knowingly let things go for so many years, it had essentially established a precedent that the industry had come to rely on. It couldn’t just change its approach on a whim.

In 2017, supposedly, customs authorities reportedly warned Reliance Jio that this classification might not be correct anymore. But Samsung says they only learnt of this recently, during the Customs department’s investigations. That warning had never been conveyed to them before — neither by Jio, nor by customs.

So now Samsung is saying, how can we be accused of misclassifying something if we were just following industry practice, which the Customs Department itself signed off on?

Sounds fair? No? Yes? maybe?

There’s also another point to consider here — the personal penalties. It’s not very common for Indian authorities to penalise individual employees of global companies to this extent. But in this case, customs has directly named and fined seven Samsung India executives. That’s a strong signal. It tells other multinational companies that personal accountability is now on the table: that if they do business in India, that could come at a personal cost.

This could change how companies think about compliance and internal controls, especially when it comes to import-related decisions.

Not the only one

Samsung isn’t the only multinational giant that’s caught up in tax troubles with our government. Consider a few other recent cases:

- Volkswagen, the carmaker, is currently facing a $1.4 billion customs demand in India over how they classified car kits imported over several years. Instead of importing cars into India, Volkswagen imported car parts in the form of ‘Completely Knocked Down’ kits — which would be assembled in an Indian unit. The customs department thinks Volkswagen was importing cars in all but name, and should be taxed accordingly.

- Kia Motors, too, ran into a similar problem. The customs department alleged that Kia tried to dodge a $155 million tax bill in how it imported parts for its ‘Carnival’ line of cars.

- French spirits giant Pernod Ricard received a $244 million customs demand in 2022, alleging that it tried to dodge customs duties while sourcing the liquor concentrates it used to make its beverages.

From Cairn Energy to BYD to Vodafone, many international companies have found themselves embroiled in horrible tax disputes with Indian authorities. The underlying issues are often similar; the way something is classified on paper can completely change the taxes a company has to pay. And the interpretation of these rules can swing both ways.

A fine line

So why does all this matter? To us, there are three takeaways here:

One: Aggressive policy can scare away foreign businesses

Companies like Samsung are big, global giants that have invested heavily in India. And they’re now being asked to pay hundreds of millions of dollars over how a few items were described on an import form. Now, we aren’t tax experts — we can’t tell you if these demands are fair or not. But as a policy move that hits foreign businesses, the optics around these cases is important.

The government, of course, intends to protect its revenue and make sure that its tax rules are followed. These are both legitimate goals. If they don’t act on classification issues now, it could create a culture where companies try to get away by bending the rules.

But there’s a fine line that the government must toe. If it’s too aggressive, it could scare off genuine investors. Overdo your tax policy, and many multinational companies might consider you an unpredictable market, where businesses have to constantly look out for shocks from the government. If the rules are open to different interpretations, and if past practices suddenly become liabilities, planning future investments can seem difficult.

Two: Different parts of the government can contradict each other

This also raises questions about whether the government is aligned internally on their different policies.

On one hand, the Indian government is running programmes like ‘Digital India’ and offering incentives for companies to Make in India — wooing companies like Samsung and Volkswagen to bring their supply chains here and build locally. At the same time, customs authorities keep applying high duties on critical imported parts.

In a sense, different Ministries might be working against each other — frustrating each other’s goals.

Three: Complex trade barriers cause confusion

In this newsletter, we’ve often mentioned tariffs, and how confusing can be for businesses. We’ve also talked about how the world criticises India for having overly restrictive tariff policies.

This is what we mean by that. When you have high tariffs, you change the incentives for everyone. Businesses constantly waste time trying to structure their operations around your tax laws, while authorities spend time and resources chasing them. And between them, they create a mass of confusion — all of which hurts business sentiment. Think about it: without import taxes, who in their right minds would ask if RRHs are standalone components, separate from BBUs? The problem isn’t just one of paying more money, but all the other problems that come with it.

Right now, the case is with the tribunal. It might get resolved there. Or it might wind its way through the legal system over the next many years. But no matter what the final decision is, the implications will go far beyond just Samsung. It will set the tone for how India handles complex, high-stakes classification disputes in the future.

For now, this case is a reminder that in a world of rapidly evolving technology, even a small change in how something is described on paper can trigger a multi-crore legal battle. And in India’s push to become a global business hub, the fine print is becoming just as important as the big picture.

Tidbits

Rural Demand Drives 11% Growth in India’s FMCG Sector

Source: Reuters

India’s consumer goods sector posted an 11% value growth in the March quarter, with rural markets outperforming urban regions for the fifth straight quarter, according to NielsenIQ. Rural areas, contributing over a third of total sales, recorded volume growth of 8.4%, down slightly from 9.2% in the previous quarter, while urban volume growth slowed to 2.6% from 4.2%. Price hikes, such as a 5.6% increase in edible oil, further lifted overall value. Smaller players led the gains, reporting 17.8% value growth, surpassing the broader FMCG market. Marico beat profit estimates, helped by stronger rural demand and higher packaged oil prices, and plans to expand in villages. In contrast, Hindustan Unilever and Nestlé India reported weaker profits, with HUL trimming its margin forecast amid high input costs and sluggish urban sales. NielsenIQ noted that revised tax slabs and an expected favorable monsoon could support further consumption growth in coming quarters.

Godrej Consumer Eyes ₹700 Crore Capex, Bets on Demand Revival

Source: Business Line

Godrej Consumer Products Ltd (GCPL) has announced a ₹700 crore capex over the next two years to expand its new factories in South and North India and set up a new facility in Indonesia. The company reported a ₹411 crore profit in Q4 with a 6.26% rise in revenue, though its consolidated EBITDA margin was hit by a more than 50% surge in palm oil prices, prompting a 15–16% calibrated price hike. GCPL expects double-digit EBITDA growth, mid-to-high single-digit volume growth in its standalone India business, and high single-digit consolidated revenue growth. The company remains optimistic about domestic demand recovery over the next 12–18 months, citing factors like cooling food inflation, income tax cuts, government welfare schemes, and an upcoming pay commission hike. Quick commerce has also seen exponential growth for GCPL, particularly in mid-size packs that deliver the highest margins. CEO Sudhir Sitapati highlighted that several production lines are yet to be added at the new domestic factories, which will be part of the planned investment.

MRF Q4 Net Profit Jumps 29%, Declares ₹235 Dividend

Source: Business Line

Tyre major MRF reported a 29% rise in consolidated net profit for Q4 FY25 at ₹512 crore. Consolidated revenue for the quarter grew 11% to ₹7,074 crore from ₹6,349 crore. For the full financial year, revenue rose 12%, but consolidated net profit fell to ₹1,869 crore from ₹2,081 crore, impacted by higher input costs. Exports saw robust growth of around 23% year-on-year, reaching ₹2,321 crore against ₹1,887 crore previously. MRF announced a dividend of ₹235 per share, including two interim dividends of ₹3 each already paid. The company said all three market segments—replacement, institutional, and export—registered strong growth. It also highlighted its ongoing presence in the electric vehicle segment across commercial, passenger, and 2/3-wheeler categories. Raw material costs softened marginally in Q4, helping offset earlier cost pressures.

- This edition of the newsletter was written by Krishna and Anurag.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()