Debt funds play an important role in your asset allocation. Since debt funds are relatively less risky than equities, they help reduce the volatility in your portfolio by providing stability. They are less risky, but not riskless. There are a few key risks you need to understand.

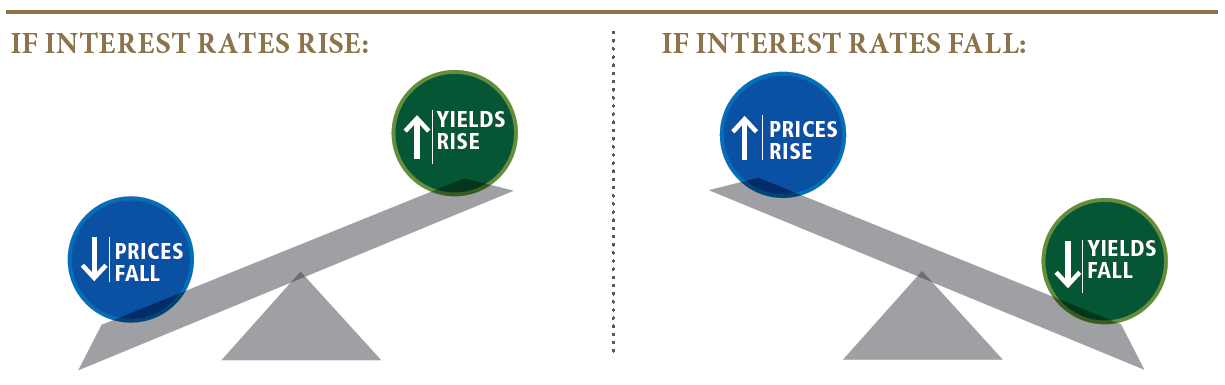

The first key risk you need to know is interest rate risk.

Bonds and, by extension, debt funds have an inverse relationship with interest rates. When interest rates rise, bond prices fall. The reason is that if interest rates rise, older bonds become less valuable.

Image: PIMCO.

Let’s say you have a bond at 5% when the interest rate (for the sake of simplicity) was 5%. If interest rates rise to 6%, companies and governments will have to issue new bonds at 6% or higher, which means your 5% bond is worth less compared to newer bonds.

So, there has to be an adjustment if someone has to buy it. That is why, as interest rates rise, the bond prices and debt fund NAVs fall. Similarly, when interest rates fall, bond prices rise and debt fund NAVs go up.

Falling interest rates are good for debt funds & vice versa.

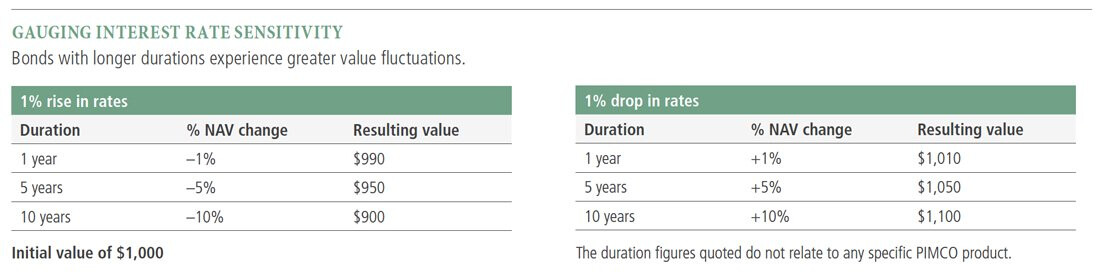

The second key risk is duration risk.

In simple terms, duration helps you figure out how sensitive a bond or a debt fund is to interest rate changes. The higher the duration, the higher the sensitivity of a bond or debt fund to interest rate changes.

There are multiple measures of duration, and modified duration is one such measure. It’s denoted in years, and you can see it in the fund fact sheets. Modified duration tells you how much a debt fund will rise or fall for a given change in interest rates.

Image: PIMCO

For example, if the modified duration of a debt fund is 5 years and if interest rates go up by 1%, the debt fund will fall by 5%. Keep in mind that duration is an approximation and bond prices and debt fund NAVs don’t fall linearly.

But it helps you quickly understand the interest rate risk in a fund. The higher the duration of a fund, the higher the interest risk is. So when interest rates go up, the modified duration of the fund will give you an idea of how much the NAV will fall.

So, if NAVs are falling, what should you do?

These funds will recover unless you sell in panic, which would be the wrong thing to do. The short-duration fund will recover faster over a few months compared to the longer-duration funds.

Just like equity funds have risks, so do bond funds. Interest rates move in cycles, and as long you stick through an entire cycle, you’ll be ok. Timing interest cycles is extremely hard.

The longer you stay invested, the lower the odds of you making negative returns.

For most investors, SIPs in debt funds based on the duration of their goals, risk appetite, and risk capacity is one of the best ways to invest. As rates rise, your subsequent investments will be invested at higher interest rates. Over the long horizon, returns will even out.

If you don’t have the ability to bear severe interest rate volatility, it’s better to invest in short-term debt funds, even for long-term goals.

You could also have a mix of short and long-duration funds if you understand the risk. There is no one right way to invest.

It’s also important to understand the role of debt funds in a portfolio. It isn’t really to generate the highest returns. That’s the role of equity. Debt funds help you lower the overall volatility of a portfolio compared to a 100% equity portfolio.

Since the volatility is lesser, debt actually helps you behave better when investing. This is an underrated reason for investing in debt funds, that gets lost in all the noise.

Debt funds can seem quite scary if you’re new. But to be honest, once you understand the basic risks and how bonds work, they become much simpler. We have a series of chapters on debt funds in the personal finance module.