India’s Biggest ever IPO opens today. Let’s have a runthrough the numbers and try and make sense of the signals amidst all that noise.

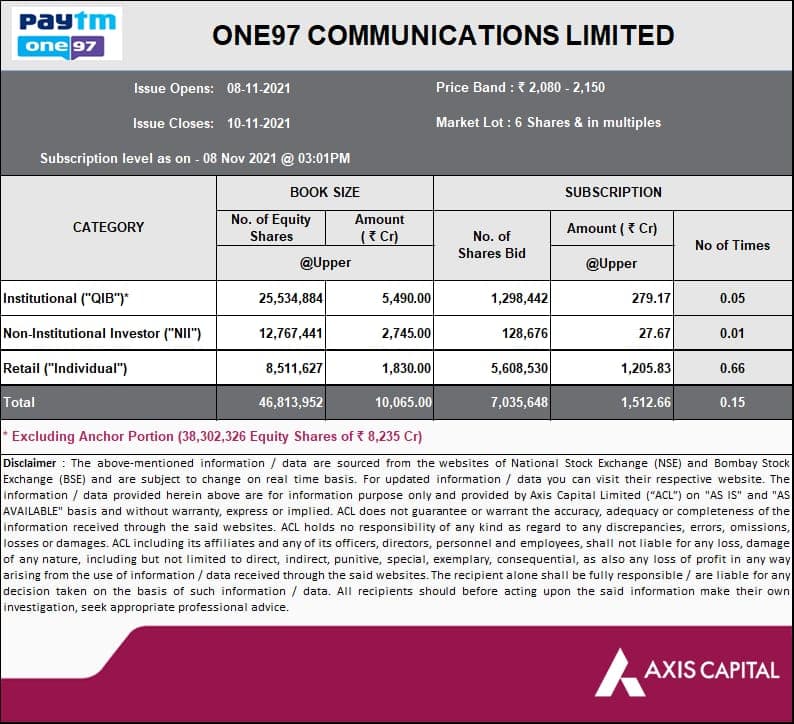

ISSUE

Financials

PayTM has cleaned up its books a lot heading into the IPO, and it did have a lot of time to do so, as the IPO was supposed to be listed in 2020, but got derailed because of COVID. Losses have been significantly brought by aggressively cutting down the marketing and promotional budget, hence the “PayTM Karo” ads are as a result running less on TV and Youtube.

Ownership

Paytm is majorly owned by its foreign overlords in China and in Softbank. This heavy Chinese involvement has been a source of constant worry in PayTM’s bid to expand into Banking and Core Finance. This however isn’t exclusive to PayTM and chinese money has awashed Indian VC space for quite some time now.

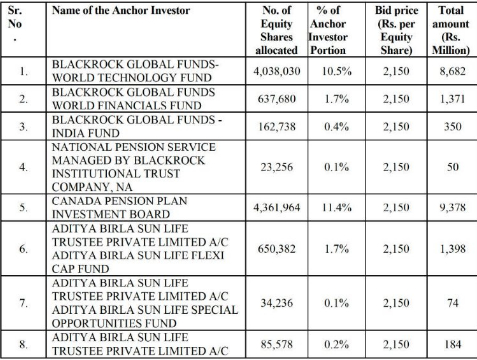

Anchor Investors :

Major Institutional players buying into this IPO would be ofcourse Blackrock the company which owns the world, and some major pensions funds alongside National Funds of Singapore and Canada. So overall mostly FII run anchor book.

Valuations

PayTM is looking to raise Rs 18,300 Cr ($ 2.5 Bn) valuing the company at 1.5 lac Cr ($ 20 Bn). At this valuation, PayTM will be a top 30 company in India by Marketcap right at the day of listing. Ahead of Multiple successful Companies which have posted phenomenal results for decades. This by all standards is a huge ask by PayTM and it has nothing really going in for it to justify this valuation.

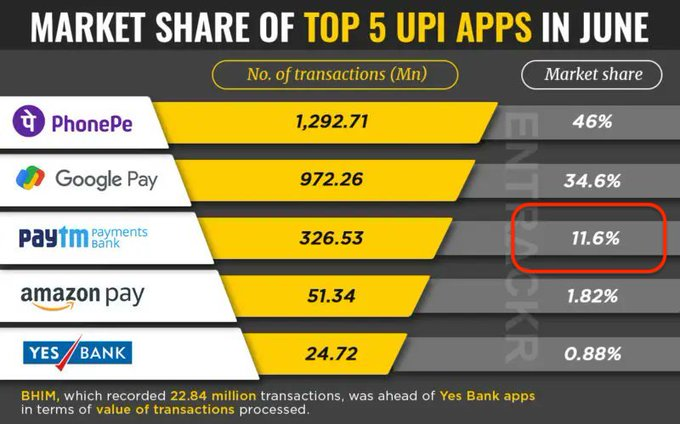

By all measures the valuation is too high for the company.The only advantage paytm has is it’s huge user base. After UPI, I don’t find many people using the paytm wallet and even the Paytm banking services are hit and miss as there are many Neo banks out there providing better service(Lifetime free cards and Free SMS alerts etc) than paytm bank. With all that being said I do use Paytm UPI as the transaction won’t fail much.

Paytm also has Paytm Mall which is dead- I don’t know who prefers it over Amazon/ flipkart or any other major online shopping app or ever will.

Paytm has Paytm Postpaid service in partnership with CLIX Finance and they charge 2-3% of fees over every transaction you do using it; unless you have Delight version.

Paytm partnerships with banks to offer credit cards but I don’t find them attractive (personal opinion) when compared to other cards in market.

They also have many other services like Personal loan, Insurance, Fasttag, travel and others. I guess they are OK. (Paytm Gold too)

Next comes Paytm Money which offers Mutual Funds and Stocks. I highly doubt that people who use Zerodha will shift to Paytm Money.

Then there is Paytm first membership and Mini apps. I don’t know about those as I never used them.

Considering all the above points and mad competition (Gpay, Amazon Pay, Bharat pe, Phone pe, Mobikwik, Freecharge, Payzaap etc). I think that the valuation is on the higher side.

All this amidst the general environment where startups which have been in business for years, are still unable to find any stable source of revenue/business model or identity, and just burning VC Money like years after years in search of dreams that one day suddenly they will have no competition and they can “focus on profitability” or maybe pass it down to the public through IPOs.

Please let me know your thoughts and wherever I am wrong with my interpretations.

Full Disclosure : These are my personal views I am not a Financial Analyst or anything, just another Trader.