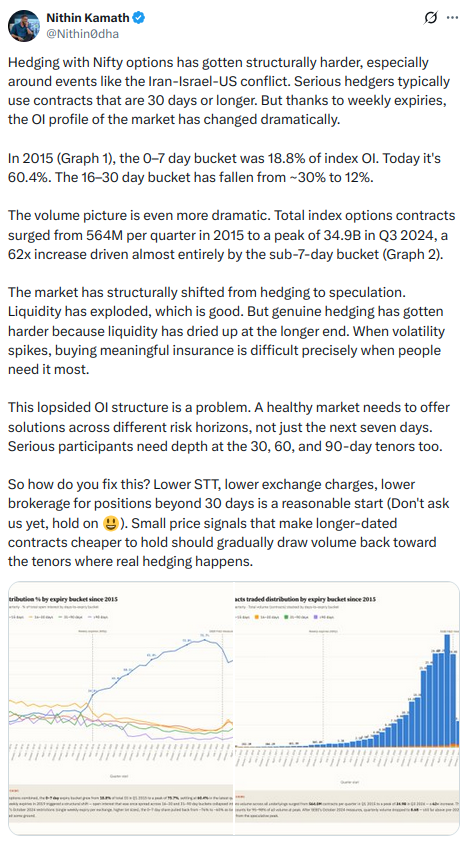

Nifty options liquidity has grown massively, though much of it now sits in very short-term expiries. Over the years, this seems to have quietly changed the structure of the market.

@nithin shared this on X Yesterday

Nifty options liquidity has grown massively, though much of it now sits in very short-term expiries. Over the years, this seems to have quietly changed the structure of the market.

@nithin shared this on X Yesterday

Upon reading the above,

and after overcoming the initial “aap keh rahe ho, theek hi hogaa…” thoughts,

here are a few questions -

market has structurally shifted from hedging to speculation

What leads us to believe that folks interested in hedging

aren’t simply preferring to use rolling shorter-term expiries?

As weekly Nifty expiries did not exist in 2015.

is the “healthy” long-dated OI profile of 2015…

hedging with NIFTY options has gotten structurally harder

If hedgers are already using rolling weeklies by choice,

will cheaper long-dated contracts actually move them?

How much cheaper?

If hedgers are doing it because long-dated liquidity is thin,

what would be the necessary magnitude of price incentives

to bootstrap sufficient liquidity in the first place?

@nithin

Why do you want to help SEBI get rid of weekly options by bringing up these points?![]()

![]()

Previously, it was you who highlighted that people were losing money in options, after which SEBI conducted a comprehensive study of the same. ![]()

Speculation is not the same as gambling if done with risk management.

If nothing is done to fix the lopsided volume concentration in weeklies, then it’s certainly going away in a few years time! ![]()

Incentivizing participation in longer dated options is the better alternative. ![]()