Interesting concept, theoretically sounds good.

In India, could be adapted to use FDs that payout quarterly and 3-month options on NIFTY.

1 Like

…Interesting concept, theoretically sounds good.

Not really.

A strategy/ETF where you can’t lose money…

…but one pays the opportunity-cost of missing zero-risk opportunities,

i.e. even lose the otherwise guaranteed returns from zero-risk opportunities.

![]()

![]()

![]()

Note that the benchmark for schemes that claim one doesn’t lose anything

is not the no-loss-no-profit scenario.

Rather, the benchmark to beat is

the returns of the sovereign govt. bonds during the same period.

The non-zero positive appreciation of an investment into govt. bonds at absolute zero risk*.

(* = minuscule risk being the continued existence of a solvent sovereign entity)

So, these “buffer funds” are a strategy where

we can risk losing-out on the zero-risk guaranteed appreciation of Govt. bonds,

in search of potentially higher market-linked returns.

3 Likes

True, theoretically. But if you consider the upward bias of the markets over the last 30 odd years, I’m sure this would beat the risk-free returns of a soverign govt bonds, esp in India. However, to your point, this needs to be backtested (I don’t have the data to do that, though).

1 Like

If one wants to rely on that historical bias,

then one can simply stick with a large-cap ETF then, right?

Yes, i too am sure it would.

And this strategy does that by taking additional risk.

i.e. no guarantees that there will be some moderate returns each year

unlike when investing in sovereign govt. bonds

that have guaranteed a moderate return every year irrespective of market conditions.

Lol it’s like saying invest in Gsecs and then reinvest the coupon payments in any asset class of choice. The max you can lose is the coupon income and not the original principal - hence a ‘lossless’ strategy!!

If this was true, you could have just traded the call options with the entire capital, rather than investing 95% of the capital in gsecs and using only 5% for call options . Right?

Nope. Cos once you lost the capital, you have none to invest in the next year.

Again, you’re theoretically correct.

Yet again I disagree, cos living thru the drawdowns is where most people falter.

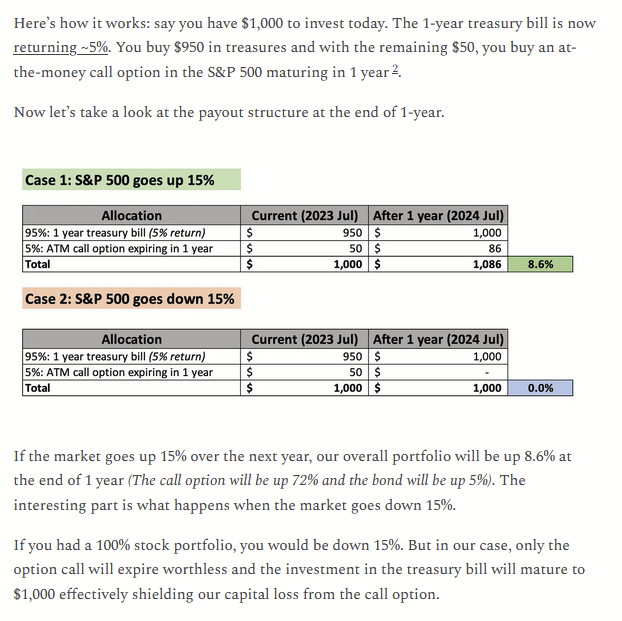

Hey guys,

Just want to clarify that I have no skin in the game. Just read an article that I thought would serve a different perspective as food for thought. Especially for people who hate drawdowns but still want to participate on the upside.

I am not following this strategy nor do I recommend that you blindly follow it.