Reliance is soon launching its rights issue. The F&O contracts of a company’s shares are adjusted on the ex-date (in this case, May 13th) to incorporate the effect of such corporate actions. On the basis of the closing price of Reliance in the cash market, the exchange will arrive at an adjustment factor to modify:

The number of shares per lot for futures and options contracts

The strike price for options contracts

Edit - May 12, 2020

NSE has modified the lot size to 505 shares per lot for F&O contracts.

Check this circular for the updated strike prices of options contracts by multiplying the current strike price by the adjustment factor 0.990610. For example, 1400 CE will become 1386.85 CE, 1300 PE will become 1287.80 PE, and so on.

Similarly, the futures adjusted price will be the closing price on May 12th multiplied by the adjustment factor.

Contract

Closing Price on May 12th

Adjusted Price

May Futures

1484.6

1470.70

June Futures

1482.2

1468.30

July Futures

1485.05

1471.10

You can check this circular from NSE for an illustration on how the adjustment factor is calculated.

Your positions will be brought forward from May 12th to 13th by adjusting the lot size and contract price in accordance with the adjustment factor. In accordance with the above example, the strike price for options will be reduced by the “benefits per share” and the lot size will be increased by dividing the current lot size (i.e. 500) by the adjustment factor.

Please note that this calculation is dependent on the closing price of Reliance shares on May 12th.

Pls also elaborate which is better at EOD 12 th May - holding one lot in future or having 500 equity shares. Or both the positions are net neutral. Thanks.

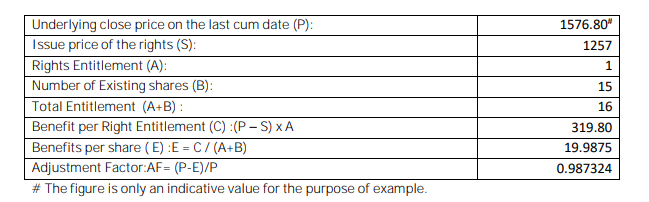

Let’s say you buy 500 shares of Reliance in the cash market at Rs. 1557 on May 12th (when the share is trading cum rights). The benefit you receive per 15 shares is Rs. 300 (i.e. 1557-1257 since you’re entitled to buy one share of Reliance at Rs. 1257 even though the price is Rs. 1557.

On May 13th, if nothing else changes, the theoretical price of the shares should be lower by Rs. 20 (i.e. (1557-1257)/15). Accordingly,

a. Cost of your holdings: 500x1557 = 778500

b. Theoretical price on May 13th (without any market changes): 1557-20 = 1537

c. Price of your holdings: 500x1537 =768500

d. Number of rights you receive: 500/15 = 33

e. Value of rights you receive: 300 x (d) = 9900

Erosion in value for you is (a) - {c + e} = Rs. 100 (This is equal to the value of the fractional rights you did not receive (i.e. 300x0.33)). However, if you held Reliance shares in multiples of 15 then theoretically you would maintain status quo.

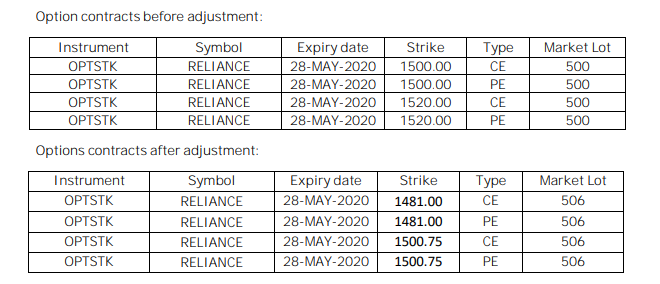

If you buy one lot of reliance futures at Rs. 1560 on May 12th, and let’s say the closing price is Rs. 1557 then you have lost Rs. 1500 (i.e. 3x500). The opening price on May 13th will be adjusted to Rs. 1537 (i.e.1557-20). This doesn’t you have lost Rs. 20 per share. Your carry forward price is taken at Rs. 1537 instead of Rs. 1557. Also, the lot size will be modified to 507 shares i.e. (500/(1537/1557). So, your gain/loss on May 13th will be computed from the base price of Rs. 1537 with a lot size of 507 shares.

Accordingly, theoretically, in the absence of market movements, the gain/loss doesn’t change for you due to the rights issue.