IMO, the advance tax calculation shown in the example above for Q2 seems wrong.

Obviously, for capital gains, tax needs be calculated based on actual gains, rather than estimates.

Now, in the above example, the cumulative tax liability needs to be seen at the end of each quarter, which needs to be adjusted for any advance tax paid in previous quarter(s), to determine the actual advance tax to be paid.

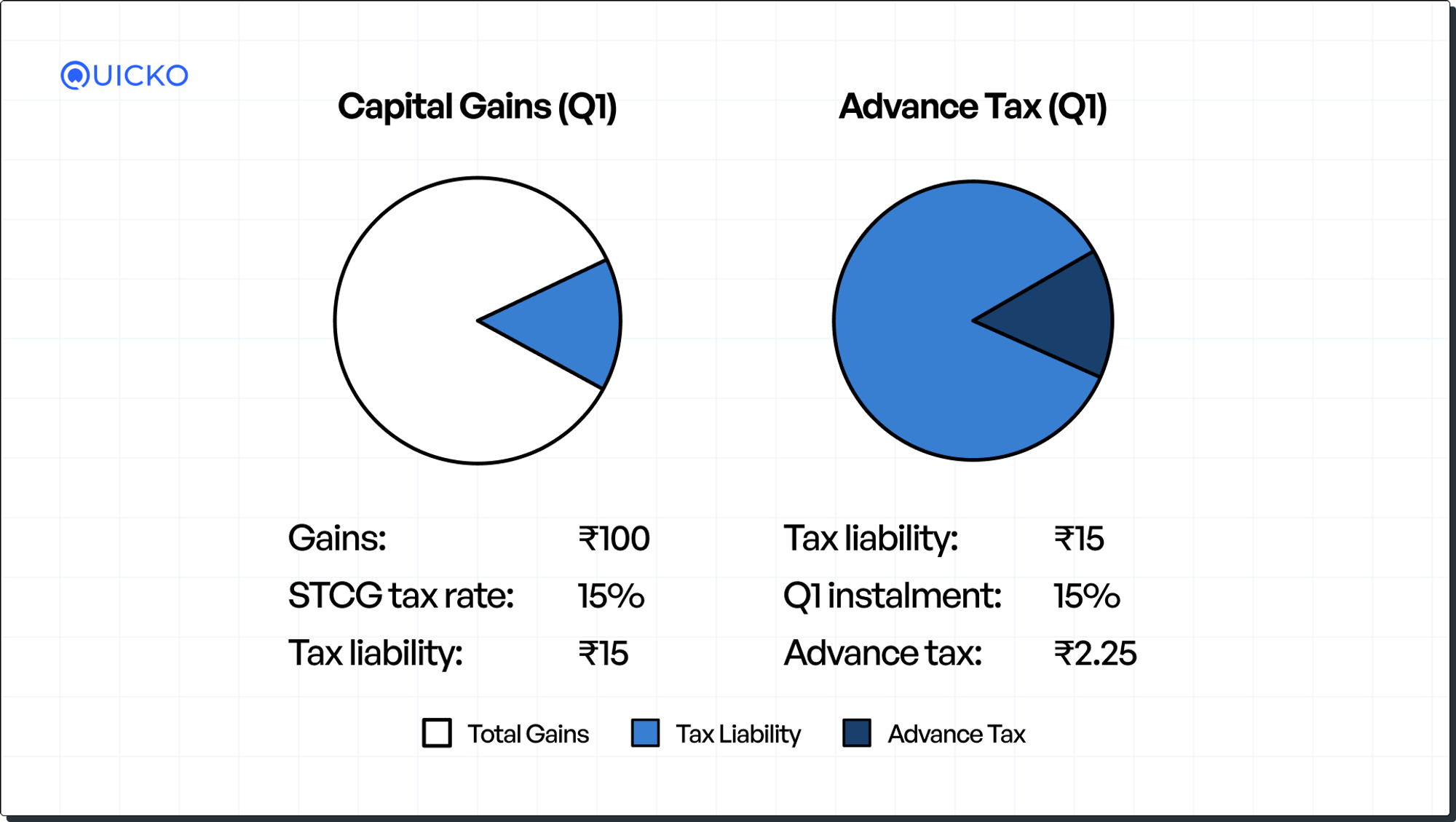

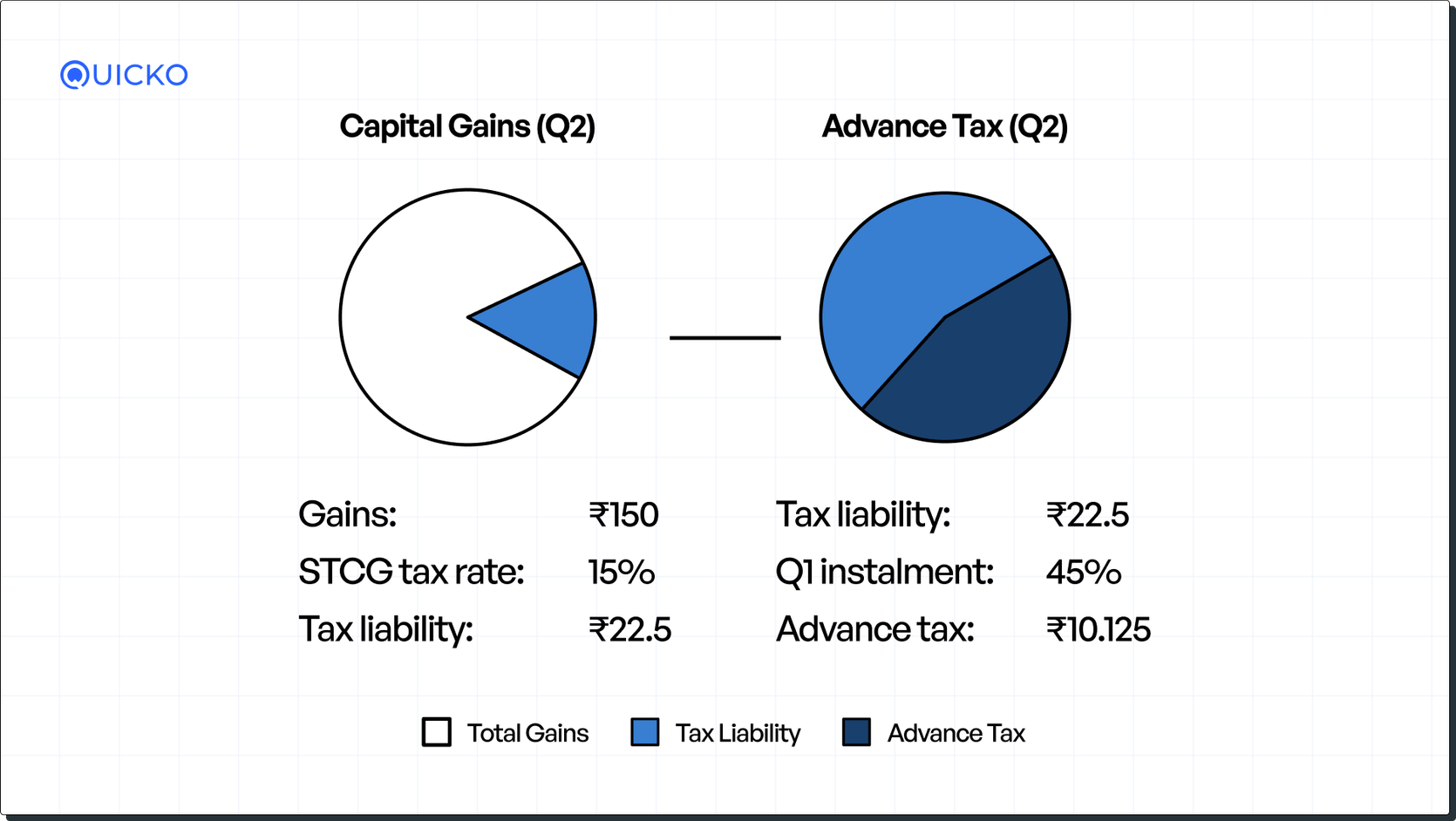

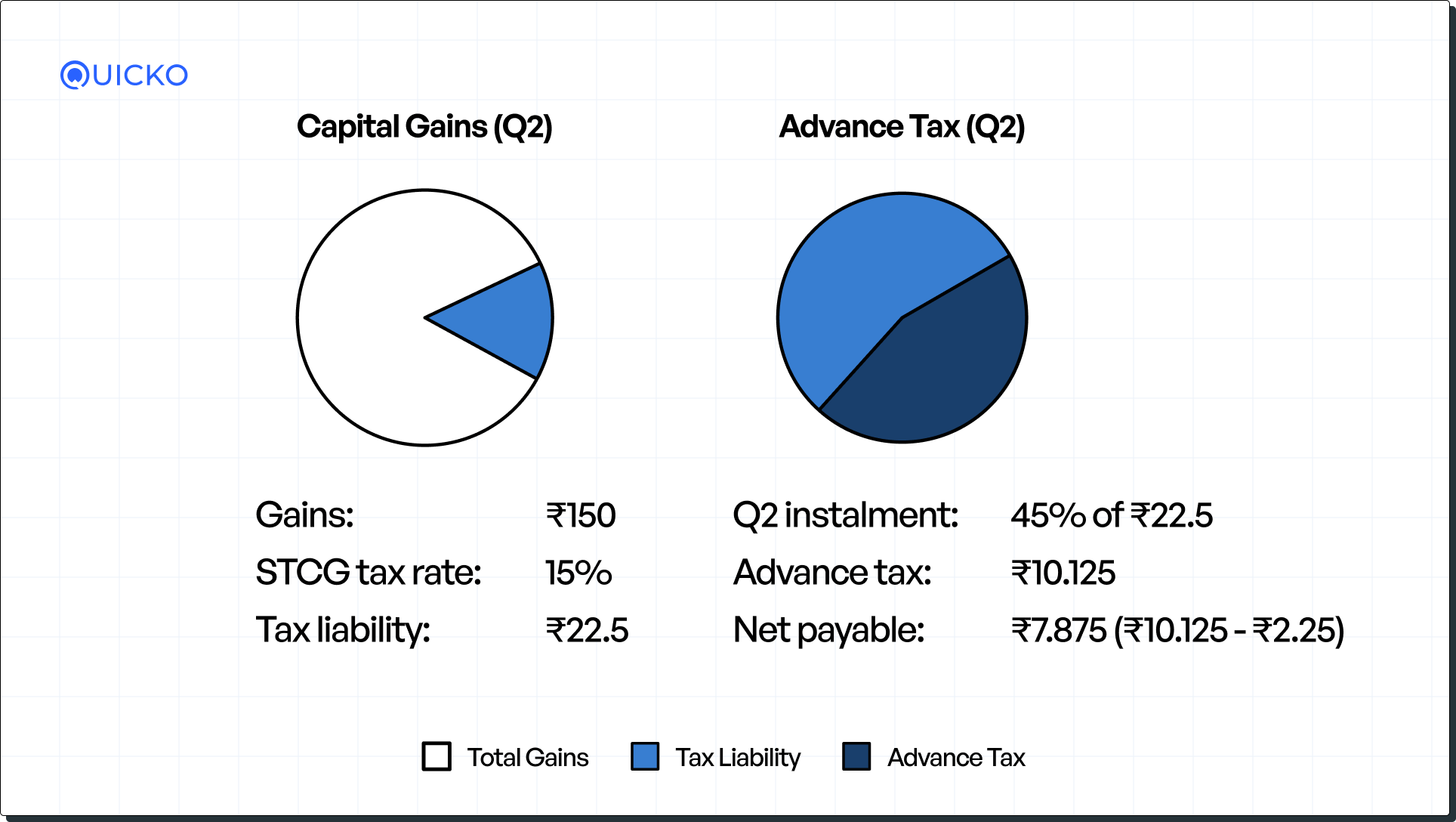

If my gains in Q1 is ₹100 and Q2 is ₹50.

For Q2, the advance tax to be paid would be ₹7.875

i.e.,

45% of advance tax (-) advance tax already paid

Calculation:

Total gains at the end of Q2 (100+ 50) = ₹150

Total tax liability in Q2 = (₹150 *15%) = ₹22.5

Advance tax to be paid in Q2= [(22.5 * 45%) - Advance tax already paid in Q1]

(₹10.125 - ₹2.25) = ₹7.875

So when the gains increase subsequently, the advance tax liability of previous quarters will remain unaffected, however the advance tax payment needs to be adjusted and calculated based on the cumulative gains of all quarters, rather than considering only the gains of the current quarter.

This view would be correct for determining the advance tax liability for other sources of incomes other than capital gains. As advance tax (for eg: business income) involves payment based on estimates, unlike capital gains, which is calculated based on actual realisation.

Capitals gains schedule in ITR contains a table , which requires you to update the gains made in each quarter.

If this is filled properly, no interest or penalty would be levied for short payment of advance tax due to increase in gains in subsequent quarters.